Medpace Holdings, Inc. Class Action Lawsuit – MEDP

|

Medpace Class Action Summary |

|

|

Company |

Medpace Holdings Inc. (NASDAQ: MEDP) |

|

Lead Plaintiff Deadline |

June 8, 2026 |

|

Class Period |

April 22, 2025 – February 9, 2026 |

|

Stock Drop |

February 10, 2026 – MEDP fell $84.30 (15.9%) to $446.05 |

|

Lawsuit Type |

Securities Class Action |

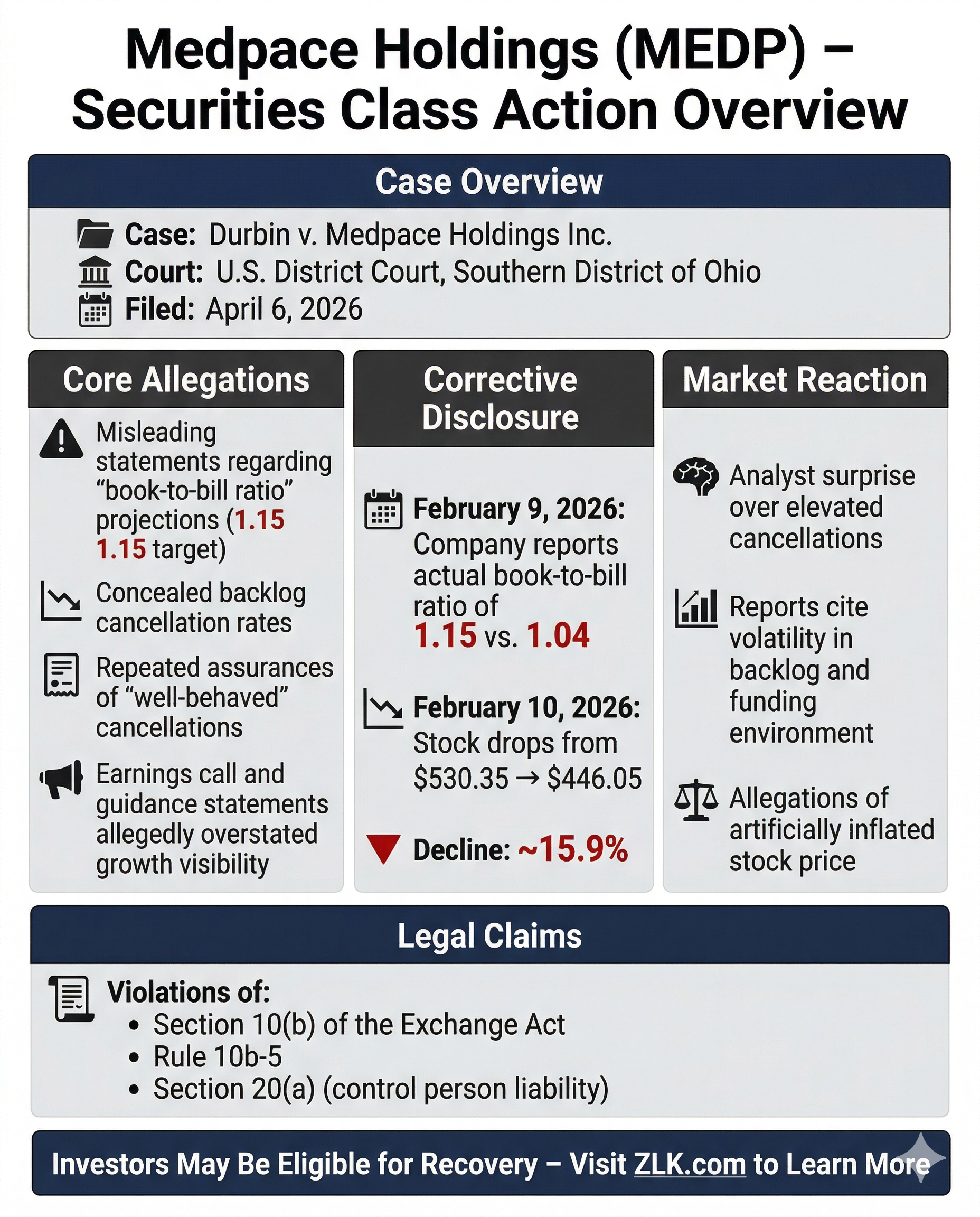

Introduction

A securities class action lawsuit has been filed against Medpace Holdings Inc. (NASDAQ: MEDP), its Chairman and CEO August James Troendle, President Jesse J. Geiger, and CFO Kevin M. Brady in the United States District Court for the Southern District of Ohio. The lawsuit, filed by plaintiff Jan Durbin and represented by Strauss Troy Co., LPA and Levi & Korsinsky, LLP, covers a Class Period from April 22, 2025 through February 9, 2026. The complaint alleges that throughout the Class Period, defendants made materially false and misleading statements regarding Medpace's projected book-to-bill ratio and backlog cancellation rates, repeatedly assuring investors that a 1.15 book-to-bill ratio for the second half of fiscal year 2025 was reasonable and achievable while concealing the true state of the Company's cancellation trends. When Medpace reported a fourth quarter 2025 book-to-bill ratio of just 1.04 on February 9, 2026, well below the 1.15 guidance, the Company's stock price plummeted from $530.35 to $446.05 per share, a decline of more than 15.9%, causing significant losses to investors who had purchased shares at artificially inflated prices.

