FDA's IGNYTE Trial Rejection Ignites Lawsuit Over Misleading Disclosures [September 17, 2025]

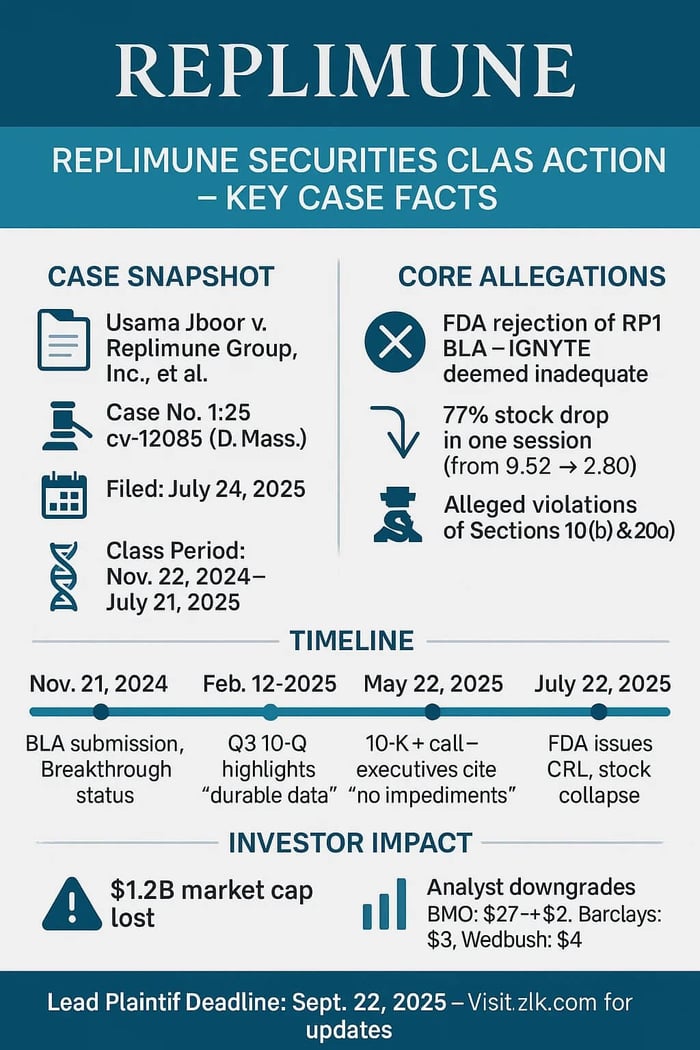

Case Name: Jboor v. Replimune Group, Inc., et al.

Case No: 1:25-cv-12085

Court: U.S. District Court for the District of Massachusetts

Filed: July 24, 2025

Class Period: November 22, 2024 to July 21, 2025

Introduction

A biotech promise unravels. Replimune Group Inc., once heralded for its oncolytic virus platform targeting stubborn melanomas, now stands accused of painting too rosy a picture. On July 22, 2025, the FDA's complete response letter—rejecting the biologics license application for lead candidate RP1—sent REPL shares tumbling 77% in a single session. Investors, caught in the downdraft, filed a securities class action, alleging the company and its executives buried flaws in the pivotal IGNYTE trial.

Backdrop and Business Context

Replimune emerged from the labs in 2015, with a singular fixation: harnessing herpes simplex virus to wage war on cancer. The RPx platform—RP1 at its vanguard—engineers HSV-1 to infiltrate tumors, unleash antigens, and rally the immune system. It's the kind of elegant brutality that drew venture capital like moths to flame, culminating in a 2018 NASDAQ debut under REPL. By fiscal 2025, the company had burned through ambitions, partnering with Bristol Myers Squibb for nivolumab supply in trials, all while eyeing RP1 as the crown jewel for skin cancers like melanoma.

Operationally, Replimune ran lean with a Woburn base and global trial sites. Milestones dotted the path—Breakthrough Therapy Designation in late 2024, BLA submission under accelerated approval. IGNYTE, a multi-cohort clinical trial with Bristol Meyers Squibb, was a collaboration yielding topline data in 2024 that boasted a 33.6% overall response rate by modified RECIST criteria.

Investors bought the vision: RP1 as a versatile warrior, synergistic with checkpoints, poised to claim a slice of the melanoma market. But as the complaint alleges, that vision blurred at the edges, where trial design whispers turned to regulatory shouts.

