![Avantor, Inc. (AVTR) Securities Class Action Update [November 11, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/banner.webp)

Avantor Overstated Its Strength and Hid Setbacks, Costing Investors Millions

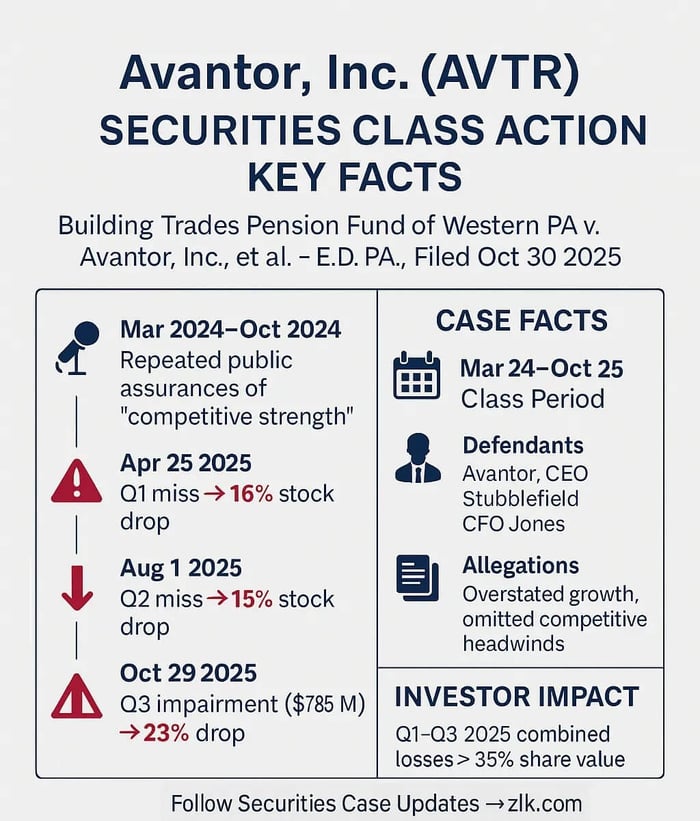

Case Name: Building Trades Pension Fund of Western Pennsylvania v. Avantor, Inc., et al.

Case No.: 2:25-cv-06187

Jurisdiction: U.S. District Court, Eastern District of Pennsylvania

Filed on: October 30, 2025

Class Period: March 5, 2024 - October 28, 2025

Introduction

The company Avantor, Inc. (NYSE: AVTR) is at the center of a securities class action. According to the complaint, investors allege that management misled the market about Avantor’s competitive strength, growth trajectory, and operational risk. The complaint asserts that the difference between public statements and actual performance triggered sharp stock drops, investor losses, and legal exposure. For investors and fund managers, the case highlights key questions around forecasting risk, internal controls, and red flags for life-sciences tool companies. This article maps the allegations, business backdrop, timeline of disclosures, investor impact, and litigation risks, culminating in implications across the sector.

Backdrop and Business Context

Avantor is a global provider of products and services to the life sciences, advanced technology, and research industries. The company describes itself as “a leading global provider of mission-critical products and services to customers in the life sciences and advanced technology industries” across 300,000 customer locations in 180 countries. Key business segments include Laboratory Solutions, which supplies research labs, educational institutions, government entities, and life-science customers; Bioscience Production, which services biopharmaceutical manufacturing and advanced manufacturing clients (for Q1 2025, this segment reported net sales of approximately $516.4 million, flat on an organic basis); and ancillary services and disposables tied to lab operations.

Operationally, Avantor has been undergoing portfolio adjustments. In October 2024, the company divested its Clinical Services business for roughly $650 million, expecting about $500 million in after-tax proceeds to pay down debt. The life-sciences tools sector is highly competitive, with margin pressures, capital intensity, reliance on research funding cycles, and sensitivity to policy and regulation. If a company under-discloses operational headwinds, investors may be exposed to heightened risk.

