Table of Contents

If you're a shareholder caught up in a securities class action, there's one legal move that can make or break your case before it even begins: the motion to dismiss. It might sound like just another courtroom formality, but this step is actually a big deal. If the judge agrees with it, your case could get tossed out before you even see any documents or evidence.

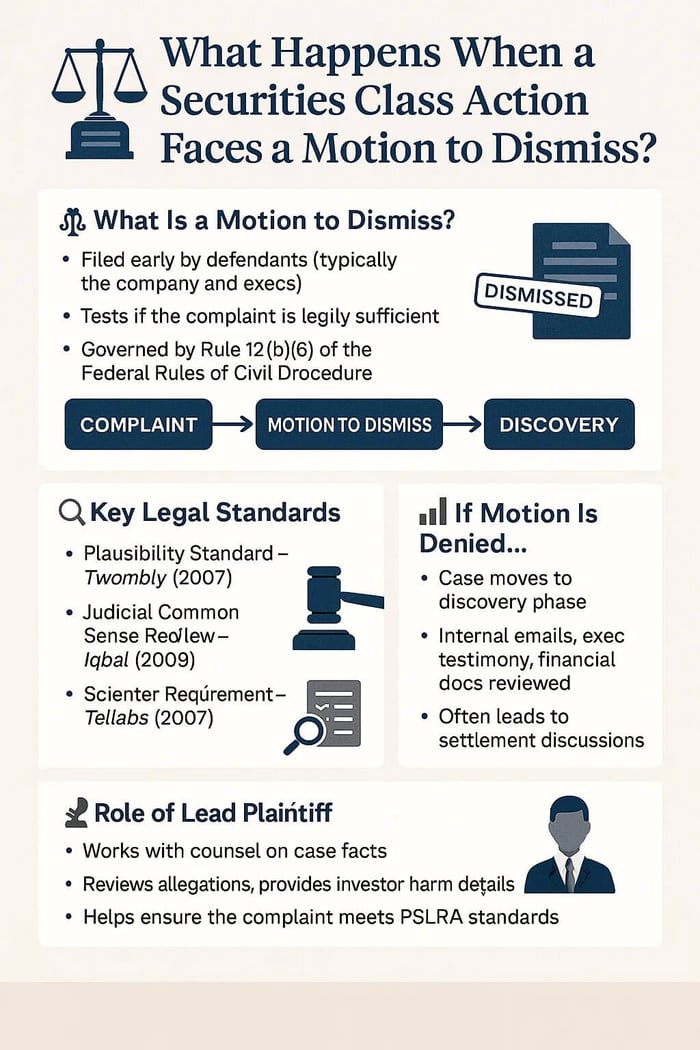

What Is a Motion to Dismiss?

A motion to dismiss is a request made by the company (and usually its top executives) asking the court to dismiss the lawsuit at the outset. Essentially, they argue that—even assuming all the allegations are true—the complaint fails to state a legally actionable claim upon which relief can be granted under the law.

At this point, the court isn’t deciding who's right or wrong. Instead, the judge reads the complaint, takes the facts as true, and asks: “Is this the kind of thing that, under the law, could even lead to a win for the investor?” This rule comes from something called Federal Rule of Civil Procedure 12(b)(6), which basically says you can’t bring a case if there’s no legal ground to stand on.