Promises Made vs. Reality

Words carry weight in biotech, where a single press release can summon billions. In November 21, 2024 press release Replimune beamed: "Today announced that it has submitted a biologics license application (BLA) to the FDA for RP1... under the Accelerated Approval pathway." Patel himself lent voice: "Today is an important milestone... one step closer to having another potential treatment available for patients who have limited options."

Fast-forward to filings. The Q3 2025 10-Q, signed by Patel and Hill under Sarbanes-Oxley, reiterated: "The topline results showed the overall response rate... was 33.6%... Responses from baseline were highly durable." The subtext? IGNYTE's data—85% durable responses, median duration north of 20 months—spoke of triumph. The May 2025 10-K echoed, layering in ESMO and SITC presentations: "Activity across all subgroups...ORR of 27.7% [for prior anti-PD1 and anti-CTLA-4 patients]." Earnings calls amplified the chorus. According to the complaint, Defendant Hill, on May 22 stated: "We're very pleased with the outcome of those interactions, and we believe there are no impediments. We're on track for our July 22 PDUFA." Defendant Patel chimed in: "We've seen around 1/3 of patients achieved durable responses... overall survival... more than about 55% of patients still alive at 3 years."

Reality intruded sharper. The complaint paints these as veils over a core flaw that IGNYTE, per FDA's later verdict, wasn't "an adequate or well-controlled clinical investigation." Where executives touted "priority review" and "no impediments," the trial's single-arm design, subgroup variances, and endpoint tweaks allegedly masked inadequacies. Investors heard inevitability. The gap? A chasm between marketed momentum and buried doubts.

Timeline of Alleged Misconduct and Disclosures

Class Period: November 22, 2024 – July 21, 2025

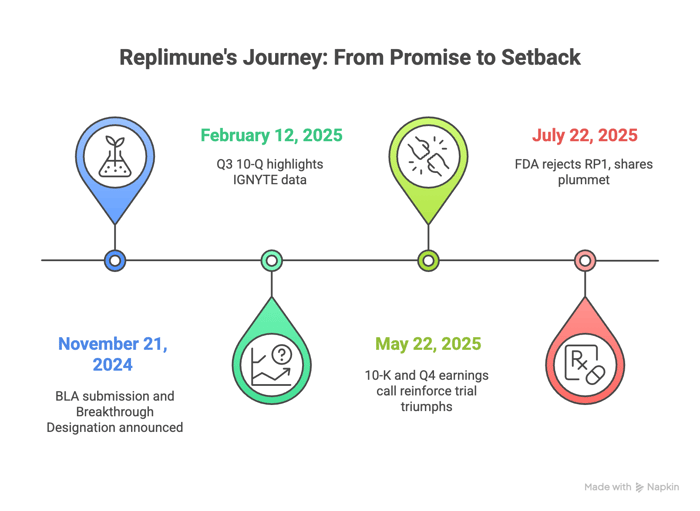

- November 21, 2024:Post-market glow. BLA submission and Breakthrough Designation announced. Media buzz—Stat News hails "a step closer for melanoma warriors."

- February 12, 2025:Q3 10-Q drops, SOX-certified by Patel and Hill. IGNYTE data repackaged as unassailable, with FDA acceptance and priority review.

- May 22, 2025: Dual salvo—10-K and Q4 earnings call. Filings recycle trial triumphs; call transcript brims with confidence: Hill's "no impediments," Patel's survival benchmarks.

- July 22, 2025: The pivot. Pre-market, Replimune discloses FDA's Complete Response Letter, citing IGNYTE's inadequacy. Shares plunge about 77% to $2.80.

Investor Harm and Market Reaction

The math of betrayal: Over the class period, REPL shed nearly 80% from highs, vaporizing $1.2 billion in market cap on disclosure day alone. Stock purchases at inflated valuations, sales in the wreckage. High-volume trading amplified the pain; halts couldn't stem the bleed. Pre-rejection, optimism reigned with buy ratings and targets around $20, buoyed by IGNYTE's apparent durability.

Analyst sentiment soured swiftly. Following the July 22 press release, ratings shifted to hold or neutral, targets halved amid warnings of trial scrutiny and platform doubt. Post-crash, shares clawed a 20% rebound by late July, fueled by dip-buyers and whispers of FDA internal shifts, though volume thinned and bearish undertones lingered.

Investors.com tallied: "77% wipeout tests faith in oncolytics." For fund managers, it's a textbook loss causation—misstatements inflate, truth deflates, damages cascade —now laced with biotech's binary volatility, where a regulator's departure can rewrite the narrative overnight.

