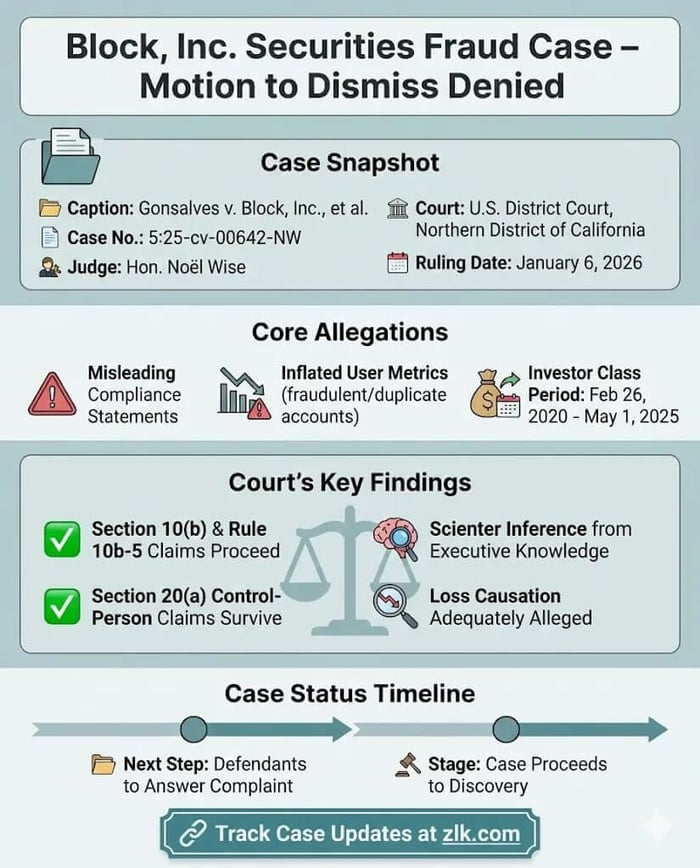

Caption: Gonsalves v. Block, Inc., et al.

Case No.: 5:25-cv-00642-NW

Jurisdiction: U.S. District Court, Northern District of California

Judge: Hon. Noël Wise

Summary

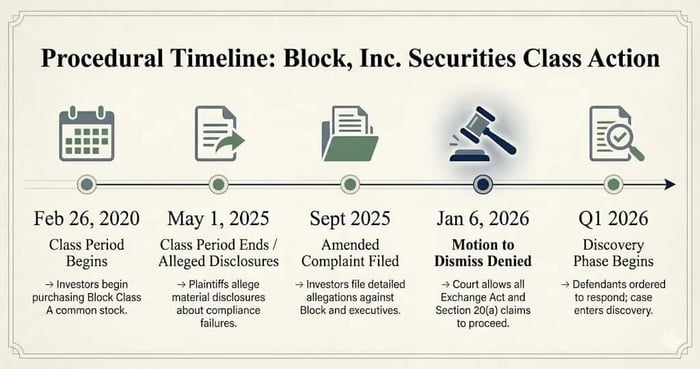

On January 6, 2026, Judge Noël Wise denied defendants’ motion to dismiss the securities class action against Block, Inc. The Court allowed all Exchange Act claims under Section 10(b) and Rule 10b-5 to proceed. Control-person claims under Section 20(a) against the individual defendants also survived.

Allegations Against Block, Inc.

Plaintiffs alleged that Block and two senior executives misled investors about Cash App’s compliance infrastructure and user metrics. The complaint said Block overstated the robustness of its compliance program while reporting user growth figures allegedly inflated by duplicate, fraudulent, or illicit accounts. Plaintiffs brought claims on behalf of investors who purchased Block Class A common stock during the class period from February 26, 2020 through May 1, 2025.

Defendants’ Motion to Dismiss

Block and the individual defendants moved to dismiss, arguing that plaintiffs failed to plead falsity, scienter, and loss causation with the particularity required by the PSLRA. Defendants contended that statements about compliance were accurate or non-actionable, that user metrics were not misleading, and that the alleged stock-price declines were not causally linked to any fraud.

Plaintiffs’ Opposition

Plaintiffs responded that the complaint identified specific misleading statements and omissions regarding compliance investment and user reporting. They argued that senior executives had access to internal information contradicting public assurances and that corrective disclosures revealed the truth to the market.

Court’s Ruling

The Court denied the motion to dismiss in full. It held that plaintiffs adequately alleged primary violations of Section 10(b) and Rule 10b-5 against Block and the individual defendants. The Court also allowed Section 20(a) control-person claims to proceed.

Court’s Rationale

Falsity: The Court found plaintiffs plausibly alleged that statements about compliance programming and user metrics were misleading when viewed in light of alleged deficiencies and undisclosed fraudulent accounts.

Scienter: The Court held that allegations regarding executives’ roles, access to internal information, and the prominence of user metrics supported a strong inference of scienter.

Loss Causation: The Court concluded that plaintiffs sufficiently tied alleged corrective disclosures to subsequent stock-price declines.

Section 20(a): The Court found allegations of control by the individual defendants sufficient at the pleading stage.

Case Status

The motion to dismiss was denied. Defendants must answer the amended complaint, and the case proceeds into discovery.