![Synopsys, Inc. (SNPS) Securities Class Action Lawsuit Update [November 11, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/snps-alert-plus-banner-image-v2.png)

Unpacking the Allegations of Misled Investors in AI-Driven Design IP Woes

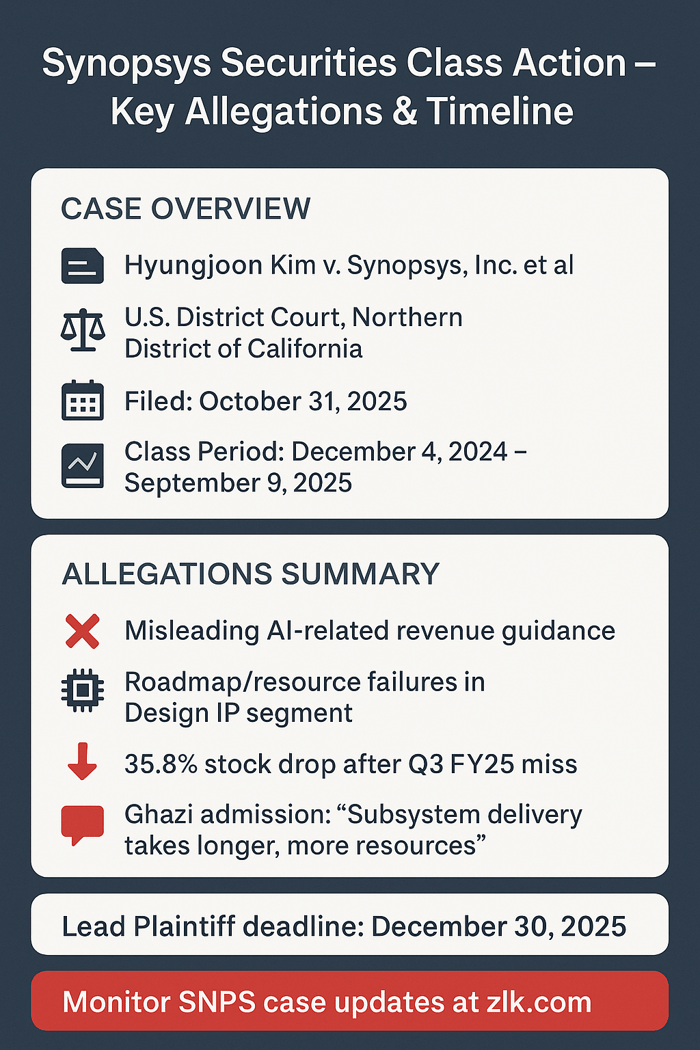

Case Name: Kim v. Synopsys, Inc. et al

Case No.: 3:25-cv-09410

Jurisdiction: U.S. District Court, Northern District of California

Filed on: October 31, 2025

Class Period: December 4, 2024 - September 9, 2025

Introduction

Synopsys, Inc. said its Design IP segment was thriving amid the AI boom. It wasn’t. Investors who bought in, drawn by promises of double-digit growth, watched shares crater when the truth emerged. This securities class action lawsuit, filed in the Northern District of California, accuses the company of concealing how its pivot to customized AI solutions was eroding profitability. The fallout: a 35.8% stock plunge, wiping out billions in market value. For fund managers eyeing tech recoveries and counsel building class claims, the case spotlights red flags in high-growth narratives. Here, the story unfolds—allegations, timelines, and what it means for portfolios.

In the Northern District of California, under Case No. 3:25-cv-09410, investor Hyungjoon Kim has filed a class action complaint against Synopsys, Inc. (ticker: SNPS), alleging violations of federal securities laws. The class period spans December 4, 2024, to September 9, 2025, a window where the company’s stock rode high on AI optimism before collapsing. Key defendants include CEO Sassine Ghazi and CFO Shelagh Glaser, accused of misleading statements that masked deteriorating economics in the fast-growing Design IP segment.

The core allegations: Synopsys failed to disclose how its increased focus on AI customers—demanding heavy customization—was undermining the segment’s profitability. This led to “certain road map and resource decisions” that fell short, triggering a material negative impact on results. Investors claim positive guidance lacked basis, inflating shares until a Q3 2025 earnings miss exposed the cracks. The stock dropped $216.59, or 35.8%, on September 10, 2025, following the disclosure.

For investors, the case raises questions of scienter and loss causation, potentially leading to recoveries.

Backdrop and Business Context

Synopsys operates at the heart of semiconductor innovation, providing electronic design automation (EDA) software and intellectual property (IP) that engineers use to create and test integrated circuits. Founded in 1986 and headquartered in Sunnyvale, California, the company went public in 1992, evolving from a niche player to a $60 billion-plus market cap giant by mid-2025. Its two main segments—Design Automation and Design IP—cater to chipmakers like Nvidia and Intel, enabling faster, cheaper production of complex chips.

