![RxSight, Inc. (RXST) Securities Class Action Lawsuit Update [September 16, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/rxsight-securities-lawsuit-blog-banner-1.webp)

Decoding the RXST Securities Class Action Allegations and What It Means for Investors

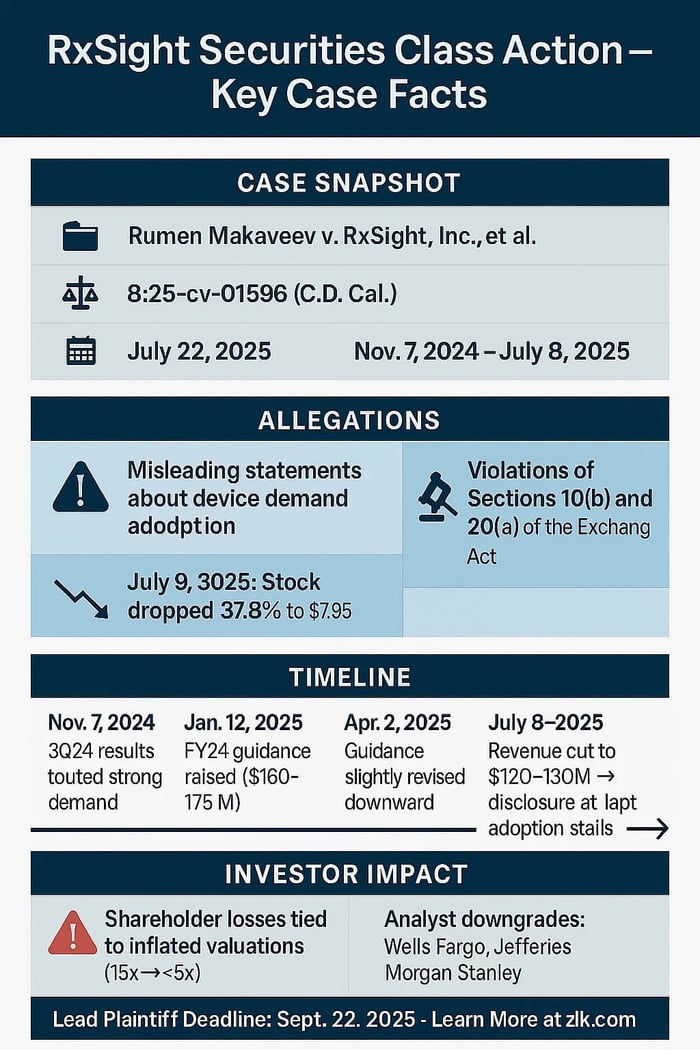

Caption: Makaveev v. RxSight, Inc., et al.

Case No.: 8:25-cv-01596

Jurisdiction: U.S. District Court, Central District of California

Filed on: July 22, 2025

Class Period: November 7, 2024 – July 8, 2025

Introduction

Investors watched RxSight, Inc. plummet in a single day, the kind of drop that echoes through portfolios long after the trading bell. On July 9, 2025, shares of RXST tumbled 37.8%, closing at $7.95 amid revelations that shattered the company's narrative of unstoppable growth. Now, a securities class action lawsuit filed in the U.S. District Court for the Central District of California alleges that RxSight and its executives misled shareholders about device demand and financial prospects.

Backdrop and Business Context

RxSight, Inc. emerged from the shadows of ophthalmic innovation, headquartered in Aliso Viejo, California, trading on NASDAQ under RXST. At its core, the company develops and sells light adjustable intraocular lenses—LALs—used in cataract surgery, allowing post-operative tweaks to vision via ultraviolet light delivered through its proprietary Light Delivery Device, or LDD. This RxSight system promised a revolution: customizable eyesight without the finality of traditional implants.

The company's journey to public markets began with an IPO in July 2021, raising funds to scale manufacturing and penetrate a premium IOL market dominated by giants like Alcon and Johnson & Johnson. By 2024, milestones piled up—FDA approvals, expanded indications for the LAL+, and a growing installed base of LDDs across North America. Revenue surged 57% year-over-year to $139.9 million in 2024, fueled by 305 LDD sales and 98,055 LAL procedures. Executives touted this as evidence of "transformative power," positioning RxSight as a disruptor in a $5 billion global cataract market. Yet beneath the surface, dependencies on surgeon adoption and patient willingness to pay premiums set the stage for the alleged missteps, where operational hurdles in scaling light treatments clashed with aggressive forecasts.

