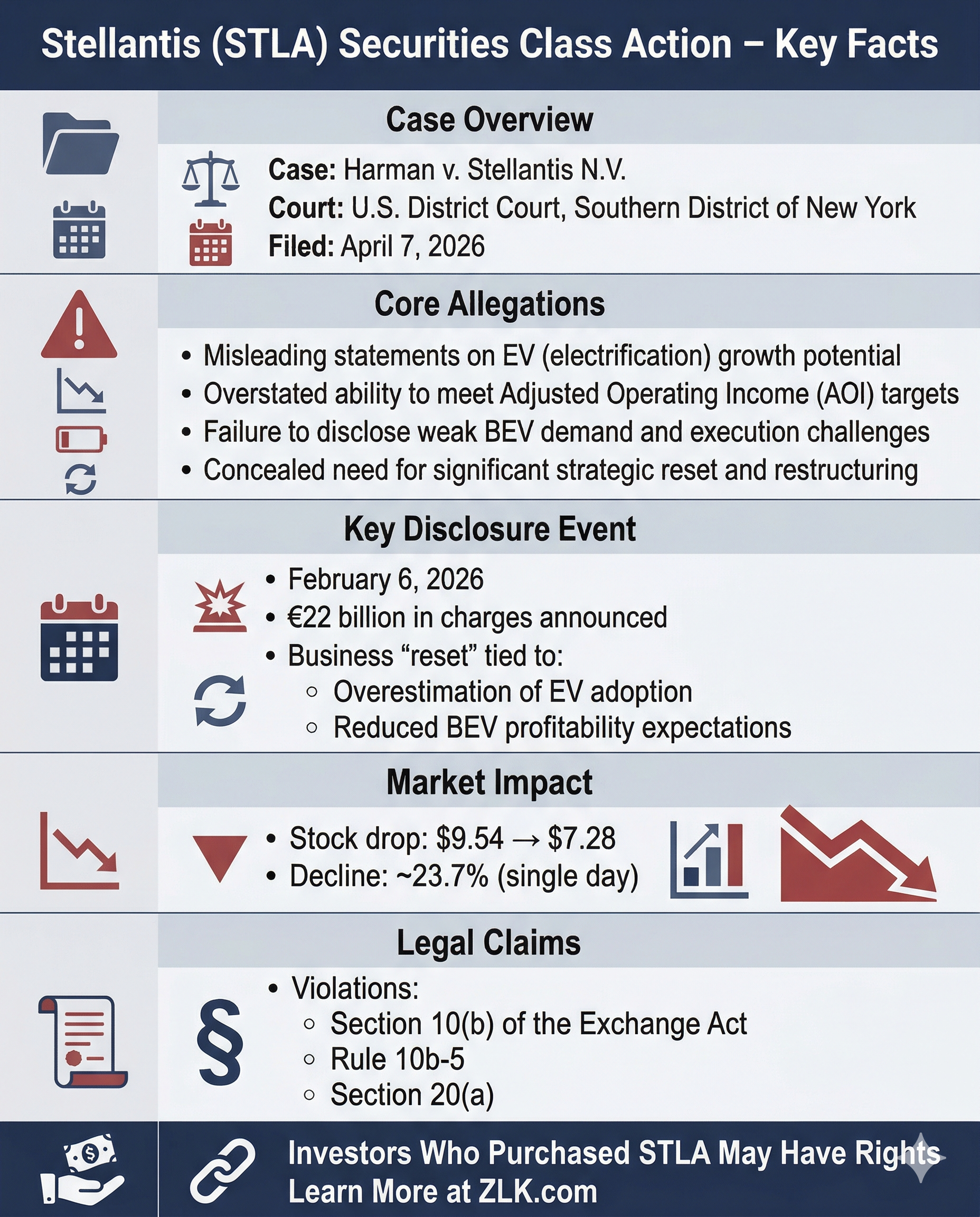

Stellantis N.V. Class Action Lawsuit – STLA

|

Stellantis Class Action Summary |

|

|

Company |

Stellantis N.V. (NYSE: STLA) |

|

Lead Plaintiff Deadline |

June 8, 2026 |

|

Class Period |

February 26, 2025 – February 5, 2026 |

|

Stock Drop |

February 6, 2026 – STLA fell $2.26 (23.69%) to $7.28 |

|

Lawsuit Type |

Securities Class Action |

Introduction

A securities class action lawsuit has been filed against Stellantis N.V. (NYSE: STLA) and several of its senior executives by plaintiff Christopher Harman, represented by Levi & Korsinsky, LLP. The lawsuit covers investors who purchased Stellantis common stock between February 26, 2025, and February 5, 2026, alleging that defendants made materially false and misleading statements about the company's earnings growth potential, its opportunity in the electrification market, and the scale of restructuring charges required to realign its business with actual customer demand. On February 6, 2026, Stellantis announced approximately €22.2 billion in charges alongside a comprehensive "reset" of its business, revealing that its prior confidence in battery-electric vehicle adoption had been fundamentally misplaced. In response, Stellantis stock fell from $9.54 to $7.28 per share in a single trading day, a decline of approximately 23.69%.

