Table of Contents

- A Word That Sounds Dry but Decides Cases

- Why Loss Causation Matters

- The Damages Connection

- Case One: Dura Pharmaceuticals v. Broudo

- Case Two: In re Omnicom Group, Inc. Securities Litigation

- Case Three: Mineworkers’ Pension Scheme v. First Solar, Inc.

- Why It’s So Hard in Practice

- Why It Matters to Investors

- Final Reflection

A Word That Sounds Dry but Decides Cases

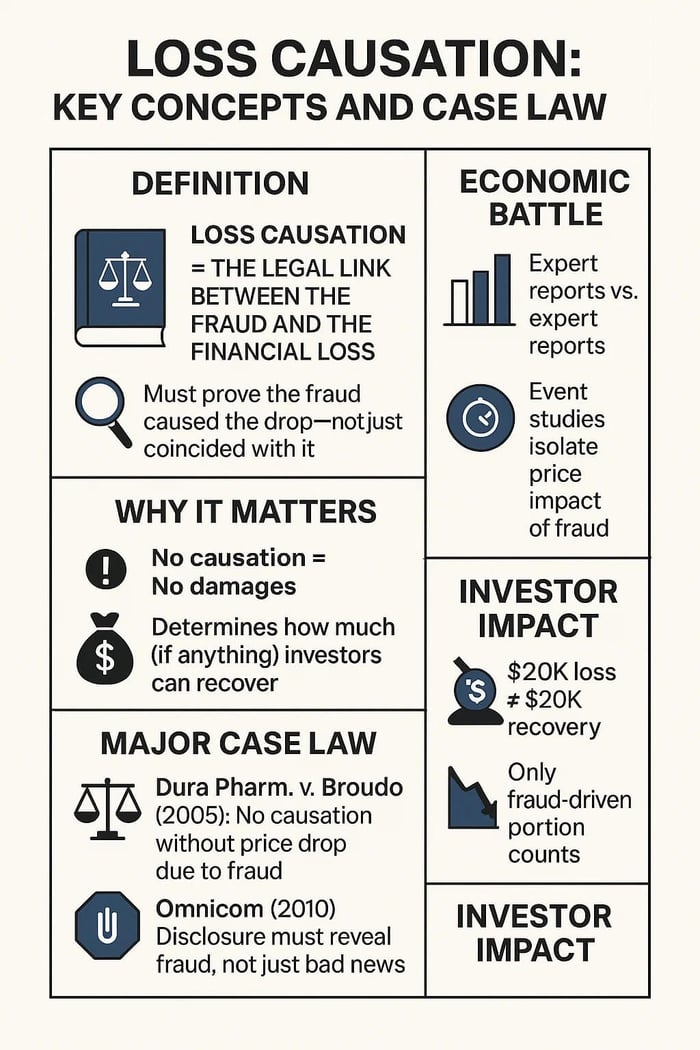

If scienter is about mindset, then loss causation is about connection.

In securities fraud, it’s not enough to prove that a company lied. It’s not enough to prove investors lost money. You’ve got to show the two things are linked—that the fraud actually caused the loss. Lawyers call this “loss causation.”

It sounds clinical, almost like an insurance term. But it’s often the line that separates a giant recovery from a case that fizzles. Because juries and judges want to know: was it really the fraud that tanked the stock, or was it just bad business, or a downturn in the economy, or something else entirely?

Why Loss Causation Matters

Section 10(b) and Rule 10b-5 don’t create a blanket insurance policy against losses. Stocks go up, stocks go down. Markets swing. Companies miss forecasts. Investors can’t sue every time the value drops.

That’s why loss causation exists. It’s the filter. Plaintiffs have to show that the misstatement or omission was a substantial cause of the economic harm. If something else broke the company’s stock price, the damages shrink—or vanish.

Think of it this way: if you trip on a broken sidewalk and break your wrist, you can sue the city for not fixing the sidewalk. But if you broke your wrist because you decided to skateboard down the street blindfolded, the city isn’t paying you. Causation matters.

The Damages Connection

Loss causation isn’t just about liability—it sets the boundaries of damages.

Courts want damages to be tied to the actual fraud, not every dollar investors have ever lost. That means plaintiffs have to untangle stock drops caused by the revelation of fraud from stock drops caused by other things—bad earnings, macroeconomic conditions, or just plain volatility. Under the Private Securities Litigation Reform Act (PSLRA), plaintiffs must plead loss causation with particularity, often relying on expert analyses like event studies to isolate fraud-related impacts.

It’s messy. Economists build event studies, parsing what portion of the price decline is “attributable” to the fraud. Defense lawyers argue the decline was caused by everything else under the sun. Plaintiffs argue the fraud was the trigger. The numbers move depending on how the story is told.