Promises Made vs. Reality

Executives painted a picture of relentless demand, but the lawsuit contends it was a facade. In a November 7, 2024 press release, CEO Ron Kurtz declared, "We are pleased to report another strong quarter driven by ongoing demand and enthusiasm for the RxSight system." The release highlighted 59% revenue growth to $35.3 million, with LAL sales up 80% and LDD units up 18%, expanding the installed base to 888. Kurtz emphasized "sustained growth in LAL sales," positioning the company for "continued success in the years to come."

The third-quarter 10-Q (3Q24 10-Q) echoed this optimism, stating sales increased "primarily due to the incremental sales of 10,897 LALs and 12 LDDs from strong adoption of our RxSight system by practices and doctors." It spotlighted key metrics: "We believe the number of LDDs sold in each quarter and our LDD installed base at the end of each period are important metrics as they represent an installed base into which we can sell our LALs."

Reality, as alleged in the complaint, diverged sharply. On July 8, 2025, RxSight issued a press release announcing preliminary Q2 2025 results reflecting revenue at $33.6 million—a 4% YoY decline—and a slashed full-year guidance from $160-175 million to $120-130 million. This $42.5 million midpoint cut exposed overstated demand, with LDD sales and LAL utilization faltering amid structural issues in post-operative infrastructure. On the Q2 2025 earnings call, Kurtz disclosed that "adoption challenges over the last few quarters" as the "primary reason for the LDD stall."

Timeline of Alleged Misconduct and Disclosures

Class Period: November 7, 2024 – July 8, 2025

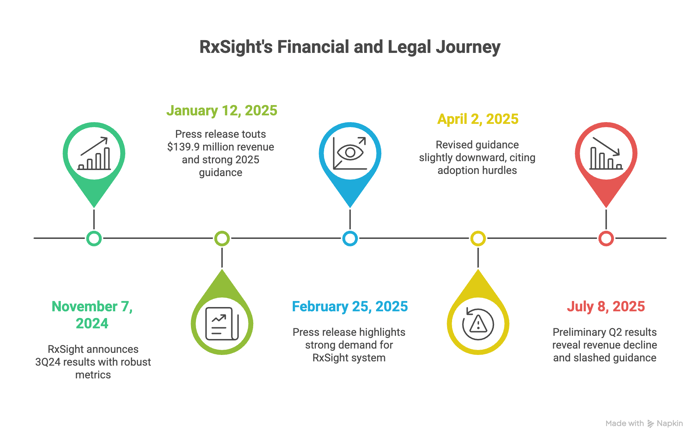

- November 7, 2024: RxSight announces 3Q24 10-Q results and heralded robust metrics, with shares buoyed by raised 2024 guidance.

- January 12, 2025: Press release issued preliminary unaudited Q424 and full-year 2024 results that touted $139.9 million revenue, up 57%, and initial 2025 guidance of $160-175 million, with Kurtz forecasting strong adoption and international expansion.

- February 25, 2025: RxSight issued a press release highlighting financial results and strong demand for RxSight system.

- April 2, 2025: RXST issued a press release with revised guidance slightly downward, citing early adoption hurdles, yet still projected growth.

- July 8, 2025: RxSight's preliminary Q2 results revealed $33.6 million revenue—down 4% YoY and 11% sequentially—with substantial declines in LDD sales, LAL procedures and overall Company revenue.

Investor Harm and Market Reaction

Losses mounted swiftly. The July 9, 2025, drop erased $4.84 per share. Broader harm ties to inflated multiples: RXST traded at 15x forward sales pre-disclosure, now languishing below 5x amid revised forecasts.

Analyst reactions amplified the pain. Wells Fargo downgraded to Equal Weight on July 9, slashing its target from $25 to $9, citing "sales concerns." Jefferies followed on July 10, downgrading from Buy to Hold, reducing their price target to $9. Morgan Stanley cut to Equal Weight later, with consensus targets from $20 to $9. Market chatter on platforms like Stocktwits turned bearish, with some users lamenting "another medtech flameout" as sentiment scores dipped to 20/100 post-drop.