Promises Made vs. Reality

Throughout 2024 and into 2025, Avantor publicly assured investors of its strong competitive positioning, citing robust digital capabilities, market share gains, and a promising growth outlook while repeatedly downplaying or dismissing concerns about rising competition. These reassurances came in multiple forums, including earnings calls and industry conferences, with senior executives promising that Avantor would maintain or even improve its market standing.

However, internal evidence and later admissions indicated that Avantor was already struggling with intensifying competitive pressure, declining sales, pricing struggles, and lost customer accounts in key business segments. On April 25, 2025, the truth began to emerge when Avantor reported disappointing first-quarter results, cut guidance for the rest of the year, and announced the CEO’s departure—news that triggered a 16% plunge in share price as management finally acknowledged the negative impact of competition on the company’s performance.

The negative trend continued on August 1, 2025, with another quarterly miss, further guidance reductions, and a stock drop of 15%. The situation culminated on October 29, 2025, when Avantor disclosed poor third-quarter results, a $785 million goodwill impairment attributed to ongoing margin pressures and lost contracts, and a sharp 23% decline in stock value.

Each disclosure not only contradicted the company’s earlier upbeat communications but also revealed that many of Avantor’s glowing public statements were without basis in the actual internal data known to management at the time. As these misstatements were corrected and the full extent of the competitive difficulties made public, Avantor’s investors suffered millions in losses, leading to class action litigation and widespread scrutiny of the company’s disclosure practices.

Timeline of Alleged Misconduct and Disclosures

From the Class Period of March 5, 2024 – October 28, 2025, here is a timeline of relevant events:

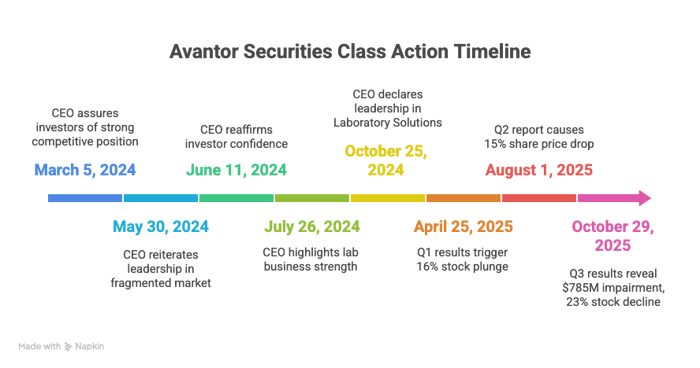

- March 5, 2024: CEO Michael Stubblefield assured investors at the TD Cowen Healthcare Conference that Avantor’s competitive position was strong, stating that “we continue to have confidence in the positioning [of] a lot of investments in our digital capabilities there to make it more efficient for our customers to engage with us,” promising that “the traffic to our sites relative to our competitors is a nice indicator for our business.”

- May 30, 2024: The Sanford C. Bernstein Strategic Decisions Conference, Stubblefield made these assurances again: “We're going to be the leader [...]. It's a very fragmented space [...] we have a differentiated platform that, at least over the 10 years that I've been here, has outgrown the broader market by 300 to 400 basis points consistently.”

- June 11, 2024: During the Goldman Sachs Healthcare Conference, Stubblefield reassured investors yet again.

- July 26, 2024: At the Q2 earnings call, Stubblefield stated, "Our lab business stacks up well [...].”

- October 25, 2024: In the Q3 earnings call, Stubblefield represented, "Avantor is clearly a leader in the Laboratory Solutions market [...]."

- April 25, 2025: The company posted Q1 results showing net sales of $1.58 billion (−6%) and Lab Solutions net sales down 8% (organic −3%), which caused a stock price drop of roughly 16.5%.

- August 1, 2025: Avantor’s lackluster Q2 report triggered an estimated ~15% share price drop.

- October 29, 2025: Q3 results revealed a massive goodwill impairment of around $785 million, resulting in an approximate 23% stock decline.

Investor Harm and Market Reaction

Investor harm was significant following key corrective disclosures by Avantor in 2025. On August 1, 2025, after reporting disappointing Q2 results and reducing full-year guidance, Avantor's stock price fell sharply by approximately $2.08 per share or more than 15%, closing at $11.36 from $13.44 the previous day. This decline reflected growing investor concern over continued competitive pressures and weak financial performance.