Case One: Dura Pharmaceuticals v. Broudo

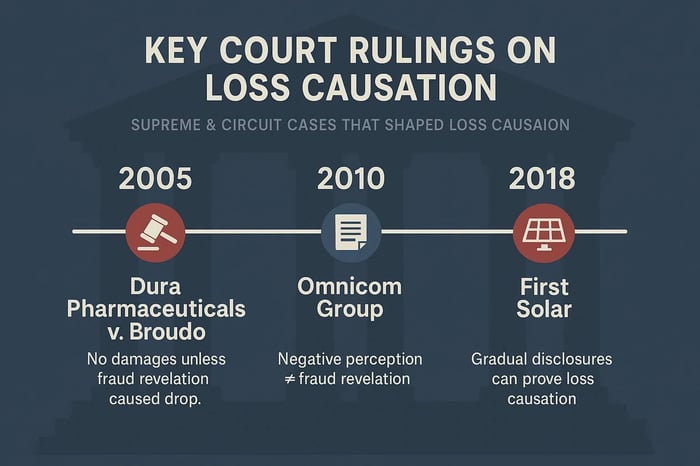

The Supreme Court nailed this point down in Dura Pharm., Inc. v. Broudo, 544 U.S. 336 (2005). Investors claimed Dura misled them about expected FDA approval and sales projections for its Albuterol Spiros asthma inhaler device. The Ninth Circuit had let the case move forward on the idea that paying an inflated price for stock was itself enough harm.

The Supreme Court disagreed. Paying too much at the time of purchase isn’t loss causation. You only have damages if the truth comes out and the stock falls because of it. Without that link, there’s no fraud-based recovery. This overturned the Ninth Circuit's 'price inflation' theory, requiring proof of proximate causation between the revelation and the loss.

What the Court was saying: You can’t just point to a lie and a later loss. You need to show the lie was unmasked and that unmasking caused the loss. Otherwise, you’re suing over coincidence.

Case Two: In re Omnicom Group, Inc. Securities Litigation

Omnicom, a giant advertising firm, faced fraud claims in the early 2000s. Plaintiffs argued the company misled investors about the accounting treatment of a complex transaction involving the transfer of declining internet investments to a new entity (Seneca). When a director resigned amid scrutiny of the deal and news articles questioned its implications, the stock fell—and investors cried fraud.

The Second Circuit in In re Omnicom Group, Inc. Sec. Litig., 597 F.3d 501 (2d Cir. 2010) said not so fast. The disclosure that caused the drop wasn’t a revelation of fraud; it was just a disclosure that investors interpreted negatively. That difference killed loss causation.

Why it mattered: courts want precision. It’s not enough that bad news hit the stock. The bad news has to reveal the fraud itself. Otherwise, damages don’t attach. Negative investor interpretation is not the same as fraud revelation.

Case Three: Mineworkers’ Pension Scheme v. First Solar, Inc.

First Solar is the counterpoint. The company was accused of concealing manufacturing defects that caused accelerated heat degradation in its solar modules, along with the associated financial impacts. When the truth came out gradually—in a series of disclosures—its stock plummeted.

Defendants argued: none of those announcements said “fraud.” They were just technical updates.

The Ninth Circuit disagreed. In Mineworkers’ Pension Scheme v. First Solar Inc., 881 F.3d 750 (9th Cir. 2018), the court held that loss causation doesn’t require a confession. It requires showing the truth leaked out in a way that corrected prior misstatements and caused the price drop.

What that means: Plaintiffs don’t need a dramatic “we lied” press release. A series of smaller disclosures that gradually reveal the concealed risk can still prove loss causation.

Why It’s So Hard in Practice

Loss causation fights usually boil down to dueling experts. Economists on one side say the drop was fraud related. Economists on the other side say it was market forces, or unrelated news. Both sets of charts look convincing. Judges and juries must decide whose story of the numbers makes more sense.

The challenge is that markets are noisy. Stock prices move for dozens of reasons at once—earnings forecasts, competitor news, interest rates, even a tweet. Pinning down the portion tied to fraud is never neat.

And because damages are measured by the drop attributable to fraud, even small shifts in how causation is drawn can mean billions of dollars in or out of a recovery.

Why It Matters to Investors

For investors, loss causation can feel like a technicality. But it’s not. It decides whether losses are recoverable, and how big those losses are.

Imagine you lost $20,000 when a stock tanked. If half that drop was due to broader market conditions, and half due to fraud, your recoverable damages might be $10,000. If none of it can be tied to the fraud, your recovery is zero.

Loss causation isn’t just an element of the case. It’s the line on the spreadsheet that tells you what the case is worth.

Final Reflection

Scienter asks: did they mean to mislead? Loss causation asks: did that lie actually cost investors money? Both are hard. Both are filters. Together, they define securities fraud.

And here’s the human truth: investors don’t sue because stocks go down. They sue because they feel misled—because the story they were sold wasn’t the story that was real. Loss causation is the law’s way of testing whether that feeling of betrayal translates into a legal claim for damages.

In the end, fraud cases aren’t just about lies. They’re about lies that cost money. And proving that connection—tying the misstatement to the loss—is the step that turns frustration into compensation.

Disclaimer: This article is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for advice on specific securities fraud matters.

![Neogen Corporation (NEOG) Securities Class Action Lawsuit Update [August 26, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/neogen-securities-lawsuit-blog-banner.webp)

![Capricor Therapeutics, Inc. (CAPR) Securities Class Action Lawsuit Update [August 25, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/capricor-therapeutics-securities-lawsuit-blog-banner.webp)