Overstated Revenue Growth Amid Visa and Permit Clampdowns

Case Name: Hickman v. Flywire Corporation, et al.

Docket Number: 1:25-cv-04110

Court: U.S. District Court, Eastern District of New York

Filing Date: July 25, 2025

Class Period: February 28, 2024 to February 25, 2025

Introduction

Flywire Corporation promised a steady ascent in the payments world, buoyed by cross-border education flows. Investors bought in. Then came the February 2025 revelations—missed earnings, slashed guidance, and admissions of deep visa-related wounds. The stock plummeted 37.36%, erasing billions in market value. Now, aggrieved shareholders claim Flywire overstated the strength and sustainability of its revenue growth while downplaying the severe impacts of tightening international student permits and visas in key markets like Canada and Australia. Ahead, we dissect the business context, misstatements, market fallout, and what it means for portfolios exposed to education-tech intersections.

Backdrop and Business Context

Backdrop and Business Context

Flywire Corporation operates as a payments-enablement and software company, facilitating transactions across borders in industries like education, healthcare, and travel. Founded in 2011 and headquartered in Boston, Massachusetts, the company went public in May 2021 via an IPO that raised $250 million, trading under FLYW on NASDAQ. Its platform connects clients—universities, hospitals, businesses—with payers worldwide, handling complex currency exchanges and compliance.

Education stands as Flywire's largest vertical, accounting for the bulk of revenue through international student tuition payments. The Americas (U.S. and Canada) and APAC (Asia and Pacific, including Australia) regions dominate, contributing over 60% of revenues in recent quarters. Milestones include acquisitions like Cohort Go in 2022 to bolster APAC presence and partnerships with global universities. Yet this setup left Flywire vulnerable. As governments in Australia and Canda imposed student intake caps starting in late 2023 and early 2024, payment volumes risked contraction. Flywire positioned itself as resilient, touting "land and expand" strategies in the U.S. and Asia-Pacific. Investors, drawn to its Rule of 40 aspirations—a SaaS metric blending growth and profitability—piled in. The alleged misconduct emerged as these policy headwinds intensified, testing the company's claims of sustainable expansion.

Promises Made vs. Reality

Flywire's executives painted a picture of robust growth, even as visa restrictions loomed. In a February 27, 2024, press release for Q4 and FY 2023 results, CEO Michael Massaro declared: "Our strong fourth quarter results, which included nearly 43% [Y/Y] growth in [RLAS], capped off an exceptional year for Flywire as we continue to show strong performance across the business . . . . We are . . . excited for what is ahead for Flywire, with a plan that puts up strong growth numbers in a complex macro environment." Then-CFO Michael Ellis downplayed Canadian caps: "Our seasonality across the fiscal year, and our results for Q1, are expected to be impacted by Canadian regulatory changes, which will reduce the number of international study permit applications and delay some Canadian applications until later in the year. The changes may also lead some students to study in other countries."

The 2023 10-K, filed February 28, 2024, warned vaguely of risks: "[G]lobal conflict and restrictions on immigration or increased limitation on the award of student visas (such as those" — but simultaneously minimized them, suggesting clients "may be adversely affected by decreases in enrollment," without quantifying the brewing storm.

Reality bit harder. By February 2025, internal pressures showed double-digit visa declines across major markets. The gap widened: promises of low-20% FX-neutral RLAS growth for FY 2025 crumbled to 10-14%, exposing the fragility beneath the optimism.

