Table of Contents

- Where Blue Sky Laws Came From

- What Blue Sky Laws Do

- State Regulators: The First Line of Defense

- The Legal Weight of Blue Sky Enforcement

- When State Regulators Collide with the Courts

- Two Case Examples: When Blue Sky Laws Mattered

- Why These Laws Still Matter Today

- A Note on Coordination

- When Blue Sky and Federal Claims Overlap—A Modern Collision

- What Investors Should Watch For

- A Personal Perspective

- Final Reflection—The Skies Above Still Matter

When people think of securities law, they picture the SEC. The three letters carry weight, and Wall Street headlines always trace back to Washington. But the story doesn’t start—or end—at the federal level.

Every state has its own securities regulator. And every state enforces its own version of what are called Blue Sky laws. These laws predate the SEC itself. They were written to stop promoters from selling investments backed by nothing more than “the blue sky above.” A century later, they’re still alive, still powerful, and still shaping investor protection in ways that don’t always make the news.

For investors and companies alike, understanding the role of state regulators isn’t optional. It’s part of the framework of accountability that makes modern securities law what it is.

Where Blue Sky Laws Came From

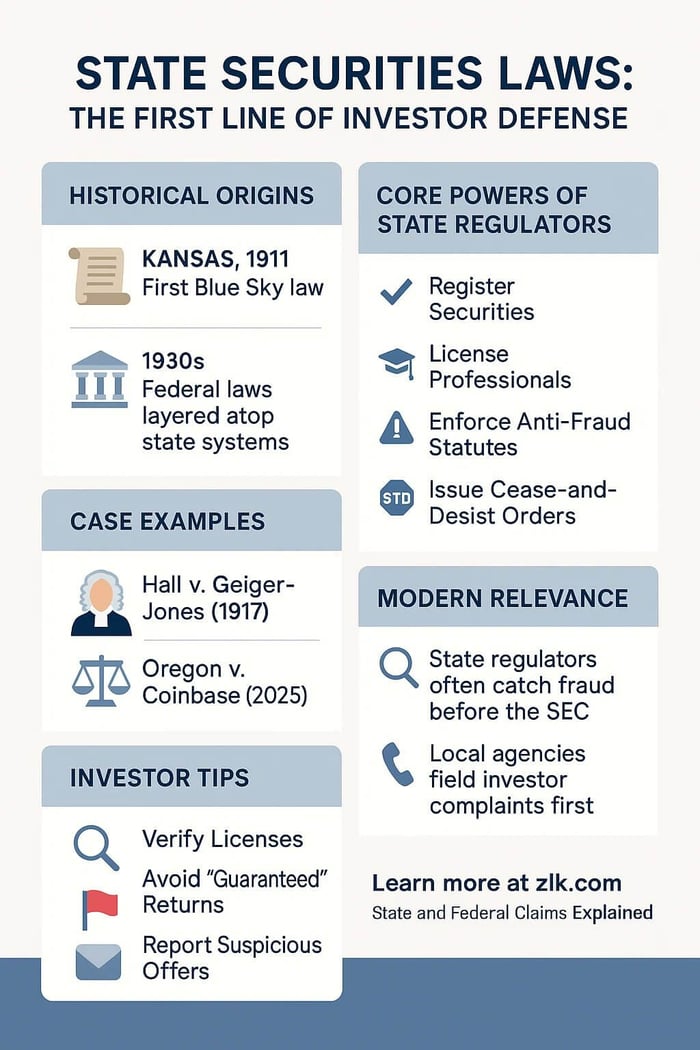

In 1911, Kansas passed the first state securities law aimed at stopping shady stock schemes. The term “Blue Sky” came from a court’s description of fraudulent investments as having no more substance than the blue sky itself.

Within a decade, nearly every state had adopted its own law. The federal securities acts of the 1930s came later, layering national rules on top of the state patchwork. But the state laws never disappeared. These acts include the Securities Act of 1933 and the Securities Exchange Act of 1934, which established the SEC but preserved state authority. They continued to govern offerings, licensing, and enforcement within their borders.

Even today, state securities statutes operate alongside the federal system. Companies that want to raise money often have to comply with both. Regulators at the state level still investigate fraud, license brokers, and bring enforcement actions—sometimes before the SEC even notices a problem.

