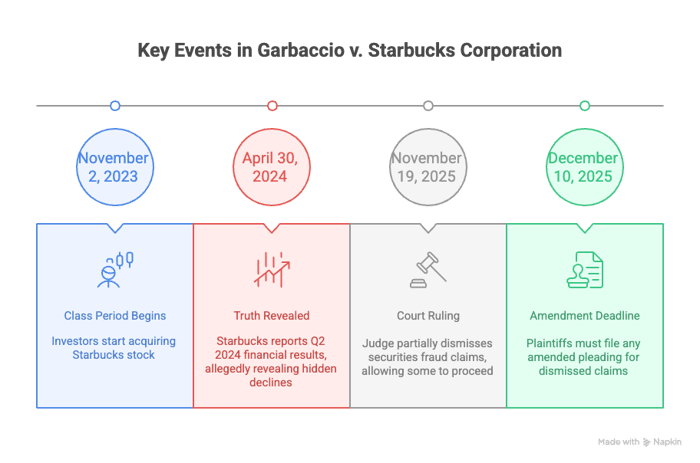

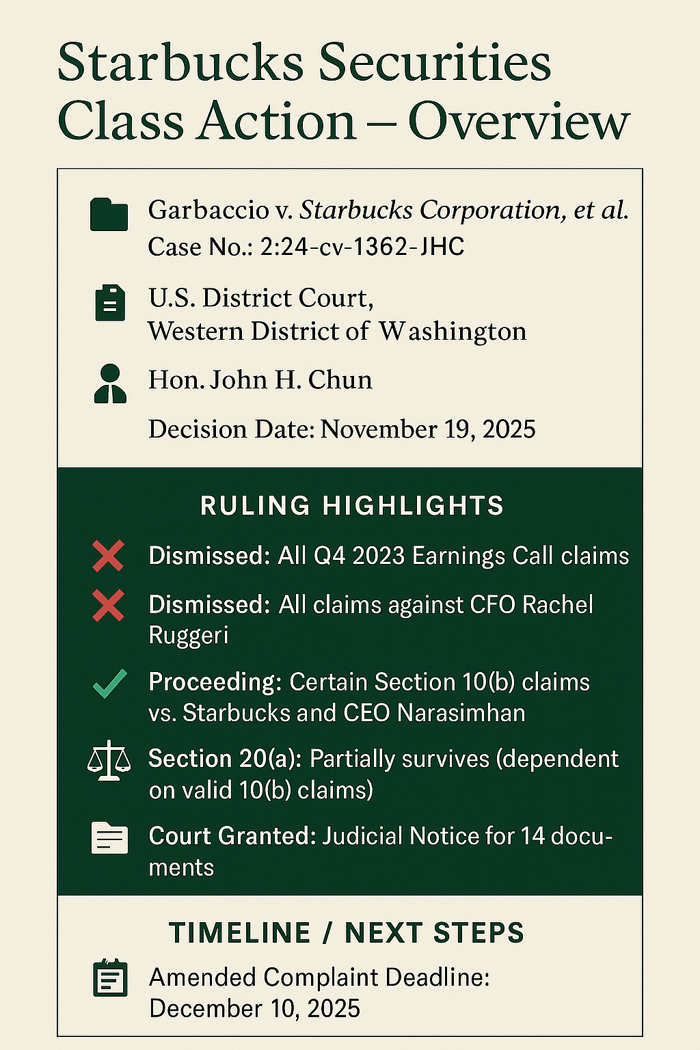

Caption: Garbaccio v. Starbucks Corporation, et al.

Case No.: 2:24-cv-01362-JHC

Jurisdiction: U.S. District Court, Western District of Washington

Judge: Hon. John H. Chun

Summary

On November 19, 2025, the Court granted in part and denied in part Defendants' Motion to Dismiss the Consolidated Complaint in the securities class action. The Court dismissed all claims based on statements from the Q4 2023 Earnings Call and most challenged statements from the Q1 2024 Earnings Call. However, the Court allowed certain Section 10(b) claims to proceed. All claims against Defendant Rachel Ruggeri, the CFO, were dismissed. The Court granted Plaintiffs leave to amend the dismissed claims.

Allegations Against Starbucks Corporation

Plaintiffs, investors who acquired Starbucks common stock during the Class Period (November 2, 2023, and April 30, 2024), brought claims under Sections 10(b) and 20(a) of the Securities Exchange Act of 1934 and SEC Rule 10b-5. The complaint alleged a concerted effort by the Defendants to hide that store traffic and transactions in the United States and China were declining. Plaintiffs said Defendants made numerous false and misleading statements and omissions during the Class Period. The relevant truth was allegedly revealed on April 30, 2024, when Starbucks reported its Q2 2024 financial results.

Defendants’ Motion to Dismiss

Starbucks and the individual defendants, former CEO Laxman Narasimhan and CFO Rachel Ruggeri, moved to dismiss the Complaint in its entirety for failure to state a claim. They argued the Complaint failed to satisfy the exacting requirements for pleading securities fraud. Specifically, they contended Plaintiffs failed to plead (1) facts establishing a materially false or misleading statement (falsity), (2) a strong inference of scienter, and (3) loss causation. Defendants also argued that all challenged statements were either accurate reports of historical results, nonactionable opinions, corporate optimism, or protected forward-looking statements.

Plaintiffs’ Opposition

Plaintiffs responded that the Complaint plausibly alleged all six elements of a claim for securities fraud under Section 10(b). They countered that the Complaint adequately pleaded falsity, scienter, and loss causation because each of the challenged statements was an actionable misrepresentation.

Court’s Ruling

The Court dismissed certain Section 10(b) claims without prejudice but found other Section 10(b) claims to be adequately pleaded and allowed them to proceed.

- Claims Dismissed: The Court dismissed all claims related to the challenged statements from the Q4 2023 Earnings Call. Claims against CFO Rachel Ruggeri were dismissed in their entirety.

- Claims Surviving: Certain Section 10(b) claims against the Company and CEO Narasimhan survived the pleading stage.

- Derivative Claims: Control-person claims under Section 20(a) were dismissed without prejudice only to the extent they hinged on the dismissed Section 10(b) claims. The remaining Section 20(a) claims survive based on the validly pleaded primary claims.

Court’s Rationale

- Falsity: The Court found Plaintiffs failed to plead a material misrepresentation for all Q4 2023 Earnings Call statements. The challenged China Business Statements were nonactionable because they constituted "generalized, vague and unspecific assertions." The Court found Plaintiffs adequately pleaded falsity only with respect to the Q1 2024 Form 10-Q Risk-Disclosure Statement and certain Q1 2024 Earnings Call statements.

- Scienter/Loss Causation: The Section 10(b) claims that survived the falsity analysis were also found to be adequately pleaded as to scienter and loss causation.

- Section 20(a): The Court declined to dismiss Section 20(a) control-person claims that hinged on the validly pleaded Section 10(b) claims.

- Other Issues: The Court granted Defendants’ Request for Incorporation by Reference and Judicial Notice for 14 documents, including various earnings call transcripts and SEC filings.

Case Status

The case continues in part, with certain Section 10(b) and Section 20(a) claims proceeding into discovery. Plaintiffs have leave to amend the dismissed claims and must file any amended pleading on or before December 10, 2025.