![James Hardie Industries (JHX) Securities Class Action Lawsuit Update [November 11, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/jhx-alert-plus-banner-image.png)

Allegations of Hidden Inventory Destocking and Channel Stuffing in North America Fiber Cement

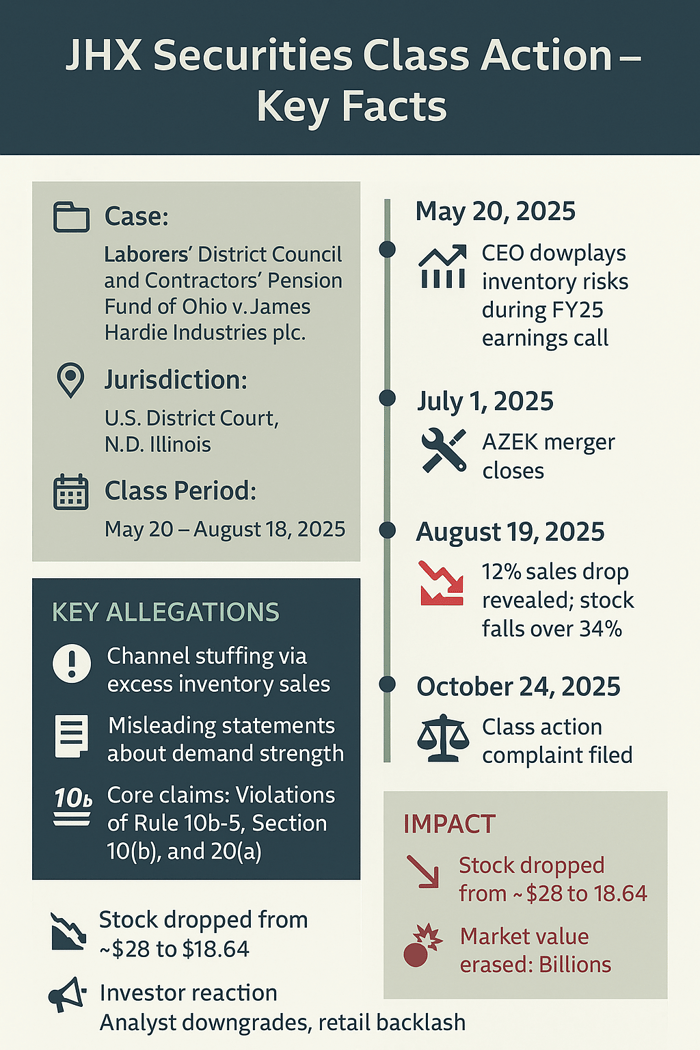

Case Name: Laborers' District Council and Contractors' Pension Fund of Ohio v. James Hardie Industries plc., et al.

Case No.: 1:25-cv-13018

Jurisdiction: U.S. District Court, Northern District of Illinois

Filed on: October 24, 2025

Class Period: May 20, 2025–August 18, 2025

Introduction

A building products giant assured the market its North American engine hummed strong. Then came the revelation—customers unloading stock piled high from earlier pushes, not fresh demand pulling sales forward. On October 24, 2025, the Laborers’ District Council and Contractors’ Pension Fund of Ohio filed a securities class action lawsuit against James Hardie Industries plc (NYSE: JHX), CEO Aaron Erter, and CFO Rachel Wilson. The complaint accuses them of misleading investors about inventory levels and demand sustainability in the company’s core North America Fiber Cement segment from May 20, 2025, through August 18, 2025. When truth surfaced on August 19, shares plunged 34%, wiping out billions in market value. Investors now grapple with what looks like classic channel stuffing masked as growth.

Backdrop and Business Context

James Hardie built its name on fiber cement siding that resists fire, rot, and termites better than wood or vinyl. North America drives roughly 80% of earnings—external siding for repairs, remodels, and new homes sold through distributors who feed dealers and big-box stores. The company prides itself on a direct-to-contractor sales force that monitors end-user demand, not just channel orders.

In March 2025, James Hardie announced a merger with The AZEK Company, closing in July for $8.4 billion. AZEK brought decking and outdoor living products; executives framed the deal as rocket fuel for cross-selling and brand dominance. Yet beneath the optimism, housing headwinds loomed—high interest rates, softening repair-remodel activity, election-year uncertainty. Distributors, sensing slowdown, began destocking as early as April. That detail stayed buried until it erupted.

Promises Made vs. Reality

On May 20, 2025, during the FY25 Q4 earnings call, CEO Aaron Erter painted resilience: “Our full-year business results demonstrate the inherent strength of our unique value proposition and the underlying momentum in our strategy against a softer market environment.”

An analyst pressed directly on destocking risks. Erter pushed back: “[I]n general, I would say that we are seeing, you know, normal stock levels out there, you know, just as a general statement.” CFO Rachel Wilson added caution but no alarm: “We are seeing performance in at the for the months to date as we would expect. But, look, we're gonna be a little cautious out there, and our guidance is reflective of that. But, again, we are performing very much to our plan.”

The next day’s press release doubled down: North America “outperforming its end markets” with “significant material conversion opportunity” and investments positioning the company “well to capitalize as the market returns to growth.”

Reality, per the complaint, diverged sharply. Defendants already knew distributors were shedding inventory acquired in March amid post-election growth hopes. Sales looked robust only because channels had overstocked—not because homeowners or builders suddenly craved more siding. By denying any such problems, executives allegedly concealed a classic red flag: growth pulled forward, destined to reverse.