What Blue Sky Laws Do

Every state’s a bit different, but they usually contain these features:

- Securities Registration: A company must register with the state before it can start selling stocks or bonds there.

- Professionals Licensing: Brokers, investment advisers, and agents have got to get licensed with the state regulator.

- Anti-Fraud Enforcement: Like federal law, state statutes outlaw fraud and misrepresentation in securities sales.

- Administrative Power: States can do things like issue cease-and-desist orders, impose fines, revoke licenses, and refer cases for criminal prosecution.

The overlap with federal law can be confusing. But it’s intentional. Federal law is a floor, not the ceiling. States can—and do—go further. While federal law (e.g., via the SEC) provides a baseline, states can impose stricter requirements.

State Regulators: The First Line of Defense

State securities regulators often are the “first responders” in securities fraud. They’re closer to investors on the ground. They field complaints directly. They know the local brokers and advisers.

In fact, many of the SEC’s biggest cases have started with tips from state agencies. When investors complain about a local adviser or a small-cap promoter, often it’s the state capital that steps in, not Washington.

So while the SEC can focus on big national trends and major market players, state regulators handle the day-to-day, smaller-scale stuff that’s often important, but doesn’t have the dazzle of headlines.

The Legal Weight of Blue Sky Enforcement

Under federal law, Rule 10b-5 is the big hammer against securities fraud. At the state level, Blue Sky laws often mirror that language—making it unlawful to make false statements or omit material facts in connection with the sale of securities.

The difference is in procedure. State regulators can act more quickly. They don’t need to wait for a federal investigation to run its course. They can freeze accounts, stop offerings, and pull licenses almost immediately if they see misconduct.

That speed matters. When someone is selling unregistered promissory notes to church members, or pitching oil-and-gas partnerships at a hotel seminar, time is critical. State agencies often shut these schemes down before they mushroom.

When State Regulators Collide with the Courts

Blue Sky laws are both administrative tool and litigation hammer. Of course, those in the state’s crosshairs clap back and say federal law preempts state authority. Courts haven’t been too sympathetic to that argument. In fact, courts consistently reaffirm states’ role, especially in policing fraud and licensing.

While not a Blue Sky case per se, the Supreme Court in Merrill Lynch, Pierce, Fenner & Smith v. Ware, 414 U.S. 117 (1973) reaffirmed that federal law does not automatically preempt state securities laws. That rule underscores the principle of “cooperative federalism,” meaning states and the feds play an intersecting role in protecting investors.

And more recently, courts have continued to hold that states can impose their own remedies, including rescission, restitution, or administrative sanctions, alongside federal remedies. That dual track is frustrating for companies but intentional for investors.

Two Case Examples: When Blue Sky Laws Mattered

1. Hall v. Geiger-Jones Co., 242 U.S. 539 (1917)

One of the earliest Supreme Court cases to address Blue Sky laws, Hall v. Geiger-Jones upheld the constitutionality of Ohio’s securities statute against claims it violated the Commerce Clause. The Court affirmed that states had a legitimate role in protecting investors against fraud—even in interstate commerce.

Takeaway: Blue Sky laws weren’t a historical curiosity—they were validated as constitutional pillars of investor protection more than a century ago.

2. State of Oregon v. Coinbase, Inc., Case No. 25CV24235 (Multnomah County Cir. Ct., filed Apr. 18, 2025

The Oregon Attorney General sued the crypto exchange in April 2025 for offering 31 cryptocurrencies as unregistered securities. Coinbase allegedly helped facilitate those sales to state residents without registration or proper disclosure, in violation of Oregon’s Blue Sky law. The complaint, filed in Multnomah County Circuit Court, didn’t ride on federal precedent—it stood on its own. The timing, though, was telling: the action came shortly after the SEC dropped its federal case against Coinbase, reinforcing that state regulators don’t stand down when federal enforcement pulls back. The case remains pending, but it underscores that states may pursue enforcement independently of federal action.

Why These Laws Still Matter Today

Critics sometimes argue that Blue Sky laws are redundant—that the SEC already covers the field. But that ignores the practical reality: federal regulators can’t be everywhere. States fill the gaps.