Company Profile

Medpace Holdings Inc. is a clinical contract research organization (CRO) focused on providing scientifically-driven outsourced clinical development services to the biotechnology, pharmaceutical, and medical device industries. The Company's operating model centers on providing full-service Phase I-IV clinical development services, with its principal executive offices located in Cincinnati, Ohio.

Class Period

April 22, 2025 – February 9, 2026, inclusive.

Investors who purchased or acquired Medpace Holdings Inc. (MEDP) securities during the Class Period may be entitled to seek recovery under the federal securities laws.

Allegations

The complaint alleges that Medpace's senior leadership engaged in a sustained campaign of misleading statements about the Company's business outlook, centering on the book-to-bill ratio, a key metric that measures new business awards relative to revenue and signals future growth trajectory. Beginning with the first quarter 2025 earnings call on April 22, 2025, CEO Troendle told analysts that despite a book-to-bill of just 0.9 for Q1, there were "paths toward getting to 1.15" in the back half of the year, characterizing a downside scenario as "somewhere around 1." According to plaintiffs, these projections were made without adequate basis given the Company's deteriorating cancellation trends.

The alleged misrepresentations intensified during the second quarter earnings call on July 22, 2025, when Troendle stated the Company saw "strong potential for book-to-bills returning to above 1.15x in Q3" and described cancellations as "very well behaved[,]" noting they were "toward the lower end of expectations or usual history." The complaint alleges Troendle specifically reassured investors that the Company's challenges were "driven by cancellations, not weak business" and that the underlying business environment was "pretty okay," framing the cancellation issue as an anomaly rather than a systemic risk. Medpace raised its revenue guidance by $280 million at the midpoint during this call, further reinforcing the optimistic outlook.

By the third quarter earnings call on October 23, 2025, Medpace reported a strong 1.20 book-to-bill and record net bookings, with Troendle again describing cancellations as "well behaved." The complaint alleges that when an analyst directly asked about expectations for fourth quarter book-to-bill, Troendle reiterated that 1.15 "looks reasonable" as a Q4 target. CFO Brady described the Company's performance as "pretty broad-based" and not "isolated to a handful of studies," while Troendle acknowledged the pre-backlog was "over-indexed in metabolic" but characterized this as consistent with current trends rather than a concentration risk.

The complaint alleges defendants knew or recklessly disregarded that the therapeutic segments driving growth, particularly metabolic trials, carried elevated cancellation risk that threatened the 1.15 target. According to plaintiffs, defendants had actual knowledge of or access to non-public information about the Company's pre-backlog composition and how cancellation patterns would translate to the book-to-bill ratio, yet repeatedly conveyed an unjustifiably optimistic projection to the market.

The Truth Emerges

On February 9, 2026, after the market closed, Medpace issued a press release reporting fourth quarter 2025 results that revealed a book-to-bill ratio of just 1.04, significantly below the 1.15 guidance defendants had maintained throughout the Class Period. During the February 10, 2026 earnings call, CEO Troendle acknowledged that "cancellations were elevated again in Q4" and that "backlog cancellations in absolute and percent terms were the highest they've been in over a year," directly contradicting his repeated prior assurances that cancellations were "well behaved" and manageable. Troendle conceded that the cancellations were "a little bit skewed towards metabolic[,]" the very area that CFO Brady had previously assured investors was part of a "broad-based" growth profile rather than a concentrated risk.

The disclosures drew immediate and pointed reactions from analysts who had relied on defendants' prior guidance. Baird Equity Research published a report titled "Expect Shares Under Pressure Tomorrow," highlighting the bookings miss. Truist lowered its price target from $555 to $539, noting that "the sequential decline in B2B and the increase in cancellations came as a surprise to many investors" and characterizing the results as reflective of "the inherent volatility in its business model given its concentrated exposure, as well as the limited visibility associated with its pre-backlog." The analyst commentary underscores the degree to which the market had relied on defendants' repeated assurances about both the 1.15 target and the manageability of cancellation risk.

Market Reaction

The market reaction to Medpace's fourth quarter 2025 disclosure was swift and severe. From a closing price of $530.35 per share on February 9, 2026, MEDP shares plunged to $446.05 per share on February 10, 2026, a single-day decline of more than 15.9%, representing a loss of $84.30 per share. The magnitude of the drop reflects how deeply the market had priced in defendants' repeated guidance of a 1.15 book-to-bill ratio, and the shock of learning that backlog cancellations had reached their highest levels in over a year at the very moment defendants had projected confidence and stability.

Next Steps

● The Court will issue its order for lead plaintiff and counsel in the weeks after submissions are due.

● The Court will then consider motion for class certification.

● The Court will later consider a motion to dismiss.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

Check Eligibility

✓ No cost or obligation

✓ See if you qualify