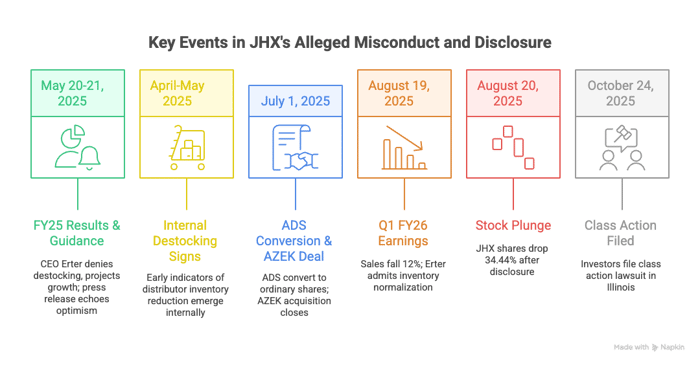

Timeline of Alleged Misconduct and Disclosures

Class Period: May 20, 2025 – August 18, 2025, inclusive.

- May 20-21, 2025: FY25 results and guidance. Erter denies destocking; company projects low single-digit North America growth for FY26.

- April-May 2025 (internal): First signs of destocking emerge, yet public commentary stays upbeat.

- July 1, 2025: ADS convert to ordinary shares; AZEK deal closes (press release).

- August 19, 2025: Q1 FY26 earnings. North America Fiber Cement sales fall 12%. Erter admits “normalization of channel inventories due to moderating growth expectations… as uncertainty built throughout April and early May.” He timelines the shift: defensive postures intensified in June-July.

- August 20, 2025: JHX closes at $18.64, down $9.79 or 34.44% in a single session.

- October 24, 2025: Class action filed in Northern District of Illinois (Case No. 1:25-cv-13018).

Investor Harm and Market Reaction

The August 19 disclosure triggered immediate carnage. Volume spiked; $9.79 per share evaporated overnight. For a company trading around $28 pre-news, the drop erased over almost a third of per share value. Funds holding JHX—pension plans, ETFs, active managers—felt the sting across portfolios tilted toward materials and housing. Broader sector sentiment soured; peers like Trex and Azek dipped in sympathy as investors questioned channel health industry-wide.

Litigation and Procedural Posture

Filed as Laborers’ District Council v. James Hardie Industries plc., Case No. 1:25-cv-13018 (N.D. Ill.). Claims: violations of Section 10(b), Rule 10b-5, and Section 20(a) of the Exchange Act. Defendants: the Company, CEO Aaron Erter, and CFO Rachel Wilson.

Scienter rests on the core-business nature of North America (80% earnings) and executives’ direct access to channel inventory data. No confidential witnesses cited—yet—but the complaint leans on Erter’s own August timeline contradicting May denials. Presumption of reliance via fraud-on-the-market; efficient market alleged through NYSE listing and regular SEC filings. Early stage: complaint just filed, no motion to dismiss yet.

Shareholder Sentiment

Retail trenches lit up post-disclosure. On X, frustration boiled over, with one user declaring: “Just not great shareholder relations behavior [...] JHX/mgmt has a long way to go to restore credibility & prove the AZEK transaction was a smart one.”

Reddit’s r/wallstreetbets and r/stocks threads echoed this feeling of betrayal. Stocktwits noted “[t]he company posted adjusted earnings of $0.29 per share, compared with the average analysts’ estimate of $0.35 per share for the fiscal first quarter[.]” While some defended the nature of cyclical businesses in online commentary, most didn’t buy it—outrage centered on the May denial when execs already saw April cracks.

Analyst Commentary

Pre-disclosure, coverage glowed. Post-August 19, axes fell fast. MST Financial grilled Erter on the call: “So the destocking into the second half of the quarter must have been quite severe.” UBS downgraded to Neutral, slashing target from $42 to $24: “Inventory normalization risk understated; visibility poor into H2.” Consensus target dropped 28% in a week. Jefferies lowered the stock price target to $30 from $34, calling Q1 results softer than expected and FY26 guidance "much weaker than expected" due to destocking and construction downturn.

SEC Filings & Risk Factors

The May 20, 2025 Form 20-F (annual report) warned generically that changes in customer inventory levels may affect demand for products and that distributors may increase or decrease inventory… impacting short-term results.

Yet the same filing boasted active monitoring: “support directly to the customers of these distribution channels” and “maintain[ing] relationships with national and other major accounts.” Risk factors never elevated destocking to material probability despite April signals. The August 19 6-K (earnings release equivalent) finally admitted the issue but claimed prior disclosure—analysts disagreed.

Conclusion: Implications for Investors

James Hardie teaches a hard lesson in distribution-dependent names. When 80% of profit flows through third-party channels, “normal stock levels” isn’t casual commentary—it’s a material assertion. Executives who monitor end demand yet dismiss destocking signals invite scrutiny. For funds chasing housing recovery, the case underscores why gross order growth alone misleads; watch days-of-inventory at distributors like a hawk.

Broader resonance hits building products, autos, consumer durables—any sector prone to pull-forward. In a macro fog of rates and elections, companies that stuff channels to hit numbers eventually pay. Investors burned here now watch peers for similar cracks. The fightback begins in Chicago federal court. Those who held JHX through summer learned: siding may endure. Stories about demand sometimes don’t.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Synopsys, Inc. (SNPS) Securities Class Action Lawsuit Filed [November 7, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/snps-banner-image.png)

![CarMax, Inc. (KMX) Securities Class Action Lawsuit Filed [November 7, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/banner.png)

![Avantor, Inc. (AVTR) Securities Class Action Update [November 11, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/banner.webp)