![Open Lending Corp. (LPRO) Securities Class Action Lawsuit Update [May 22, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/lpro.jpeg)

Introduction

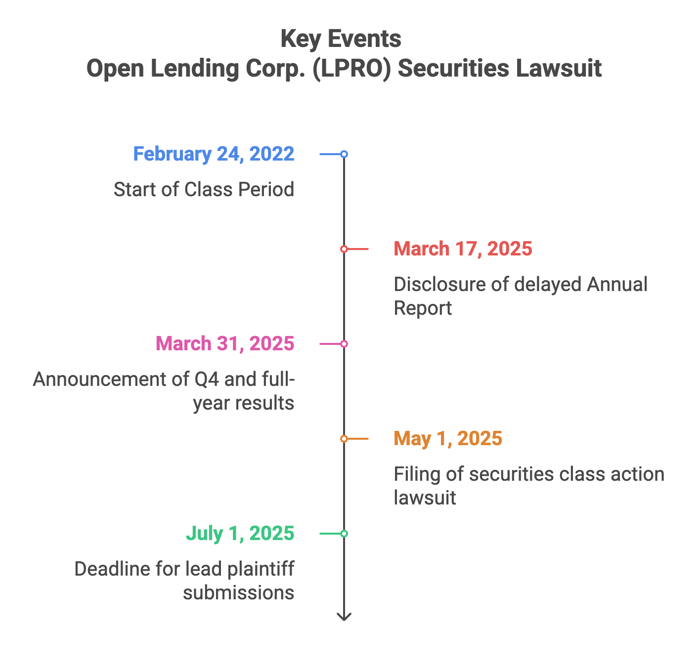

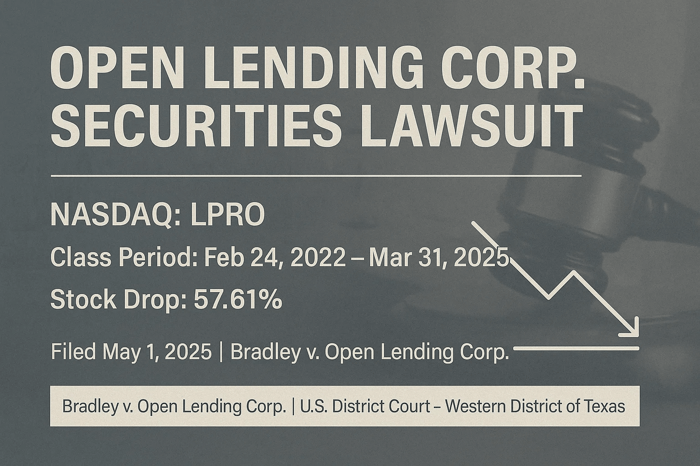

A securities class action lawsuit has been filed against Open Lending Corporation (“Open Lending” or the “Company”) for alleged violations of federal securities laws, including the Securities Exchange Act, during the period from February 24, 2022 to March 31, 2025 (the “Class Period”). The lawsuit seeks to recover damages for investors who purchased or otherwise acquired Open Lending securities during the Class Period.

The securities fraud Complaint alleges Open Lending Corporation touted the effectiveness of its risk analytics solutions, underpinning its Lender Protection Platform. However, Open Lending failed to disclose vintage loans had become worth significantly less as vehicle prices declined. In March 2025, the Company disclosed its Fourth Quarter 2024 and Fully Year 2024 financial results were substantially worse than anticipated.

Investors reacted negatively to the news. Open Lending stock fell 57% in one day.

Open Lending Corp. (LPRO) Lawsuit Case Details

Bradley v. Open Lending Corporation, et al.

Case No.: 1:25-cv-00650

U.S. District Court, Western District of Texas

Filed on May 1, 2025

Open Lending Corp. (LPRO) Company Profile

Open Lending Corporation is a financial technology company that provides loan services to automotive lenders. Its core offering, the Lenders Protection Platform, is a cloud-based software used to underwrite default insurance for loans issued to near-prime and non-prime borrowers. Open Lending generates revenue through program fees, profit-sharing with insurance partners, and claims administration fees.

Open Lending Corp. (LPRO) Lawsuit Class Period

February 24, 2022 to March 31, 2025, inclusive.

Investors who acquired Open Lending securities during the class period might be eligible to join the Open Lending Corp. lawsuit.

Allegations in the Open Lending Corp. (LPRO) Securities Lawsuit

Throughout the Class Period, Open Lending repeatedly touted the effectiveness of its risk-based accounting and review processes, which underpin its flagship Lenders Protection Platform. The Company claimed these proprietary models allowed lenders to assess borrower risk within seconds, using a combination of credit bureau and alternative data.

However, the complaint alleges that Open Lending failed to disclose mounting problems in its loan portfolio. Specifically, loans originated in 2021 and 2022—when used car values peaked—had become “worth significantly less than their corresponding outstanding loan balances” as vehicle prices declined. This deterioration in the Company’s 2021 and 2022 vintages ultimately accounted for approximately 40% of the profit share revenue revision disclosed in March 2025.

In 2023 and 2024, Open Lending originated additional loans that were later found to be underperforming. The complaint states that two borrower cohorts — those with “credit builder tradelines” and those with “fewer positive tradelines” — experienced elevated default rates, contributing another 40% to the downward revision in profit share revenue. The remaining 20% of the revision stemmed from elevated delinquencies and defaults across the broader loan portfolio.

The securities fraud complaint filed against Open Lending alleges the Company made materially misleading statements regarding its loans throughout the Class Period, misrepresented the capabilities of its risk-based pricing models, and failed to disclose the extent of its exposure to underperforming loans. As a result, investors were misled about the true financial condition of the Company.

The Truth Emerges

On March 17, 2025, Open Lending disclosed it would be unable to file its Annual Report on time due to complications “related to its profit share revenue and related contract assets.” The Company stated that it needed additional time to finalize its accounting review processes.

Two weeks later, on March 31, 2025, Open Lending announced its Q4 and full-year 2024 results, revealing quarterly revenue well-below expectations. The Company reported a quarterly revenue of negative $56.9 million, driven by an $81.3 million reduction in estimated profit share revenues. This reduction was attributed to delinquency-driven defaults and poor performance from its 2021–2024 vintages. The Company also revealed a $144 million net loss and a massive $86.1 million valuation allowance on deferred tax assets. At the same time, Open Lending replaced its CEO and COO, who had previously held multiple executive titles simultaneously.

Market Reaction

Investors reacted sharply to the revelations. Following the financial disclosures and executive shakeup, Open Lending stock fell 57.61% in a single day.

Next Steps

Submissions for lead plaintiff are due July 1, 2025.

The Court will issue its order for lead plaintiff and counsel in the weeks after submissions are due.

The Court will then consider motion for class certification.

The Court will later consider a Motion to Dismiss.

To learn if you are eligible for recovery under the Open Lending shareholder class action, visit the case submission page here.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Ibotta, Inc. (IBTA) Securities Class Action Lawsuit Update [May 22, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/ibotta-securities-class-action.webp)

![BigBear.Ai Holdings, Inc. (BBAI) Securities Class Action Lawsuit Update [May 15, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/bigbearai-lawsuit-blog-banner.webp)