What Courts Are Looking For

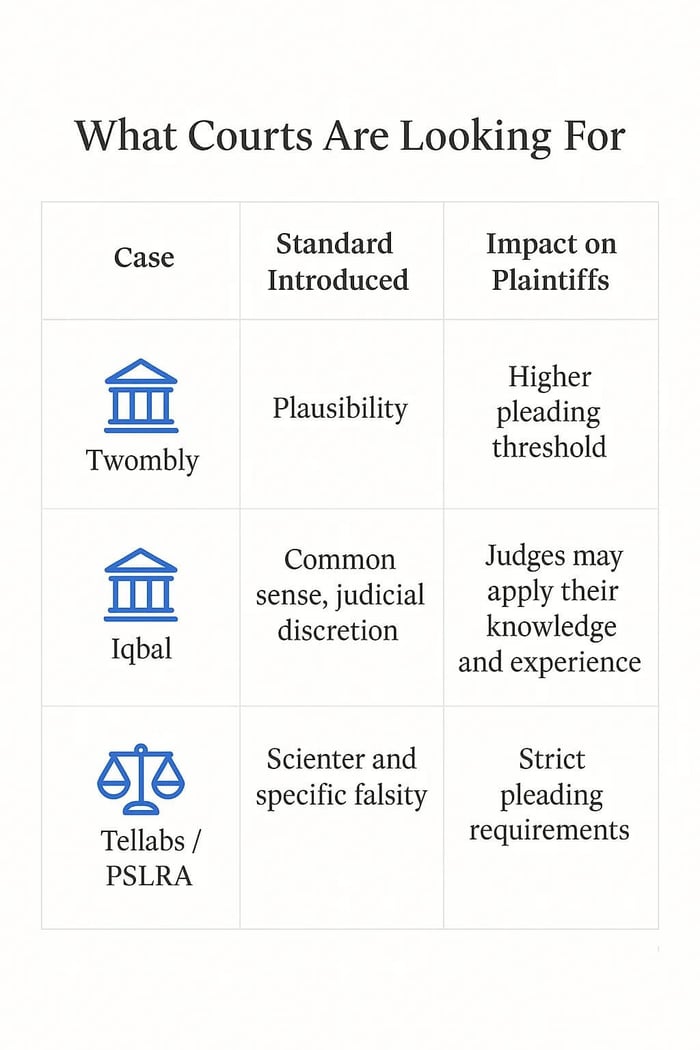

The U.S. Supreme Court has set a high bar for surviving a motion to dismiss. In Bell Atlantic Corp. v. Twombly, 550 U.S. 544 (2007), the Court introduced the “plausibility” standard, requiring complaints to include enough factual detail to show a claim is more than just possible—it must be plausible. The Court said you’ve got to do more than tell a story that might be true and that means giving enough detail to show the case could realistically go somewhere.

Then, in Ashcroft v. Iqbal, 556 U.S. 662 (2009), the Court clarified that judges should use their experience and common sense to assess whether the allegations plausibly suggest liability, rejecting claims that are too speculative or lack sufficient factual support. If something sounds too thin or far-fetched, the judge can say, “That’s not good enough.”

In securities fraud cases, the bar is even higher due to the Private Securities Litigation Reform Act (PSLRA). Investors must specify exactly what statements were false, why they were false, and provide particularized facts to support these claims (15 U.S.C. §78u-4(b)). They also have to show what’s called a “strong inference” of scienter which is that the company acted intentionally or with reckless disregard for the truth. The case Tellabs, Inc. v. Makor Issues & Rights, Ltd., 551 U.S. 308 (2007), made it clear: vague or conclusory accusations are not enough.

That’s why so many of these cases don’t make it past this early stage.

Two Real Cases That Got Dismissed

1. Janus Capital Group v. First Derivative Traders, 564 U.S. 135 (2011)

Investors claimed Janus made false statements in mutual fund prospectuses. But here’s the twist: the Supreme Court said those statements weren’t technically made by Janus itself, but by a separate fund entity. Since only the one who “makes” the statement can be sued under Rule 10b-5, the case was tossed. This ruling set a pretty strict rule on who can be blamed—and Janus walked away at the motion to dismiss stage.

2. City of Livonia Employees’ Retirement System v. Boeing Co., 711 F.3d 754 (7th Cir. 2013)

This case was about Boeing and its new Dreamliner. Investors thought they were being misled about delays. But the court didn’t buy it. Why? Because the investors didn’t show strong evidence that Boeing’s execs were intentionally lying. Without that strong “scienter” (legal-speak for intent), the court dismissed the case early on.

What If the Motion to Dismiss Fails?

If the judge doesn’t dismiss the case? Then the lawsuit goes forward. That means discovery—basically the part where lawyers on both sides dig up facts, question executives under oath, and gather documents. Discovery is often where internal documents, emails, and depositions shed light on whether executives knowingly misled investors. Getting past the motion to dismiss is huge for investors. It shows the court sees at least a plausible case, and it often pressures companies to settle rather than risk a courtroom loss.

What Do Class Action Plaintiffs Do During This?

The lead plaintiff, appointed by the court under the PSLRA, plays an active role in reviewing the complaint and ensuring it reflects the facts and investor harm experienced. They work closely with lawyers to make sure the complaint includes enough solid facts and hits the legal marks. They help walk the lawyers through the timeline, explain how the statements affected them, and keep the case grounded in real-world harm.

Why This All Matters

If you’re part of a securities case—or just reading about one in a shareholder alert—understanding the motion to dismiss is key. It’s not a minor procedural step. It’s the first real legal test. If the company wins here, the case is over. But if they lose, the real battle begins. A denial of a motion to dismiss doesn’t guarantee victory, but it means the plaintiffs’ claims have passed the first legal hurdle and will proceed to discovery and potentially trial.

So, when you hear that a motion to dismiss has been denied? That’s not just legal noise. That’s the sound of investors getting a shot at justice.