![Unicycive Therapeutics, Inc. (UNCY) Securities Class Action Lawsuit Update [October 6, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/unicycive-therapeutics-uncy-lawsuit-blog-banner.webp)

Unpacking the UNCY Securities Class Action Allegations and Investor Fallout

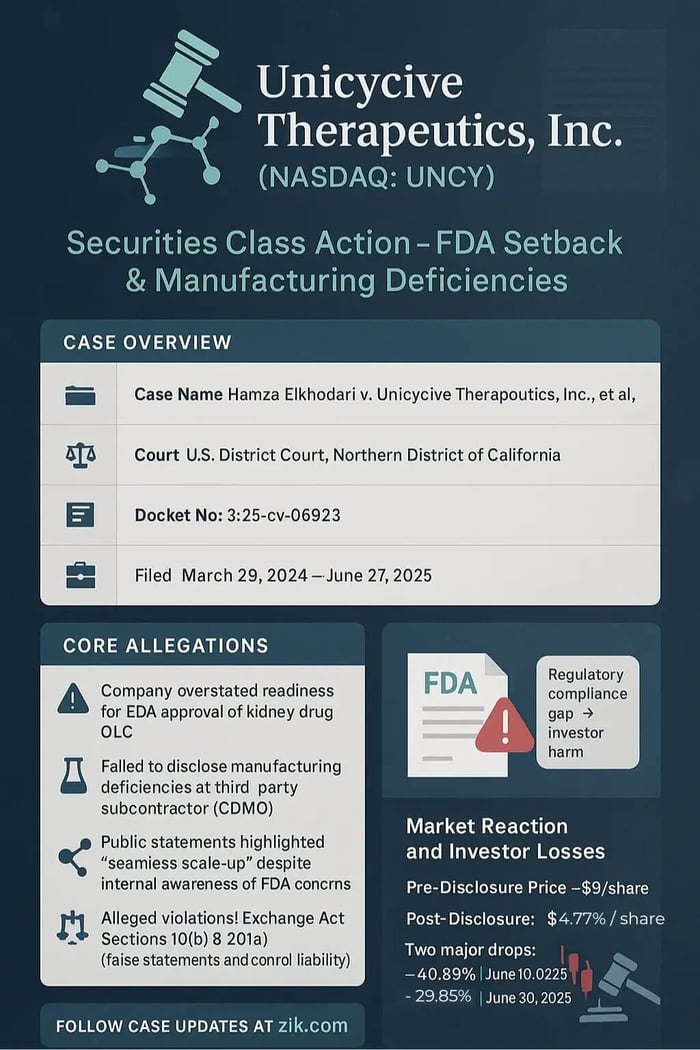

Case Name: Elkhodari v. Unicycive Therapeutics, Inc., et al.

Docket Number: 3:25-cv-06923

Court: U.S. District Court, Northern District of California

Filing Date: August 15, 2025

Class Period: March 29, 2024 – June 27, 2025

Introduction

Unicycive Therapeutics, Inc. (NASDAQ: UNCY) promised a breakthrough in kidney disease treatment, a next-generation drug poised to ease the burdens of patients on dialysis. Investors bought in, drawn by assurances of FDA readiness and manufacturing prowess. Then came the June 2025 revelations. Manufacturing lapses, regulatory roadblocks, and two stock plunges: a 40.89% plunge on June 10, 2025, following news of FDA-identified deficiencies at a third-party manufacturer, and a 29.85% fall on June 30, 2025, after a Complete Response Letter (CRL) citing the same issues. Now, a securities class action lawsuit accuses the company of misleading the market.

Backdrop and Business Context

Unicycive Therapeutics emerged as a clinical-stage biotechnology firm focused on unmet needs in kidney disease. Headquartered in Los Altos, California, Unicycive positions itself as an identifier and developer of therapies, leveraging third-party partners for manufacturing and commercialization. This lean model—common in early-stage biotech—allows focus on innovation without heavy infrastructure costs.

Central to its story is OLC, touted as a superior phosphate binder. Hyperphosphatemia affects millions on dialysis, where high phosphate levels strain hearts and bones. Existing treatments burden patients with dozens of pills daily; OLC promised fewer, thanks to nanoparticle technology enhancing absorption. By 2024, Unicycive had completed pivotal trials, submitted an NDA, and gained FDA acceptance with a PDUFA date of June 28, 2025. Milestones like enrollment completion in trials and positive data readouts built momentum. Yet, reliance on contract development and manufacturing organizations (CDMOs) and their subcontractors introduced vulnerabilities—ones that, per the lawsuit, management downplayed amid hype.

