Table of Contents

For most shareholders, suing a Fortune 500 company alone is intimidating and often impossible—the costs are overwhelming, and the opposing lawyers seem to have endless billable hours.

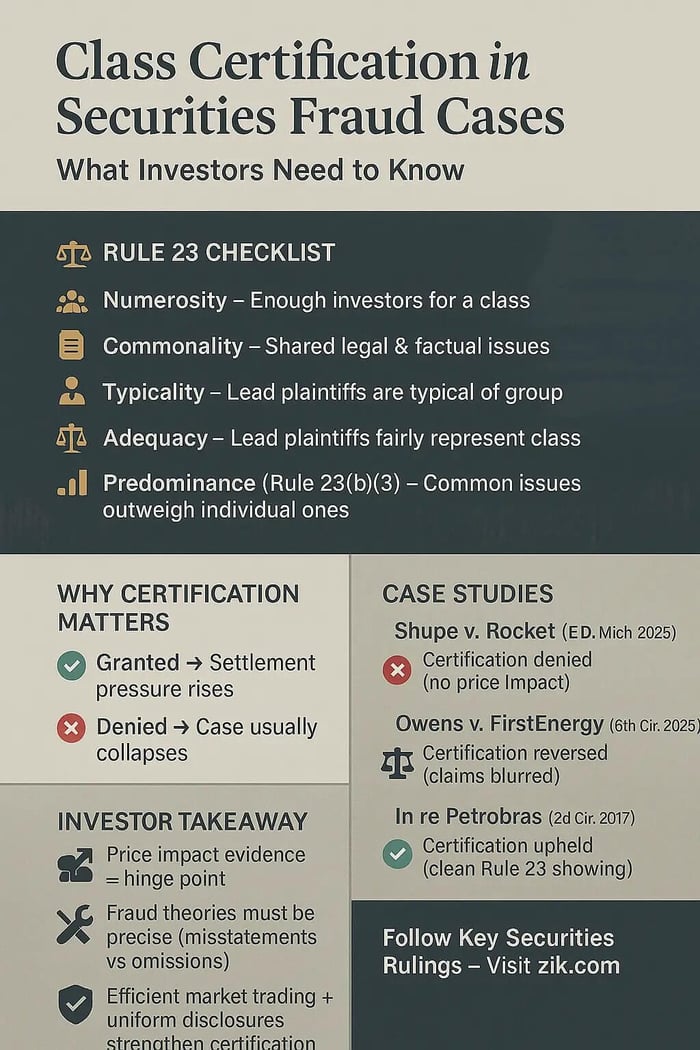

But there’s a gate you have to get through first. It’s called class certification. And courts don’t just wave you past. Plaintiffs have to prove the case fits the strict boxes of Federal Rule of Civil Procedure 23: that there are enough investors to make a class worthwhile, that they share common issues, that the lead plaintiffs are typical of the group, and that they’ll represent the class fairly. Then there’s the kicker under Rule 23(b)(3): common issues have to predominate, and treating the case as a class has to be the best option.

This step is messy. It’s often the make-or-break moment. Defendants know if certification is granted, the pressure to settle skyrockets. While plaintiffs know if it’s denied, the case is usually dead in the water.