Timeline of Alleged Misconduct and Disclosures

Class Period: February 28, 2024 – February 25, 2025

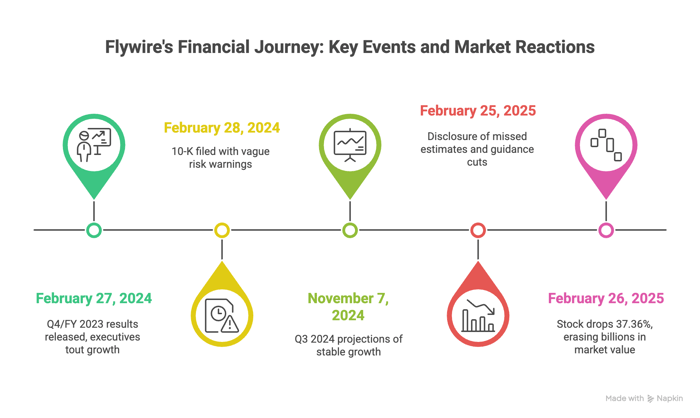

- February 27, 2024: After-market optimism. Q4/FY 2023 results released, touting "nearly 43% [Y/Y] growth in [RLAS]" and "strong performance across the business." Massaro hails sustainable growth in a "complex macro environment"; Ellis minimizes Canadian permit caps as mere seasonality shifts.

- February 28, 2024: 10-K filed, SOX-certified by Massaro and Ellis. Vague warnings recycle enrollment risks, downplaying visa restrictions as potential "decreases in enrollment," without quantifying impacts from known Canadian and Australian policies.

- November 7, 2024: Q3 2024 salvo—press release, earnings call, and 10-Q. Executives project FY 2025 FX-neutral RLAS growth in "the low 20s . . . plus," with Canada "relatively flat" and Australia showing "early moderation." Pitigoi affirms Rule of 40 status; analysts note contrast to emerging headwinds.

- February 25, 2025: The unraveling. Q4/FY 2024 results miss estimates—$0.12 loss per share and $117.6M revenue. Massaro blames "significant headwinds"; Pitigoi slashes guidance to 10-14%, revealing over-30% Y/Y drops in Canada and Australia. Call exposes "double digit declines in student visa issuance."

- February 26, 2025: Market backlash. Shares crater 37.36% to $11.05. Analysts downgrade en masse—Goldman Sachs to Neutral, citing "unexpected" cuts; multiple firms highlight "sharp contrast" to prior flat Canada claims.

Investor Harm and Market Reaction

Losses mounted swiftly. The news on February 26, 2025 caused shares to tumble 37.36% from $17.64 to $11.05. Investors who bought at Class Period highs—around $30 in mid-2024—faced 60%+ erosion. Analyst downgrades amplified the pain: Goldman Sachs shifted from Buy to Neutral on February 27, 2025, citing "unexpected" guidance cuts. Multiple firms slashed price targets, noting contrasts with prior flat Canadian growth claims; one report highlighted "sharp contrast to Defendants’ prior representations." Market sentiment soured—trading volume spiked 500% post-disclosure, with short interest rising as bears piled on. Broader indices dipped modestly, but FLYW's outsized fall tied directly to the visa admissions. For institutional holders, the harm echoes in diluted portfolios; retail investors, drawn by SaaS hype, bore acute losses. Each inflection—earnings miss, call revelations—triggered waves of selling, underscoring loss causation in the suit.

Litigation and Procedural Posture

The complaint asserts Section 10(b) and Rule 10b-5 claims for false statements, plus Section 20(a) for control-person liability against executives Michael Massaro (CEO), Cosmin Pitigoi (CFO from March 2024), Michael Ellis (prior CFO), and Rob Orgel (President/COO). Scienter allegations hinge on knowledge of headwinds such as executives accessed real-time payment data yet touted growth, bolstered by insider sales totaling over $5.7 million: Massaro offloaded 852,126 shares for $4.67 million, Orgel sold 46,096 for $1.05 million.

Procedural steps: Filed July 25, 2025; lead plaintiff motions due soon, with potential consolidation. Defendants will likely move to dismiss, arguing warnings in filings sufficed. Venue is in the Eastern District of New York. Milestones ahead include class certification, where reliance and commonality will be tested. For counsel, the case fits classic post-disclosure patterns, with strong loss causation from the 37.36% drop.