Promises Made vs. Reality

Executives painted a picture of seamless readiness. In a March 28, 2024, press release announcing FY 2023 results, Gupta declared: "[W]e remain on track with topline data expected from the trial towards the latter part of the second quarter of this year and plan to file the NDA shortly thereafter." The accompanying 10-K echoed confidence, noting "manufacturing standards... established" and executive "expertise in the biopharmaceutical industry," while boilerplate risks on noncompliance felt distant.

As alleged in the complaint, the reality diverged. Gupta's June 25, 2024, conference call response to manufacturing queries: "[W]e are very, very much ready... scaling up our manufacturing process. There is no problem." Yet, FDA inspections uncovered cGMP deficiencies at a third-party subcontractor, halting label discussions and leading to the CRL.

Timeline of Alleged Misconduct and Disclosures

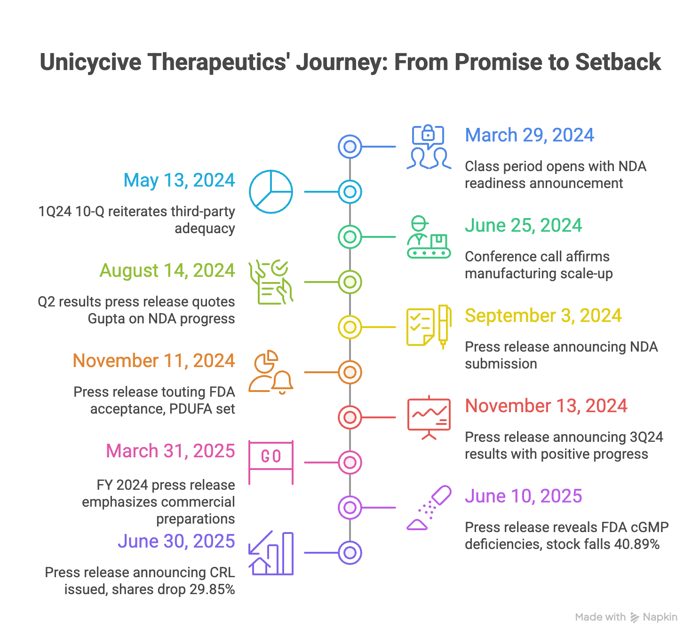

Class Period: March 29, 2024 – June 27, 2025

- March 29, 2024: The class period opens with post-FY 2023 results touting NDA readiness.

- May 13, 2024: 1Q24 10-Q reiterates third-party adequacy.

- June 25, 2024: Conference call affirms manufacturing scale-up.

- August 14, 2024: Q2 results press release quotes Gupta: "We remain on track to submit our NDA by the end of this month... high degree of confidence."

- September 3, 2024: Press release announcing NDA submission, with "specifications and practices related to chemistry, manufacturing and controls" supporting the package.

- November 11, 2024: Issued press release touting FDA acceptance, PDUFA set for June 28, 2025.

- November 13, 2024: Issued a press release announcing 3Q24 results touting positive progress and NDA acceptance.

- March 31, 2025: FY 2024 press release emphasizes commercial preparations.

- June 10, 2025: The unraveling. Press release reveals FDA cGMP deficiencies at a third-party subcontractor, precluding label talks. Stock falls 40.89% to $5.32.

- June 30, 2025: Press release announcing CRL issued, citing the same issues. Shares drop 29.85% to $4.77.

Investor Harm and Market Reaction

Quantifiable pain: From class period highs around $9 pre-split, shares cratered post-disclosures. The June 10 drop erased $3.68 per share; June 30 shaved another $2.03.

Market reactions were swift. Pre-market trading on June 10 saw 20% losses initially, ballooning to 40.89% close. Analysts responded: One analyst noted the CRL as "derisking" if fixable, but cut targets; Benchmark adjusted post-split to $21 (from pre-split equivalent). Broader sentiment turned cautious, with Yahoo Finance showing downgrades amid biotech volatility.

Each inflection tied to disclosures: Manufacturing news shattered confidence in NDA prospects, amplifying harm for long-term holders.

Litigation and Procedural Posture

The complaint invokes Section 10(b) of the Exchange Act and Rule 10b-5 for false statements, plus Section 20(a) for controlling-person liability against Gupta and Townsend. Scienter allegations? Access to adverse facts—via internal reviews and FDA interactions—yet public optimism persisted. No insider sales detailed.