The Rule 23 Checklist—And Why It’s Harder Here

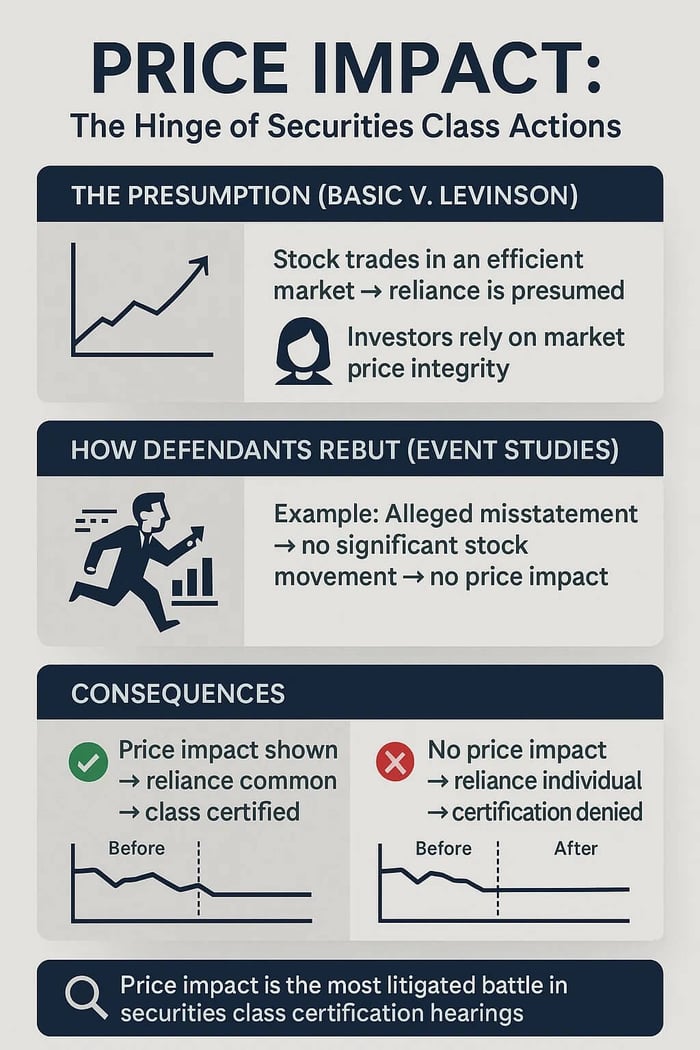

Securities fraud plaintiffs have one powerful tool: the Basic v. Levinson presumption (called the "Basic Presumption"). If a company’s stock trades in an efficient market and the alleged misstatements were public, courts assume investors rely on the integrity of the market price. In theory, that means if a misstatement inflated the stock price, every investor who bought at that price was harmed in the same way.

But “in theory” doesn’t always survive expert reports. Defendants can rebut the presumption by showing the alleged misstatements didn’t actually affect the stock price. If they succeed, reliance becomes individualized—different investors making decisions for different reasons. And once reliance splinters, predominance under Rule 23 collapses.

That’s exactly what happened in one recent case.

When Experts Rebutted the Class: Shupe v. Rocket Companies Inc.

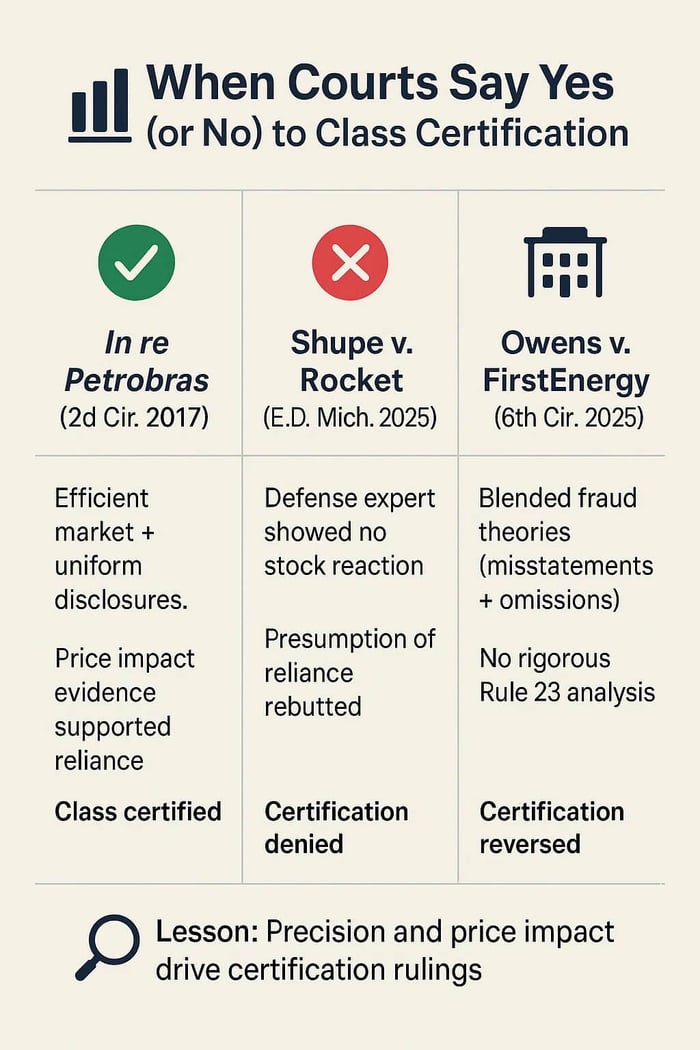

Investors accused Rocket Companies of misleading the market about its mortgage business. At first glance, it looked like a standard securities fraud class action. A large, publicly traded company. Uniform statements. A market that should have reflected those statements.

But the defendants fought back with expert testimony. Their economist ran event studies and concluded Rocket’s alleged misstatements didn’t move the stock price in a reliable way. Plaintiffs had their own expert, but the court found the defense more persuasive.

No price impact meant no common reliance. Without reliance working class-wide, Rule 23’s predominance requirement wasn’t met. The presumption from Basic fell apart. And so did the class.

Citation: Shupe v. Rocket Companies Inc., No. 21-cv-11528, 2025 WL 270890 (E.D. Mich. Feb. 4, 2025).

Takeaway: price impact is the hinge. If defendants show the stock didn’t actually respond to the alleged fraud, certification can disappear—no matter how many investors are in the room.

Case Two: Owens v. FirstEnergy Corp.