Litigation and Procedural Posture

The lawsuit accuses RxSight and some of its top executives of violating Sections 10(b) and 20(a) of the Exchange Act. Plaintiffs allege executives acted with scienter through knowledge of adoption stalls, evidenced by Kurtz's admission of "challenges over the last few quarters."

The suit seeks a jury trial and damages for the plaintiff. The case was filed in the Central District of California on July 22, 2025. Lead plaintiff motions are due soon.

Shareholder Sentiment

Pre-drop, sentiment leaned positive on growth narratives; post-revelation, it soured, with calls for executive accountability dominating. This pivot underscores how quickly faith erodes when promises fracture.

Voices across platforms reveal a shift from guarded optimism to outright disillusionment. On X (formerly Twitter), posts captured the raw edge of betrayal. One investor lamented, "Every time they get hit with a lawsuit, the stock takes a hit. I'm worried that they are not a legit medical company, but only masquerading as one. Too risky for me."

Another, from an analyst account, noted, "Legal headwinds for its light-adjustable lens business weighed on sentiment," tying the drop to litigation fears. Trends showed a spike in negative mentions post-July 8, with hashtags like #RXSTlawsuit trending briefly, users warning of "shaky sentiment" and "high volatility risk."

Stocktwits echoed this gloom, with sentiment flipping from 60% bullish pre-disclosure to 80% bearish afterward. Threads buzzed with frustration: "Lost big on RXST—guidance cut was the nail in the coffin." Reddit's r/stocks and r/investing subs hosted sparse but pointed discussions, one user posting, "RXST class action incoming? Adoption challenges were obvious if you read between the lines."

Analyst Commentary

Before July 2025, optimism reigned:

- January 2025: Stifel reiterated Buy at $35, praising sustained growth.

- April 2025: Needham held Buy at $43 citing “double-digit growth and the prospect of near-term profitability.”

But the Q2 preliminary sparked downgrades:

- Wells Fargo (July 9, 2025): Downgraded RXST from Overweight to Equal Weight with a $9 target, citing the 25% cut to fiscal year 2025 guidance.

- Jefferies (July 10, 2025): Downgraded its target from $24 to $9, citing “elongated LDD capital selling cycles as a key factor in the downgrade” and “noting that new customers are taking longer to ramp up operations than previously anticipated.”

- Morgan Stanley (July 15, 2025): Downgraded to Equal Weight, highlighting growth concerns.

Professional views swung decisively post-disclosure, reflecting eroded confidence.

SEC Filings & Risk Factors

RxSight's filings offered warnings, yet the lawsuit argues they fell short of revealing known issues. The 3Q24 10-Q, filed November 7, 2024, disclosed risks hypothetically: "The commercial success of our RxSight system will depend upon attaining significant market acceptance... Our success will depend, in part, on the acceptance of our RxSight system as safe, effective and, with respect to doctors, cost-effective." On demand forecasting: "Our results of operations could be materially harmed if we are unable to accurately forecast customer demand for our products and manage our inventory."

The document qualified these as possibilities—"may" or "could"—without commentary concerning ongoing stalls. Management's discussion affirmed "strong adoption," with sales up 59% due to "incremental sales... from strong adoption." The most recent 10-K (FY24 10-K) echoed supply chain vulnerabilities: "We seek to maintain sufficient levels of inventory... but due to the expansion of global lead times... has resulted in the lack of availability of raw materials."

Plaintiff argues omissions include failing to flag "adoption challenges" despite alleged internal awareness.

Conclusion: Implications for Investors

This RxSight saga teaches a familiar lesson in medtech: where innovation dazzles, execution falters can blindside. With the lead plaintiff deadline looming on September 22, 2025, shareholders face a narrowing window to step forward.

For portfolio stewards, this prompts a deeper probe into utilization metrics, those quiet harbingers of demand erosion in growth-dependent sectors like biotech or emerging health tech. Class counsel, meanwhile, gauges momentum from the 37.8% plunge, a stark anchor for damages. The broader echo? In a market rewarding growth narratives, verify the foundation—innovation alone won't illuminate the path if infrastructure falters. Investors, attuned now to such shadows, should proceed with eyes adjusted.

![RxSight, Inc. (RXST) Securities Class Action Lawsuit Update [September 03, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/rxsight-securities-lawsuit-blog-banner.webp)

![Alto Neuroscience, Inc. (ANRO) Securities Class Action Lawsuit Update [September 10, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/anro-shareholder-alert-blog-banner.webp)