![Fiserv, Inc. (FI) Securities Class Action Lawsuit Update [September 25, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/fiserve-inc-securities-class-action-blog-banner.webp)

Unpacking Allegations of Inflated Growth Through Forced Merchant Migrations and the Fallout for FI Investors

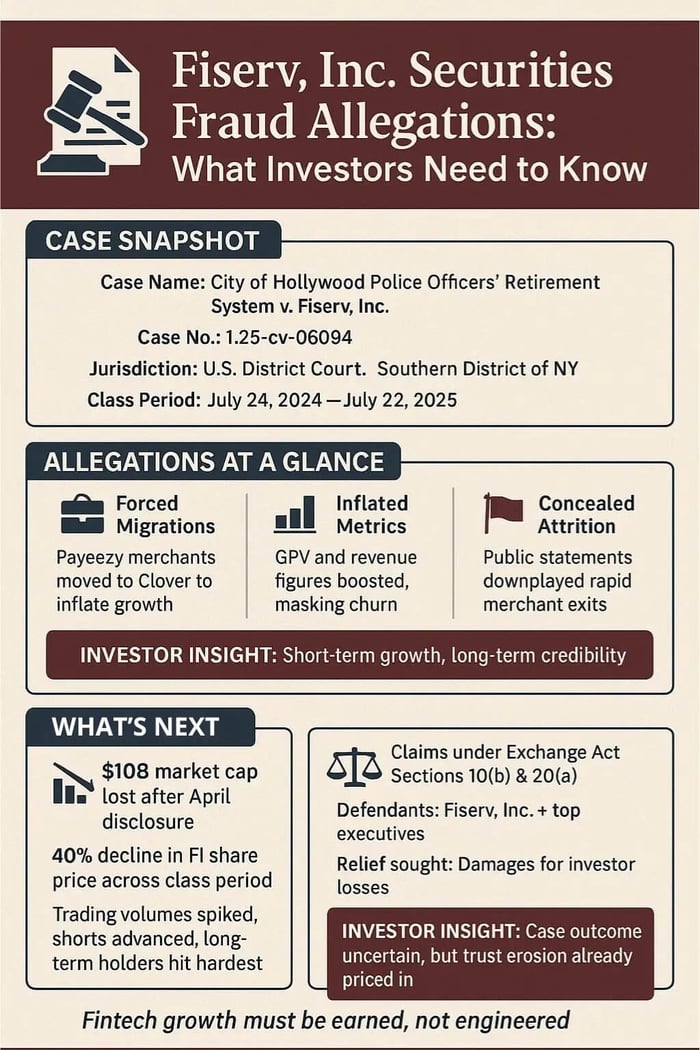

Case Name: City of Hollywood Police Officers’ Retirement System v. Fiserv, Inc., et al.

Case No.: 1:25-cv-06094

Jurisdiction: U.S. District Court, Southern District of New York

Filed on: July 24, 2025

Class Period: July 24, 2024 – July 22, 2025

Introduction

Fiserv, Inc. is facing a securities fraud lawsuit where it’s alleged the company promised a payments revolution anchored by its Clover platform but delivered investors a mirage. Investors who bought into the narrative of organic expansion now face a reckoning in the form of a federal securities class action lawsuit, alleging the company concealed how forced shifts from legacy systems propped up numbers that couldn't hold. The suit, filed in the Southern District of New York, spotlights a familiar tension in fintech: the gap between headline metrics and underlying fragility.

At the heart of the complaint: claims that Fiserv artificially boosted Clover's growth figures by compelling legacy Payeezy users to migrate, all while touting new merchant wins as the driver. When attrition hit—merchants fleeing to cheaper rivals like Square and Toast—the facade cracked, triggering stock plunges that wiped out billions in market cap. This case underscores the risks in fintech's race for scale, where platform transitions can inflate short-term wins at the expense of long-term trust. Investors left holding FI shares confront not only immediate losses but questions about governance in an industry where data opacity reigns.

Backdrop and Business Context

Fiserv traces its roots to Milwaukee, Wisconsin, evolving from a regional check-processing outfit into a global fintech powerhouse through aggressive acquisitions. The pivotal move came in 2019 with the $22 billion all-stock purchase of First Data Corporation, which brought Clover into the fold—a cloud-based point-of-sale system pitched as the future of merchant payments. Clover wasn't just hardware; it was an ecosystem, bundling transaction processing with value-added services like payroll and financing, aimed at small businesses craving integrated solutions.

