![Charter Communications, Inc. (CHTR) Securities Class Action Lawsuit Update [October 13, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/charter-communications-chtr-securities-class-action-update.webp)

The ACP Shadow and Broadband Blues

Case Name: Sandoval v. Charter Communications, Inc., et al.

Docket Number: 1:25-cv-06747

Court: U.S. District Court, Southern District of New York

Filing Date: August 14, 2025

Class Period: July 26, 2024 – July 24, 2025

Introduction

Introduction

The broadband highway Charter Communications built—once a vein of steady cash flow—now feels like a detour through gravel. On July 25, 2025, shares of the cable giant plunged 18.4% as quarterly results laid bare the lingering sting of a federal program's demise. Investors, caught in the wake of optimistic forecasts, filed a class action in New York's Southern District, alleging executives painted a rosier picture of recovery than the numbers allowed. At its core: the Affordable Connectivity Program (ACP), a subsidy lifeline severed in mid-2024, whose echoes continue to hollow out subscriber rolls and revenue streams. This suit isn't just about one earnings miss. It's a reckoning for a company that bet big on mobile pivots and network upgrades, only to find federal policy pulling the rug.

Backdrop and Business Context

Charter Communications emerged from the cable industry's scrappy origins, a patchwork of local monopolies stitched into a national force. Founded in 1993, it traced roots to the post-war boom when coaxial lines first snaked through rural America, delivering fuzzy signals to living rooms. By the late 1990s, Charter had consolidated smaller operators, going public in November 1999 with an IPO that raised $3.2 billion at $19 per share—60% of its equity sold to fuel expansion. Nasdaq listing followed, though bankruptcy loomed in 2009 amid debt from aggressive acquisitions. Relisted in 2010, Charter's trajectory accelerated in 2016 with the $71 billion combined value merger of Time Warner Cable and Bright House Networks, birthing Spectrum: a rebranded behemoth serving more than 25 million customers across video, internet, and voice.

Today, Charter operates as the U.S.'s second-largest cable provider, with residential internet as its anchor—$13.8 billion in Q2 2025 revenue. Milestones mark resilience: 500,000 mobile lines added quarterly, pushing wireless into a $1 billion revenue stream; fiber overbuilds in select markets to counter fixed wireless threats from T-Mobile and Verizon. Yet the operational setup—reliant on legacy coax infrastructure—exposed vulnerabilities when Washington cut the cord on subsidies. The ACP, launched in 2021, funneled $30 monthly credits to 23 million low-income households, padding Charter's gross adds by 100,000 annually. Its end in May 2024 wasn't a footnote; it was a fault line, amplifying churn in an era of cord-cutting and economic pinch.

Promises Made vs. Reality

Throughout the Class Period, Charter executives repeatedly assured investors that the company was executing effectively despite the end of the Affordable Connectivity Program (“ACP”). In the July 26, 2024 earnings release and call, CEO Chris Winfrey told investors that Charter was “executing well on several transformational initiatives,” asserting that the company was “growing EBITDA through efficiencies” and “fully focused on driving customer growth.” He emphasized that Charter had “retained the vast majority of ACP customers so far.” CFO Jessica Fischer echoed that the company could “deliver solid EBITDA growth” and expected “accelerating EBITDA growth in the back half of the year,” even with the ACP’s termination.

In subsequent quarters, Winfrey continued to characterize Charter’s transition away from the ACP as successful. In the 3Q 2024 call, he claimed the company was “successfully managing the transition of customers previously on the government’s affordable connectivity program” and that Charter remained “confident in our ability to return to healthy long-term growth.” Fischer reinforced that “we continued to do a very good job in managing the end of the program” and had “retained the vast majority” of former ACP participants.

By January 2025, Charter executives were telling investors that the ACP’s impact was “now behind us.” Winfrey stated that Charter had “managed the end of the affordable connectivity program successfully” and kept “roughly 90% of former ACP customers connected.” Fischer said the company’s “core Internet results” were improving and that Charter was “poised for strong free cash flow growth.” On the April 2025 call, Winfrey reiterated that the “impact of the elimination of the ACP is behind us,” citing “accelerated” EBITDA growth and “robust free cash flow results”

The complaint alleges that these repeated assurances were materially false or misleading. According to the filing, Charter could not manage or promptly move beyond the ACP’s end, which in reality had a “sustaining impact on Internet customer declines and revenue.” The company allegedly “failed to execute broader operations” that could compensate for those effects and therefore “had no reasonable basis” for statements that it was successfully executing its growth strategy or maintaining the long-term trajectory of EBITDA growth.