Procedural steps: Filed August 15, 2025; lead plaintiff motions due soon, with motion to dismiss likely shortly thereafter, testing PSLRA standards for particularity.

Shareholder Sentiment

Across platforms, shareholders grapple with betrayal and resilience. On X (formerly Twitter), reactions spiked post-June drops. One user lamented, "UNCY already has a lawsuit and this company has never had one. It’s crazy to me," capturing shock amid historical stability. Optimism lingering with one user stating: "What we know is that UNCY has a drug that is safe and works, and FDA agrees with this. And when they sort out the manufacturing issues."

Reddit threads echo frustration: "Seems to me that if this was already communicated by FDA then there was something uncy could do about it before the decision." Sentiment trends downward post-CRL, with queries on revenue potential: "some analysts say 500m, but that seems very unrealistic"—and calls for diligence. r/UNCY hosts tactical talk: "When OLC approved, what is its expected revenue?"

Stocktwits mirrored this. Bearish volume surged 300% post-June 10, with messages like "Going all in on UNCY" turning to "What’s going on with the stock?" Overall, a pivot from YOLO enthusiasm to wary monitoring, underscoring biotech's emotional toll.

Analyst Commentary

Professional views evolved with events. Before the June 2025 disclosures, analysts built a bullish case around Unicycive's NDA momentum and OLC's potential in hyperphosphatemia treatment. In April 2024, Piper Sandler initiated coverage with an Overweight rating and $90 price target, highlighting the drug's differentiated profile amid positive trial data. February 2025 saw Noble Financial start Outperform at $60, emphasizing commercial upside. Guggenheim joined in April 2025 with a Buy at $60, citing FDA acceptance and PDUFA proximity. HC Wainwright reiterated Buy multiple times through early 2025—at $7.50 in April and $9 in May—praising manufacturing readiness and pipeline progress. Consensus leaned Strong Buy, with averages near $60 and highs at $105, fueled by expectations of a mid-2025 launch.

The June 10 manufacturing alert and June 30 CRL tested that optimism, but reactions stayed measured—framing the issues as resolvable vendor snags rather than fatal flaws. Maxim Group reiterated Buy at $30 on CRL day, viewing it as a short-term delay. HC Wainwright held Buy at $9, calling the CRL "anticipated" and unrelated to OLC's core efficacy. Noble Financial echoed this in August, sticking with Buy at $6 (adjusted post-split), noting Unicycive's backup suppliers could swiftly address cGMP gaps: "We believe this may be corrected by using different manufacturers." Benchmark maintained Speculative Buy, boosting its target to $21 in September after the reverse split, signaling confidence in a January 2026 resubmission. Consensus held Strong Buy into October, averages at $55-60, with upside potential tied to Type A meeting outcomes— a resilient thread in biotech's regulatory weave.

SEC Filings & Risk Factors

Unicycive's filings disclose risks, but the lawsuit argues omissions amplified harm.

The FY 2023 10-K (filed March 28, 2024) warns of "noncompliance with regulatory standards and requirements," including cGMP, yet downplays via boilerplate: "We plan to continue to use third-party service providers... to manufacture and supply the materials." Management highlights "considerable product launch experience," implying control.

Q1 2024 10-Q (May 13) repeats: Third-party sufficiency assumed, with SOX certifications affirming no material omissions. Q2 2024 10-Q (August 14) maintains this, post-NDA submission. Q3 2024 10-Q (November 13) notes CMC data support, but risks section flags "dependence on third parties" for compliance.

Recent 10-Q (August 14, 2025) post-CRL urges reading prior risks, including "any material adverse change" in factors like manufacturing.

Conclusion: Implications for Investors

This case teaches vigilance in biotech's shadows. Red flags? Overreliance on third parties, mismatched assurances versus outcomes. For similar firms, scrutinize CDMO chains; FDA CRLs often stem from manufacturing, not molecules. Broader lesson: In a sector of binary events, diversified portfolios buffer; class actions offer recourse, but prevention outweighs recovery. As Unicycive navigates fixes, investors weigh resilience against risk— a reminder that breakthroughs demand not just science, but unyielding execution.

![LifeMD, Inc. (LFMD) Securities Class Action Lawsuit Update [October 9, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/lifemd-securities-lawsuit-blog-banner.webp)

![Tronox Holdings Plc (TROX) Securities Class Action Lawsuit Update [October 9, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/tronox-holdings-securities-lawsuit-blog-banner.webp)

![PubMatic, Inc. (PUBM) Securities Class Action Lawsuit Update [October 6, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/pubm-banner-image.webp)