The company operates in two core segments: Merchant Solutions, where Clover drives revenue through fees on gross payment volume (GPV), hardware sales, and subscriptions; and Financial Solutions, serving banks with account processing and digital tools. According to the complaint, by the class period's start, Clover had become Fiserv's growth engine, with executives like Bisignano emphasizing its role in capturing market share amid a shift to digital payments. Yet this setup bred vulnerabilities. Legacy platforms like Payeezy, inherited from First Data, catered to cost-conscious merchants with basic e-commerce needs. Phasing it out seemed logical—until the migrations turned coercive, exposing mismatches between Clover's premium pricing and the needs of smaller users. Fiserv's executive offices in New York City placed it squarely in Wall Street's gaze, where GPV acceleration signaled health, but deceleration whispered trouble.

Promises Made vs. Reality

Fiserv's narrative was crisp and compelling. At a November 2023 investor conference, Bisignano outlined Clover's path to $3.5 billion in 2025 revenue and $4.5 billion in 2026, driven by "expansion of its direct sales force and increasing VAS revenue through product innovation." He stressed that 90% of growth stemmed from new merchants, with only 10% from "back book" conversions—existing clients voluntarily switching. "We have the benefit of looking at attrition rates from everything," Bisignano assured on the Q2 2024 Call, implying tight oversight.

Reality diverged sharply. The complaint reveals Fiserv forcibly migrated up to 200,000 Payeezy locations to Clover from late 2023 into 2024, inflating 2024's $2.7 billion Clover revenue and $310 billion GPV. These weren't eager adopters; they were price-sensitive users ill-suited to Clover's bells and whistles. Internal churn metrics, which executives claimed to monitor closely, showed rapid departures—merchants ditching for Square or Toast due to higher costs and poor service.

Timeline of Alleged Misconduct and Disclosures

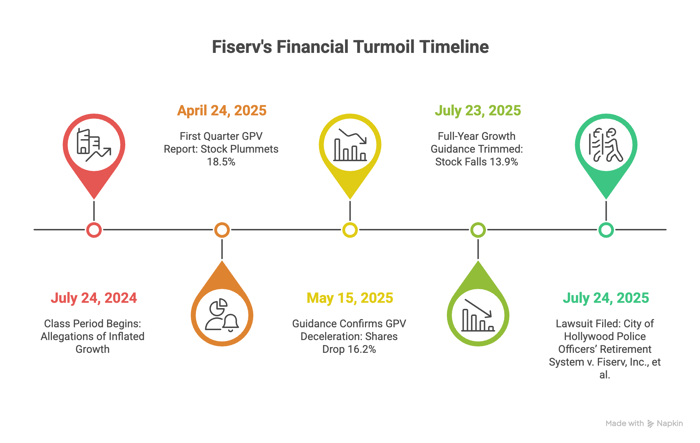

Class Period: July 24, 2024 – July 22, 2025

- April 24, 2025: Fiserv reported first-quarter GPV at just 8%, blaming Payeezy converts' lower volumes. Revenue held at 27%, attributed to hardware and VAS uptake. Media buzzed—analysts flagged the "widest spread" between metrics. FI stock tumbled 18.5%, closing sharply lower.

- May 15, 2025: Guidance confirmed ongoing GPV deceleration, with executives admitting "very significant churn" from back book migrants. Analysts cited the significant churn from former Payeezy to Clover. Shares dropped another 16.2% on this news.

- July 23, 2025: Fiserv trimmed full-year organic growth guidance, merchant segment revenue slowing to 9% from 11%. FI plunged 13.9% to $143.00, capping a cascade that erased investor confidence.

Investor Harm and Market Reaction

The disclosures carved deep into investor confidence. From class period peaks, FI erased more than 40% of its value, amounting to billions in collective setbacks for shareholders, including pension systems. That initial revelation on April 24 vaporized roughly $10 billion in market capitalization, a direct recoil from the GPV slowdown.

Sentiment shifted abruptly—trading volumes surged as positions unwound, shorts advanced. By mid-year, the stock lingered at levels not seen since before the First Data merger. The May 15 update deepened the unease, with shares sliding another 16%, closing near $159, as deceleration signals persisted. Broader views turned cautious; growth assumptions faced scrutiny, sustainability in question amid competitive pressures. July's guidance trim sealed the pessimism, another 14% drop to around $143, reflecting widespread disappointment in the merchant segment's pace.

By July's end, FI traded at discounts unseen since pre-merger days, reflecting not just numbers but eroded faith in management's candor. Overall, the market's mood soured, echoing doubts over Clover's durability in a crowded field.