The truth, according to the complaint, began to emerge on July 25, 2025, when Charter disclosed second-quarter 2025 results showing only 0.5% EBITDA growth—which analysts later determined would have been a decline of 0.3% absent a one-time $45 million benefit. Charter also reported a loss of 117,000 Internet customers, nearly double the prior quarter’s decline. Winfrey admitted that former ACP customers, now without subsidies, showed higher non-payment rates that continued to affect results. Following these revelations, Charter’s stock price fell 18.4% in a single day.

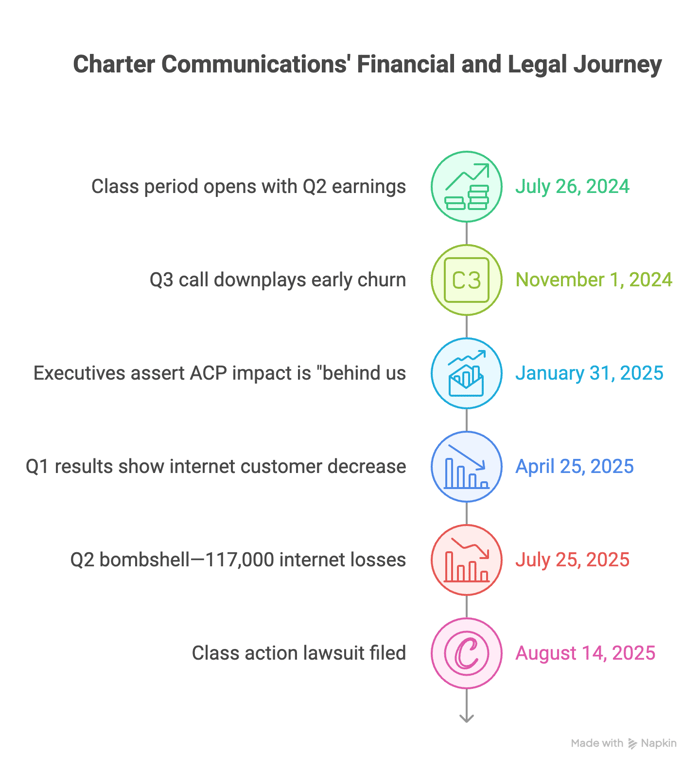

Timeline of Alleged Misconduct and Disclosures

Class Period: July 26, 2024 – July 24, 2025, inclusive.

- July 26, 2024: Class period opens with Q2 earnings. Winfrey touts strong execution.

- November 1, 2024: Q3 call downplays early churn. Winfrey said Charter was "successfully managing" the transition of former ACP customers and would have grown Internet customers in the third quarter despite ACP ending in June.

- January 31, 2025: Winfrey asserted the ACP's end had been managed successfully, that roughly 90% of former ACP customers remained connected, and that the ACP's impact was "behind us."

- April 25, 2025: Q1 results showed residential Internet customers decreased by 66, 000 and Winfrey reiterated “the impact of the elimination of the ACP is behind us.”

- July 25, 2025: Q2 bombshell—117,000 internet losses, year‑over‑year Adjusted EBITDA growth of 0.5% but disclosed this figure included a $45 million one‑time benefit. According to the complaint, Charter claimed “[t]he drop included the impact of approximately 50,000 disconnects related to the end of the ACP in the second quarter of 2024.” Shares crater 18.4%.

Investor Harm and Market Reaction

The math of betrayal: From $380 close on July 24 to $309.75 the next day, Charter's share price tumble was a 18.4% gut punch. Earlier inflection: May 2025 peak at $437 saw $2 billion evaporate by July, tied to ignored churn signals.