Litigation and Procedural Posture

Massachusetts filing tags Replimune, Patel, Hill for 10(b), Rule 10b-5, 20(a) violations. Scienter: Executives, deep in operations and FDA whispers, knew or recklessly ignored IGNYTE's fatal flaws—trial not adequate, well-controlled—yet greenlit glowing filings and calls. No insider sales flagged, but SOX seals and omission chains, as alleged, stoke the fire. Demands class certification, jury trial, damages. Fresh off July 24 docket: Lead plaintiff deadline nears, dismissal volleys next. Biotech's broad holder base signals a slog through discovery's shadows.

Shareholder Sentiment

Before July 2025, retail investors buzzed with optimism around Replimune's prospects. On Reddit's r/pennystocks in mid-July, one user posted: "Why I think REPL will see a decent upside in the short term... RP1 has both Priority Review and Breakthrough Therapy designations." In r/Biotechplays back in May: "As we near our PDUFA date, our commercial organization is now fully hired and ready to execute our first launch." On X in late July: "$REPL All eyes on REPL this week with PDUFA Tuesday, July 22. Viral immunotherapies have come a long way[.]"

After the July 22 FDA rejection, the mood soured sharply. Reddit's r/biotech erupted: "Replimune's shares crater as FDA rejects melanoma drug... Looks like Prasad wants to tighten up approval standards." In r/wallstreetbets, users vented frustration over the CRL: "Replimune's RP1 was IOVA's biggest competitive threat, and the rejection... means that Amtagvi will be able to maintain its monopoly." Stocktwits reflected the shift, sentiment flipping to 'extremely bullish' spikes amid rumors of reversal post-Prasad's exit: "Replimune stock catches retail fire as analyst says FDA shakeup removes 'major obstacle' for skin cancer drug."

Analyst Commentary

Before the July 2025 rejection, analysts largely leaned bullish on Replimune's trajectory. In January 2025, BMO Capital raised its price target to $27 from $18, maintaining an Outperform rating amid FDA acceptance of the RP1 BLA. By February, HC Wainwright lifted to $22 from $21, reiterating Buy on strong IGNYTE data and priority review. Consensus in May hovered at Buy, with average targets near $20 driven by durable responses and PDUFA momentum. Piper Sandler upped to $22 Overweight in June, citing ASCO updates and no AdCom risks.

July 22's CRL refracts the light. The FDA's Complete Response Letter flipped the narrative. Cantor Fitzgerald downgraded from Overweight to Neutral on July 22 amid trial design flaws. BMO Capital shifted to Underperform that day, slashing to $2 from $27. Barclays joined at Equalweight $3, Leerink to Market Perform $3, and Wedbush to Neutral $4, all underscoring IGNYTE inadequacies.

SEC Filings & Risk Factors

Replimune's filings reflected optimistic forward momentum, but plaintiff argues they left out risks.

- November 21, 2024 press release: Announced BLA submission under accelerated approval; Patel quoted, "Today is an important milestone... one step closer." Breakthrough Designation cited IGNYTE's "safety and clinical activity."

- February 12, 2025 10-Q (Q3 FY2025): Highlighted IGNYTE's "ORR... 33.6%... highly durable with 85%... lasting more than 12 months"; BLA accepted, PDUFA July 22, 2025; SOX certifications by Patel and Hill.

- May 22, 2025 10-K (2025 Annual Report): Reiterated "ORR was 33.6%... well-tolerated... on track for [PDUFA].”

- July 22, 2025 press release: “[T]he FDA is unable to approve the application in its present form…the IGNYTE trial is not considered to be an adequate and well-controlled clinical investigation… no safety issues were raised…[t]he Company will request a Type A meeting and expects it will be granted within 30 days.”

Conclusion: Implications for Investors

Replimune's setback unveils biotech vulnerability. Trial hopes, approval bets—dig deeper. Red flags: Data gloss, PDUFA cling, regulatory whispers. In immuno-oncology, FDA rigor rules; one flaw, gains dissolve. Suit trackers linger. Takeaway stings: Amid cure-all shine, seek fissures—or see portfolios crumble like rejected drugs.

![RxSight, Inc. (RXST) Securities Class Action Lawsuit Update [September 16, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/rxsight-securities-lawsuit-blog-banner-1.webp)

![Fiserv, Inc. (FI) Securities Class Action Lawsuit Update [Sept 15, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/fiserve-shareholder-alert-blog-banner.webp)