Litigation and Procedural Posture

The suit invokes Sections 10(b) and 20(a) of the Exchange Act, plus Rule 10b-5, alleging false statements on Clover's growth drivers. Defendants include Fiserv, Inc. and executives Bisignano (ex-CEO), Lyons (current CEO), Hau (CFO), and Best (CAO), accused of controlling misleading disclosures. Scienter allegations hinge on their access to attrition data—Bisignano's boasts of monitoring "everything" undercut ignorance claims. Filed on July 24, 2025, the case demands jury trial; motions to dismiss loom, testing loss causation amid stock drops synced to disclosures.

Shareholder Sentiment

Across platforms like X and Stocktwits, Fiserv's unraveling sparked a shift from guarded optimism to outright frustration. Before April's drop, early 2025 threads buzzed with Clover hype, such as: "FI's got the payments edge, GPV flying high[.]"

Post-disclosure, the tone darkened. On X: "FISERV’S CLOVER TURNS SOUR! Despite a red-hot market, $FI's downtrend screams MISSED OPPORTUNITY... Problematic deceleration or turnaround play?" Echoes rippled through Reddit's r/investing: "Bought in on the organic growth story—now it's all forced migrations and churn. Feels like bait and switch." Stocktwits threads trended bearish after May: "Attrition from Payeezy users killing momentum; management's credibility shot." By July, sentiment hit nadir—posts like "Time for legal action" from disgruntled holders reflected betrayal, blending calls for accountability with vows to divest.

The lawsuit announcement amplified this, drawing comparisons to other fintech fiascos, though a minority held out for recovery: "Dust settles, FI rebounds—fundamentals still there."

Analyst Commentary

Professional voices amplified the alarm. Pre-class period, optimism reigned. Targets hovered above $200, with praise for Clover's VAS penetration. April's GPV shock flipped the script.

The April 24, 2025, Q1 earnings miss upended that poise, as Clover's GPV growth slowed to 8%. Reactions centered on the yawning gap between revenue and volumes:

- J.P. Morgan: According to the complaint, flagged the "widest spread between revenue and volume in our model’s history, raising concerns about sustainability of premium growth," holding neutral but trimming estimates.

May 15 brought further gloom, with confirmation of persistent GPV deceleration through 2025. Surprise rippled through coverage, underscoring churn from back book migrations:

- Bernstein: highlighted "intensifying competitive dynamics" and churn risks.

- Goldman Sachs: noted "very significant churn" from back book.

By July 23, the lowered full-year guidance—trimming organic revenue to the low end—and merchant segment deceleration to 9% cemented skepticism:

- Wolfe: "We recognize a need for the dust to settle, with stability/credibility in metrics and guidance reestablished before some investors add materially to shares."

- Keefe Bruyette & Woods: "FI missed Merchant segment organic growth expectations (again) and lowered its FY25 organic growth revenue outlook to the lower end of the prior range, implying the steep ramp in Merchant segment growth that was previously anticipated is unachievable."

Consensus shifted bearish, with average targets dropping to $150, reflecting skepticism on Clover's path amid rivals' gains.

SEC Filings & Risk Factors

Fiserv’s disclosures painted Clover as a growth juggernaut, but plaintiffs allege they glossed over migration pitfalls.

- 2023 10-K (year ended Dec 31, 2023): Touted Clover’s potential, warned broadly of competition from rivals like Square and Toast, and risks of merchant attrition or failure to renew contracts.

- Q2 2024 10-Q: Referenced 2023 10-K risks without updates, amid touting Clover’s 17% GPV growth.

- Q3 2024 10-Q: Similar boilerplate, as Clover revenue hit 28% growth.

- 2024 10-K (year ended Dec 31, 2024): Echoed prior warnings, added AI risks but downplayed platform transitions as mere “costs and disruptions.”

- Q1 2025 10-Q: No significant risk changes noted, despite GPV drop to 8%.

- July 23, 2025 8-K: Lowered organic growth guidance, merchant segment to 9%.

Plaintiffs argue omissions concealed Clover’s reliance on forced Payeezy shifts, masking churn and unsustainable metrics.

Conclusion: Implications for Investors

This Fiserv saga lays bare fintech's migration pitfalls: where legacy overhauls promise efficiency but deliver churn if mismatched with user needs. For holders of FI, watch for GPV-revenue divergences as red flags; organic growth claims demand scrutiny against back-book dependencies. Broader sectors, from SPACs to payments startups, face amplified regulatory gaze, where opacity invites suits. Investors emerge wiser, armed to probe beyond headlines, turning forced evolutions into voluntary vigilance. The courtroom may decide restitution, but the market has already rendered its verdict.

![Fiserv, Inc. (FI) Securities Class Action Lawsuit Update [Sept 15, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/fiserve-shareholder-alert-blog-banner.webp)