The Design IP segment, central to the lawsuit, supplies pre-designed, silicon-proven components for building System-on-Chips (SoCs). This includes Interface IP for protocols like USB and PCIe, allowing semiconductor firms to integrate ready-made blocks and accelerate time-to-market. From 25% of revenue in fiscal 2022 to 31% in 2024, Design IP became Synopsys’ growth engine, fueled by the AI surge. Customers demanded more customized IP for AI accelerators, pulling resources into bespoke solutions.

Key milestones set the stage: In January 2024, Synopsys announced a $35 billion acquisition of Ansys, closing in July 2025, to expand into simulation software. Amid U.S.-China tech tensions, export restrictions disrupted deals. The company’s narrative emphasized AI tailwinds, but internally, customization demands strained margins—a risk allegedly downplayed. This backdrop frames the alleged misconduct: a high-flying tech firm where AI promises masked operational strains.

Promises Made vs. Reality

Synopsys painted a picture of robust growth, but plaintiffs argue it was a facade. In its December 4, 2024, press release for Q4 fiscal 2024 results, the company touted “record full-year 2024 revenue of $6.127 billion, up approximately 15% YoY, while improving non-GAAP operating margin and delivering approximately 25% non-GAAP EPS growth.” Guidance projected fiscal 2025 revenue at $6.745–$6.805 billion, with EPS of $10.42–$10.63, emphasizing “double digit revenue growth in 2025.”

The FY24 10-K, filed December 19, 2024, reinforced this: “Our revenues are subject to fluctuations, primarily due to customer requirements including the timing and value of contract renewals.” It warned AI initiatives “could” adversely affect the business, stating, “If we fail to develop and timely offer products with AI features [...] our business, operating results or financial condition could be adversely affected.” Operating results “may” fluctuate from product mix changes, like lower-margin hardware.

Reality, per the complaint, diverged sharply. On September 9, 2025, Synopsys issued a press release announcing third quarter 2025 financial results where it was revealed that the “IP business underperformed expectations.” Earnings calls later revealed “certain road map and resource decisions that did not yield their intended results,” driven by AI customization demands. Defendant Ghazi admitted on the September 9, 2025 call: “there’s more and more customization [...] moving from an off-the-shelf to a more subsystem delivery which is it takes longer, it takes more resources.” This pivot eroded economics, contradicting upbeat filings. Confidential witnesses aren’t cited, but earnings admissions suggest executives knew—or should have—of the mismatch.

Timeline of Alleged Misconduct and Disclosures

The narrative builds chronologically, with misstatements inflating shares until corrective disclosures triggered drops.

- December 4, 2024: Q4 FY24 results press release promises strong 2025 growth. Stock climbs amid AI hype.

- December 19, 2024: FY24 10-K filed, highlighting Design IP growth but with boilerplate risks. No specific mention of AI customization woes.

- February 26, 2025: Q1 FY25 results beat estimates; guidance reaffirmed. Press release: “Quarterly revenue of $1.455 billion, exceeding midpoint of guidance.”

- May 28, 2025: Q2 FY25 results strong; guidance intact. Revenue $1.604 billion, EPS $3.67.

- September 9, 2025: Q3 FY25 results miss: Revenue $1.740 billion vs. $1.755–$1.785 billion expected. Design IP down 7.7% YoY to $426.6 million. Ghazi admits IP underperformance due to “certain road map and resource decisions.” Guidance implies 5%+ FY25 Design IP decline. Stock falls 35.8% next day on heavy volume.

Media coverage amplified: Yahoo!Finance noted the plunge with an article headlined “Synopsys Q3 Earnings and Revenues Miss Estimates.” No prior whistleblowers surfaced, but the earnings call provided the smoking gun per the complaint.

Investor Harm and Market Reaction

The harm crystallized on September 10, 2025, with SNPS shares closing at $387.78, down $216.59 or 35.8% from $604.37—erasing over $33 billion in market cap. Trading volume spiked to 15 million shares, triple the average, signaling panic selling.

Analysts reacted swiftly: Piper Sandler downgraded to Neutral, citing geopolitical risks and concentration in volatile markets. Morgan Stanley cut its target to $510 from $715, warning of strategic risks post-China export restrictions. Pre-drop, consensus was Buy with $700+ targets; post-drop, averages fell to $450, reflecting eroded confidence.

Investors like plaintiff Kim, who bought 37 shares at $610.22 on September 8, 2025, allege losses tied directly to the disclosure. Class-wide, damages could reach hundreds of millions, given the period’s trading volume and inflation estimates.