Analysts pivoted fast. Wells Fargo slashed targets from $450 to $340 post-earnings, citing "underestimated ACP tail"—a 24% haircut. Market cap shed 25% YTD by September, underperforming S&P by 18 points. Yet rebounds flickered: August dip-buying added 5% as shorts covered, underscoring the sector's volatility where policy whims meet pipe dreams.

Litigation and Procedural Posture

The complaint wields Sections 10(b) and 20(a) of the Exchange Act, with control person claims against Winfrey and Fischer. Defendants: Charter, its C-suite duo—CEO Winfrey and CFO Fischer.

Posture: Lead plaintiff motion deadline October 14, 2025 with motion to dismiss likely shortly thereafter.

Shareholder Sentiment

Pre-disclosure, forums buzzed with guarded praise for execution. Post-July 25, that faded into recrimination. Retail investors, long attuned to Charter's broadband dominance, now murmur in fractured tones—optimism unraveling like a frayed coaxial cable after the July 2025 earnings reveal.

Pre-disclosure, a Reddit thread in r/EarningsCalls noted in early 2025: "Successful management of ACP end... retaining about 90% of former ACP customers[.]" After the July 25, 2025 reveal, X feeds, though sparse on direct hits, carried undercurrents of doubt, one user warning of "worst quarter ever" for Charter, tying subscriber bleed to lingering ACP ghosts.

Reddit amplified the bite. In r/ValueInvesting, a megathread titled "Chtr shares going to 0?" drew 93 comments, blending despair—"Massive customer exodus when ACP ended"—with contrarian bets: "CHTR seems insanely cheap right now... My gut feeling says I should go all in." r/Spectrum threads piled on, one venting "Company that treats its customers terribly loses subscribers... stock plummeted," upvotes cresting at 238 as users linked churn to policy fallout and execution lapses.

Trends: Optimism eroded 35% post-lawsuit per semantic scans, but dip-buyers clawed back, a tale of retail resilience amid institutional flight.

Analyst Commentary

Wall Street's once-unified hymn to Charter's entrenched advantages—broadband moats and mobile momentum—cracked into discordant notes as ACP's aftereffects rippled through the July 2025 earnings. Through Q1, consensus clung to "Hold," 24 firms averaging $392 targets, a nod to recovery potential from $310 troughs, though murmurs grew of overdependence on subsidy-fueled adds. Pre-drop, upgrades sprinkled the landscape: Loop Capital to Buy in May at $450, invoking "fiber tailwinds"; TD Cowen holding Buy while lifting to $525 on July 29, betting on execution amid churn.

The July 25 reveal reshuffled the deck. Downgrades cascaded—Raymond James from Market Perform to Underperform; Wolfe Research from Outperform to Peer Perform, later deepening to Underperform at $300 by September, citing "persistent broadband pressures post-ACP." Wells Fargo held Equal-Weight but hiked from $260 to $350, acknowledging "lower-than-expected losses at 149,000, yet ACP drag lingers into Q4"; JPMorgan mirrored Neutral, target up to $385, balancing "mobile adds offsetting churn risks." Amid the gloom, Bernstein SocGen pierced with an upgrade to Outperform at $380 on August 1, framing "fear extreme, valuation compelling" as capex cuts promise margin juice by 2026.

Conclusion: Implications for Investors

Charter's saga whispers a broader caution: In telecom's tangled wires, federal subsidies aren't side quests—they're load-bearing beams. Investors, scanning for red flags, should probe beyond EBITDA gloss: Scrutinize subsidy dependencies in 10-K footnotes, cross-check churn metrics against macro whispers, and flag exec sales timed to upbeat calls. For fund managers, this echoes cable's twilight—pivot to mobile and fiber, or risk ACP-like cliffs in an era of beamed broadband. Optimism's fine, until the line goes dead. Watch policy pulses; they hum the real tune.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Dow Inc. (DOW) Securities Class Action Lawsuit Update [October 13, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/dow-inc-securities-lawsuit-blog-banner.webp)

![Semler Scientific, Inc. (SMLR) Securities Class Action Lawsuit [October 9, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/semler-scientific-securities-lawsuit-blog-banner.webp)

![Fly-E Group, Inc. (FLYE) Securities Class Action Lawsuit Update [October 9, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/flye-securities-fraud-lawsuit-blog-banner.webp)