They protect smaller investors. They monitor local brokers. They take on fraud that isn’t large enough to hit the SEC’s radar but can still devastate families. And they often catch misconduct early enough to limit the damage.

For companies, Blue Sky compliance may feel like paperwork. But for investors, it’s part of the thin line between protection and exploitation.

A Note on Coordination

The North American Securities Administrators Association (NASAA) helps coordinate state regulators’ efforts. When you hear about multi-state settlements against abusive mortgage lenders or predatory investment schemes, NASAA is often in the background.

This cooperation highlights the reality: state agencies don’t work in isolation. They share information with each other, and with the SEC, creating a layered system of oversight that’s stronger than any single agency could provide.

When Blue Sky and Federal Claims Overlap—A Modern Collision

States don’t just shadow the feds—they sometimes run alongside them, in parallel. That can happen when a single securities scheme crosses both state and federal lines. One recent example involves Binance, the crypto exchange.

In a class action filed against Binance (called Williams v. Binance, No. 22-972, 2d Cir., 2024), plaintiffs accused Binance of offering unregistered securities—violating both Section 12(a)(1) of the federal Securities Act of 1933 and multiple state Blue Sky laws. Initially, the district court dismissed the claim. But on appeal, the Second Circuit reversed parts of that dismissal and sent the case back for further proceedings. The Second Circuit specifically invited litigation under both federal law and the state laws, where jurisdiction was properly established. The court’s opinion leaves the door open for state-law claims to proceed in tandem with federal claims where jurisdiction permits.

What makes this meaningful isn’t just the tech angle. It illustrates how state regulators and state court systems remain powerful actors in securities enforcement—even when federal claims loom large. Plaintiffs can allege a single wrongdoing and pursue justice on both fronts. And state claims aren’t always booted out or preempted. The federal court’s nod in Williams v. Binance is a modern reminder: Blue Sky laws still matter.

What Investors Should Watch For

You don’t have to memorize state statutes. But there are a few things every investor should know:

- Check Licenses: Most states have online databases to verify if your broker or adviser is registered.

- Beware of “Guaranteed” Returns: State regulators see these claims all the time. They’re red flags.

- Report Suspicious Offers: Many state offices accept investor complaints online. A single complaint can trigger an investigation.

- Understand the Dual Role: Federal filings matter. But state agencies often act on the ground faster.

A Personal Perspective

One of my first jobs in law was inside a state securities regulator’s office. From the inside, the view is different. There’s a never-ending series of calls from investors who lost thousands and don’t know where to turn. Each case was heart-breaking – but the office tried its best for these angry people.

From the inside, you see examiners poring over broker-dealer records in real time, not years later. Others appeared in court to claw back money fraudsters swindled. I poured over thousands of lines of trades in an effort to recover millions for the state’s residents.

From that view, you realize how much of the system’s protection depends not on Wall Street headlines but on small, careful investigations happening in plain office buildings across the country. The states are, to a large extent, investors’ first line of defense.

Final Reflection—The Skies Above Still Matter

Blue Sky laws began as a response to small-town fraudsters a century ago. They survive today because those frauds never went away. They just adapted.

State regulators remain the first line of defense. They don’t always make headlines. But they’re the ones who answer the calls from retirees, shut down the hotel seminars, and make sure the promise of investor protection isn’t just a federal talking point.

Understandably, when people think of securities law they think New York, San Francisco, or Washington. Really, they should be thinking of their state capital. Often, the daily grunt work of investor protection happens under the blue skies of a state office, with state regulators are their defenders.

Disclaimer: Under the rules of certain jurisdictions, this website and its content may constitute attorney advertising. Prior results do not guarantee a similar outcome. This article is for general informational purposes only and does not constitute legal advice. Readers should not act or refrain from acting based on the information contained in this blog without consulting a qualified legal professional.

![Capricor Therapeutics, Inc. (CAPR) Securities Class Action Lawsuit Update [August 25, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/capricor-therapeutics-securities-lawsuit-blog-banner.webp)

![Neogen Corporation (NEOG) Securities Class Action Lawsuit Update [August 26, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/neogen-securities-lawsuit-blog-banner.webp)