Shareholder Sentiment

Across platforms like X (formerly Twitter), Reddit, and Stocktwits, Flywire shareholders vented frustration post-February 2025 drop. Sentiment shifted from cautious optimism to outright betrayal. On X: "FLYWIRE 96 HOUR DEADLINE ALERT... Remind Investors With Losses in Excess of $100,000 of Deadline in Class Action Lawsuit Against Flywire Corporation - FLYW." Others decried executives: "Given the horrifying waterfall price of this nightmare I don't understand why a class action lawsuit hasn't started... There's seems to be something really sketchy going on and potential fraud." Trends showed spikes in "FLYW stock drop" mentions, with pre-disclosure hope, giving way to post-drop anger. Reddit threads on r/stocks echoed this: "They knew the visa caps would tank revenues but kept promising Rule of 40." Stocktwits buzzed with bearish emojis and "bagholder" confessions, sentiment scores plunging to 20/100. Shifts were palpable: early 2024 posts praised APAC growth; by March 2025, calls for board accountability dominated, blending resignation with demands for accountability.

Analyst Commentary

Professional analysts turned skeptical after Flywire's February 25, 2025, disclosures. Goldman Sachs led with a downgrade from Buy to Neutral on February 27, 2025, slashing its price target amid "significant headwinds" in education. Pre-Class Period, coverage was bullish: in early 2024, firms like RBC and JPMorgan highlighted 40%+ RLAS growth, with targets above $35. Post-drop, downgrades cascaded—multiple reports cited "unexpected" FY 2025 guidance of 10-14% vs. prior low-20s. One analyst noted, "Flywire's forecasted FY 2025 revenue growth, particularly with respect to U.S., Canadian, and Australian markets, was unexpected and/or stood in sharp contrast to Defendants’ prior representations." Price targets fell to $12-15 ranges, with commentary focusing on visa policy risks: "Double-digit declines in student visa issuance" undercut models. Upgrades were absent; instead, holds proliferated, reflecting eroded confidence in management. Broader views tied this to SaaS sector woes, but Flywire's exposure drew unique scrutiny.

SEC Filings & Risk Factors

Flywire’s filings projected a steady course, yet the plaintiff contends they masked critical vulnerabilities tied to visa restrictions.

- February 27, 2024 press release: Unveiled Q4/FY 2023 results, with Massaro stating, "Our strong fourth quarter results, which included nearly 43% [Y/Y] growth in [RLAS], capped off an exceptional year for Flywire." Ellis noted Canadian regulatory changes as seasonal impacts.

- February 28, 2024 10-K: Highlighted education sector risks, stating "[g]lobal conflict and restrictions on immigration or increased limitation on the award of student visas (such as those" might affect enrollment, downplaying severity with broad disclaimers.

- November 7, 2024 10-Q: Reiterated stable growth, projecting FY 2025 FX-neutral RLAS in the low 20% range, with no updated risk specifics on visa caps.

- February 25, 2025 press release: Disclosed Q4/FY 2024 results, with Pitigoi revealing "[f]or our 2025 financial outlook, we project [RLAS] growth of 10-14% on an FX-neutral (constant currency) basis," citing over-30% Y/Y drops in Canada and Australia due to "recent policy changes."

Plaintiffs argue these filings omitted the depth of visa-related headwinds, concealing the true impact on revenue streams.

Conclusion: Implications for Investors

This case teaches vigilance in global-dependent SaaS plays. Red flags abound—insider sales amid rosy forecasts, vague risk language masking specifics. For similar firms in edtech or payments, it underscores diversifying beyond education verticals. Broader relevance? In a post-pandemic world, migration clamps signal volatility; investors should probe non-GAAP metrics like RLAS for hidden FX vulnerabilities. Fund managers might eye settlements, historically 2-5% of damages, but the reckoning here is personal: borders close, and trust evaporates. Flywire's story isn't over, but it reshapes how we weigh policy against promise.

![Charter Communications, Inc. (CHTR) Securities Class Action Lawsuit Update [September 30, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/charter-communications-chtr-securities-lawsuit-blog-banner.webp)

![Unicycive Therapeutics, Inc. (UNCY) Securities Class Action Lawsuit Update [September 30, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/uncy-therapeutics-class-action-blog-banner.webp)