Litigation and Procedural Posture

Filed October 31, 2025, the suit asserts Section 10(b) and Rule 10b-5 claims against all defendants for misleading statements, plus Section 20(a) against Ghazi and Glaser as controlling persons. Scienter allegations hinge on executives’ access to internal data; Ghazi’s admissions suggest knowledge of roadmap failures. No insider sales are detailed, but the complaint implies recklessness in ignoring customization impacts.

No confidential witnesses are named, but earnings quotes bolster claims. Procedural next steps: Lead plaintiff deadline December 30, 2025; motions to dismiss likely in early 2026. Fraud-on-the-market presumption applies, given NASDAQ efficiency. No significant milestones yet—this is early-stage, with potential for consolidation if more suits follow.

Shareholder Sentiment

Across X, Reddit, and StockTwits, Synopsys shareholders reeled from betrayal and scrambled for opportunity after the September 10, 2025 bloodbath—and again when class-action notices hit in early November.

On X, the initial reaction was pure shock mixed with “buy the dip” frenzy:. One user wrote “Tale of two tapes: $ORCL +35%, highest daily volume in 12 years. $SNPS -35%, highest daily volume in 8 years.” Likewise, another user asked “Now this SEEMS like an overreaction, no?? $SNPS.” Others piled in with teasing “$SNPS craters on weak IP & Ansys cost pressure [...] Buy the dip?”

On Reddit, the plunge spawned instant mega-threads on r/stocks, r/wallstreetbets, and r/investing. One r/options DD thread aged like milk overnight and became a mourning circle: My First DD: Synopsys (SNPS) Earnings.

StockTwits sentiment collapsed from ~70% bullish pre-September 9 to the low-20s% immediately after. By November, the board is split: half bagholders demanding settlements, half triumphant dip-buyers bragging about being up 25% from the bottom.

Analyst Commentary

Professional analysts viewed the Q3 fiscal 2025 earnings miss as a significant setback driven by weakness in the Design IP segment, but many maintained a long-term positive outlook on Synopsys' role in AI-enabled chip design and the Ansys integration. Pre-miss consensus was strongly Overweight/Buy; post-miss, several firms slashed targets sharply, yet the overall rating remains Moderate Buy.

Notable post-earnings moves: Piper Sandler lowered from $660 to $630 (later adjustments seen in some reports to $655), maintained Overweight. From 24/7 Wall St. was posed the key question on everyone's mind: “Synopsys Dropped 36% After Earnings: Is This an Overreaction or Buying Opportunity?” and concluded the selloff created a compelling long-term entry point. A MarketBeat headline captured the rebound narrative: “Wall Street Eyes +30% Upside in Synopsys After Huge Earnings Fall” while noting analysts cut targets by only ~14.5% vs. the stock's 36% plunge.

Overall, the commentary balanced near-term caution (China exposure, IP customization headwinds, Ansys integration costs) with conviction in Synopsys' moat and multi-year AI tailwinds. Most downgrades were price-target trims rather than rating cuts, leaving the street still bullish for patient investors.

SEC Filings & Risk Factors

Synopsys’ SEC filings during the class period included boilerplate warnings that plaintiffs deem inadequate. The FY24 10-K (December 19, 2024) stated: “We may not be successful in our AI initiatives, which could adversely affect our business,” noting failure to integrate AI could lead to obsolescence. It added operating results “may fluctuate” from “changes in the mix of our products sold,” like lower-margin hardware.

Q1 2025 10-Q (February 26, 2025) repeated: AI “could” harm if competitors outpace. Q2 2025 10-Q (May 28, 2025) echoed these. No 8-Ks flagged specific IP issues pre-drop.

Omitted risks, per suit: Extent of AI customization’s economic drag. Management warned of fluctuations from “customer requirements” but not the roadmap failures admitted later. These disclosures, plaintiffs argue, were generic, failing to alert to brewing problems—key to loss causation claims.

Conclusion: Implications for Investors

This case teaches vigilance in AI-driven sectors: Customization sounds innovative but can silently erode margins. Red flags include vague risk factors amid aggressive guidance—Synopsys’ “could” and “may” masked certainties. For similar firms like Cadence or Arm, scrutinize segment breakdowns; over-reliance on AI clients invites volatility.

Investors should monitor lead plaintiff motions; recoveries could offset losses if scienter holds. Broader lesson: In tech, where narratives drive multiples, demand transparency on resource pivots. The drop wasn’t just a miss—it was a reckoning with overhyped economics. Portfolios endure when facts precede faith.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Inspire Medical Systems, Inc. (INSP) Securities Class Action Lawsuit Filed [November 11, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/insp-banner-image.png)

![CarMax, Inc. (KMX) Securities Class Action Lawsuit Filed [November 7, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/banner.png)

![Avantor, Inc. (AVTR) Securities Class Action Update [November 11, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/banner.webp)