Company Profile

Stellantis N.V. is a global automobile designer, engineer, manufacturer, and distributor operating under numerous brands including Jeep, Ram Trucks, Chrysler, Dodge, Fiat, Peugeot, Citroën, Alfa Romeo, Maserati, and Opel. The company also provides financing, leasing, rental services, and after-market parts businesses across multiple geographic regions.

Class Period

February 26, 2025 – February 5, 2026, inclusive.

Investors who purchased or acquired Stellantis N.V. (STLA) securities during the Class Period may be entitled to seek recovery under the federal securities laws.

Allegations

The complaint alleges that beginning on February 26, 2025, when Stellantis reported its fourth quarter and full year 2024 results, defendants painted a consistently optimistic picture of the company's electrification strategy and earnings trajectory. Executive Chairman John Elkann told investors that "electrification is growing" and that Stellantis was "very well equipped for the world to come," while then-CFO Douglas Ostermann outlined expectations for adjusted operating income margins ramping to mid-to-high single digits in North America's second half and significant improvement in Europe. According to the complaint, these statements failed to disclose that Stellantis was not truly positioned to grow its adjusted operating income as forecasted and that its confidence in the pace of electric vehicle adoption was fundamentally disconnected from actual customer demand.

As 2025 progressed, defendants allegedly continued reinforcing this narrative even as warning signs mounted. Stellantis suspended its full-year guidance in April 2025 citing tariff uncertainties, and its first-half results revealed AOI margins of just 0.7% alongside €3.3 billion in restructuring charges. When asked about the potential for additional charges in the second half, Ostermann acknowledged they "could see other strategic shifts that could lead to onetime charges" but characterized the outlook in measured terms. By October 2025, new CFO Joao Laranjo similarly told investors that any project cancellations "could have a cash impact" but that the company "would expect to have limited cash impact in '25." The complaint alleges these disclosures materially understated the severity of what defendants knew or recklessly disregarded about the restructuring required.

The complaint further points to an internal contradiction in defendants' messaging. Even as CEO Antonio Filosa acknowledged in mid-2025 that Stellantis was "correcting some initial all-in BEV powertrain decisions" because prior assumptions about 50% U.S. BEV penetration by 2030 had proven wrong, actual penetration was below 6%, defendants continued to guide investors toward low-single-digit AOI margins for the second half and sequential improvement in all key performance indicators. According to plaintiffs, defendants were aware that the gap between Stellantis' BEV-centric strategy and real customer preferences would necessitate charges of a magnitude far beyond anything signaled to the market, yet they repeatedly minimized these risks while the company's stock traded at artificially inflated prices.

The Truth Emerges

On February 6, 2026, Stellantis disclosed the full scope of its strategic miscalculation. The company announced approximately €22.2 billion in charges, including €6.5 billion in cash payments expected over the following four years, as part of what it called a "decisive reset" of its business. Of these charges, €14.7 billion related directly to realigning product plans with customer preferences, encompassing €2.9 billion in write-offs of cancelled products and €6.0 billion in impairments of BEV platforms due to "substantially reduced volume and profitability expectations." Another €2.1 billion addressed the need to resize the company's electric vehicle supply chain, while €5.4 billion covered warranty provision adjustments driven by quality deterioration and other operational charges. CEO Filosa stated the charges "largely reflect the cost of over-estimating the pace of the energy transition that distanced us from many car buyers' real-world needs, means and desires."

The disclosure also revealed that Stellantis had missed even its already-reduced second-half guidance, with AOI finishing below the guided low-single-digit range. Stellantis announced it would not pay a dividend in 2026 and authorized the issuance of up to €5 billion in hybrid bonds. Analysts reacted with shock at the scale of the writedown. Deutsche Bank noted that "the size of the charges taken and the cash relevant portion of it which is far above market expectations," while Morningstar described the magnitude as "a surprise, particularly the €6 billion platform impairments, given the supposed flexibility of Stellantis' multi-energy architecture to support different powertrains." The gap between what defendants had prepared the market for, the possibility of incremental charges with "limited" cash impact, and the €22.2 billion reality underscored the degree to which investors had been kept in the dark about the full extent of Stellantis' strategic and operational problems.

Market Reaction

Stellantis stock suffered an immediate and severe decline following the February 6, 2026 disclosure. Shares fell from a closing price of $9.54 on February 5, 2026, to $7.28 on February 6, 2026, a single-day drop of approximately $2.26 per share, or 23.69%. The magnitude of the sell-off reflected the market's recognition that the €22.2 billion in charges, the earnings miss against previously guided benchmarks, and the suspension of the dividend collectively represented a far more dire situation than defendants had communicated throughout the Class Period. Multiple analysts cut their price targets in the wake of the announcement, with Deutsche Bank resetting its target and Morningstar reducing its estimate by approximately 12.86%.

Next Steps

● The Court will issue its order for lead plaintiff and counsel in the weeks after submissions are due.

● The Court will then consider motion for class certification.

● The Court will later consider a motion to dismiss.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

Check Eligibility

✓ No cost or obligation

✓ See if you qualify