The negative trend worsened on October 29, 2025, when Avantor reported weak Q3 results, including a $785 million goodwill impairment and margin pressures linked to lost large accounts, causing a further stock drop of about $3.50 per share or over 23%, closing at $11.58 from $15.08 the prior session.

These substantial price declines illustrate the material shareholder losses stemming from prior overly optimistic management statements and the delayed revelation of the company’s deteriorating business conditions.

Litigation and Procedural Posture

The Eastern District of Pennsylvania filing names Avantor, Inc., CEO Stubblefield and CFO Jones as defendants for 10(b), Rule 10b-5, 20(a) violations. The complaint alleges that executives knew or recklessly disregarded the truth of operational weakness and competitive erosion, yet publicly painted a more favorable picture.

Since the class period encompasses multiple disclosures, the case may involve complex issues of both misstatement (falsity) and omission (failure to disclose material risks), as well as causation and scienter — all hot spots in securities fraud litigation.

Shareholder Sentiment

Investor sentiment surrounding Avantor, Inc. shifted markedly during the class‑period in response to operational missteps, disclosure surprises, and activist intervention. On public forums such as Yahoo! Finance, the general tone shifted from cautious optimism to heightened concern as the company’s weakness became evident.

In the wake of the company’s disappointing third‑quarter results (e.g., the August 11, 2025 disclosure of activist investor Engine Capital taking a stake and calling for board changes), the sentiment among institutional and retail investors turned decidedly more critical. Engine Capital’s public letter accused Avantor of “self‑inflicted” value destruction, citing cost control failures, turnover and underperformance.

The overall shareholder trend went from initial credibility in management’s story, to disappointment at execution, to distrust in narrative transparency. For class-action practitioners, this shift matters: it signals that the “reasonable investor” may have reacted to the corrective disclosures, strengthening the link between misstatement and price drop.

Analyst Commentary

Professional analysts downgraded Avantor following weak quarterly results, particularly in Laboratory Solutions, and highlighted challenges in education/government lab demand. The company’s cost-transformation goal of $400 million in gross run-rate savings by the end of 2027 was noted as ambitious. Analysts flagged that the decline in the legacy Lab Solutions business undermined Avantor’s positioning in bioprocessing and advanced manufacturing.

For institutional investors, the combination of analyst downgrades plus rising short interest (reported in public filings) adds to the narrative of eroded confidence and raises the cost of capital. From a securities-litigation vantage, analyst commentary can help establish loss-causation — showing that third-party market participants connected the disclosed bad news to valuation decline.

SEC Filings & Risk Factors

Avantor’s Q1 2025 10-Q highlighted the use of non-GAAP measures, and the 2024 10-K included generic risk factors, such as potential declines in government/academic research spending, intense competition, and impairment of goodwill or intangible assets. The class-action complaint alleges that these risks manifested materially before they were disclosed publicly.

Conclusion: Implications for Investors

This case underscores several lessons. Narrative matters, but transparency and execution matter more. Segment-level disclosure is critical, and risk-factor boilerplate cannot replace material updates. For Avantor, the decline in the Laboratory Solutions business (−8% sales in Q1) and headwinds in education/government labs were early warning signs.

Analyst and sentiment-shifts offer valuable signals. When analyst downgrades mount and retail sentiment flips, the market is often ahead of management in re-rating risk. For class-action counsel, those signals can help link disclosure to price reaction.

Litigation risk remains. While this Avantor case is specific, it reminds investors that when management narrative diverges from internal reality, the risk of a securities class action increases — disclosure gaps, timing mismatches and material surprises are triggers.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![James Hardie Industries (JHX) Securities Class Action Lawsuit Update [November 11, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/jhx-alert-plus-banner-image.png)

![Synopsys, Inc. (SNPS) Securities Class Action Lawsuit Update [November 11, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/snps-alert-plus-banner-image-v2.png)

![DexCom, Inc. (DXCM) Securities Class Action Lawsuit Update [November 11, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/dxcm-alert-plus-banner.webp)