FirstEnergy’s problems went far beyond accounting. The company was caught up in a massive bribery scheme tied to Ohio lawmakers and a billion-dollar nuclear bailout. When the truth came out, shareholders sued, claiming executives misled them through both misstatements and omissions.

The district court certified the class. On appeal, the Sixth Circuit reversed.

The problem wasn’t the scale of the scandal. It was the structure of the claims. Plaintiffs treated misstatements and omissions as one blended theory, without showing how each individually satisfied Rule 23. The appellate court said that was a fatal flaw. Without a rigorous analysis separating the two, certification couldn’t stand.

Citation: Owens v. FirstEnergy Corp., No. 23-3945 (6th Cir. Aug. 13, 2025).

Takeaway: Courts want precision. Fraud theories can’t be blurred together. Each pathway—misstatements on one side, omissions on the other—has to hold up on its own terms.

When Certification Works—What Courts Look For

Most securities fraud classes actually do make it through the gate. And when they do, courts highlight the same things again and again, such as:

Efficient Market: If the stock trades on an established exchange, the presumption of reliance under Basic usually applies.

Uniform Statements: Misstatements in 10-Ks, 10-Qs, press releases, or earnings calls check the “commonality” box.

Price Impact Evidence: Courts don’t demand perfection, but they want some reliable link between the alleged fraud and market movement.

Clear Rule 23 Boxes: Numerosity, typicality, adequacy—checked cleanly, with no overreach.

One example is the Petrobras litigation. Investors alleged the Brazilian oil giant misled them during its corruption scandal. The Second Circuit upheld class certification, finding the common elements strong enough: uniform disclosures, efficient market trading, and price impact evidence that worked across the class.

Citation: In re Petrobras Sec., 862 F.3d 250 (2d Cir. 2017).

Takeaway: The difference between Petrobras and cases like Shupe or FirstEnergy is stark. Where the latter collapsed under expert challenges and fuzzy theories, Petrobras held together because the core elements of Rule 23 were met with clean, class-wide proof.

Why Denials Cut So Deep

When courts deny class certification, it doesn’t mean the fraud didn’t happen. It means the case can’t be litigated as one collective story. And for investors, that distinction is everything.

In Shupe, the denial turned on market science—the numbers didn’t show impact. In FirstEnergy, it turned on structure—the claims weren’t clearly divided. Neither ruling spoke to the underlying scandal. Both simply said: the class can’t go forward.

That leaves individual investors stranded. The losses don’t go away. The alleged misconduct doesn’t vanish. But the path to accountability closes, because few will bankroll an individual securities suit.

Why This Step Feels Like the Whole Case

If you’re not a lawyer, “class certification” sounds procedural. Technical. Almost boring. But inside securities law, it’s the battlefield. Plaintiffs line up experts. Defendants do the same. Judges parse reliance, price impact, and theories of liability in painstaking detail.

Because everyone knows: if the class is certified, settlement pressure surges. If it’s denied, the case usually collapses. The merits may never be reached. The truth may never be tested in trial.

Final Reflection—The Gate Is Real

Courts don’t treat class certification as a box to tick. They treat it as a stress test. Does the market evidence hold? Are the theories clean? Do common questions really predominate?

As Shupe, FirstEnergy, and Petrobras show, the answers can go in different directions. Sometimes the gate opens and investors walk through together. Sometimes it slams shut.

The class certification ruling can be outcome-determinative—deciding whether investors proceed collectively or whether their claims dissipate into individual suits few can afford to pursue.

FAQs

How often do appeals courts overrule a district court's class certification decision?

Somewhat often, but only if appealed and the court actually hears the appeal -- which isn't a guarantee. Different circuits also have different approaches to these appeals.

In which circuit is it easier to get class certification?

The Third Circuit (Pennsylvania, New Jersey, Delaware, and the Virgin Islands) has described itself as applying a "more liberal standard" for granting petitions to appeal, potentially making it more plaintiff-friendly for appeals (simply because more plaintiffs actually reach the Court). However, there's no evidence that the Circuit is more likely to overturn a class certification denial than is any other circuit.

What if class certification is denied?

Investors have a few choices: they can proceed individually (which might be complex and costly); they can appeal to the Circuit Court; or, they can withdraw the case.

What's the standard of proof for class certification?

The Supreme Court precedent holds courts perform a "rigorous analysis" of class certification criteria. That's thought to mean judges rule based on the "preponderance of the evidence." Under that standard, courts weigh out if it is more likely than not that the class meets the various criteria for certification. The burden of proof rests with the plaintiffs.

![Petco Health and Wellness Company, Inc. (WOOF) Securities Class Action Lawsuit Update [August 12, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/petco-securities-class-action-lawsuit-blog-banner.webp)

![XPLR Infrastructure (XIFR) Securities Class Action Lawsuit Update [August 18, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/xplr-infrastructure-xifr-lawsuit-blog-banner.webp)