![Alto Neuroscience, Inc. (ANRO) Securities Class Action Lawsuit Update [September 10, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/anro-shareholder-alert-blog-banner.webp)

Alto Neuroscience promised a revolution in treating depression. It didn't deliver.

Caption: Feldman v. Alto Neuroscience, Inc., et al.

Case No.: 5:25-cv-06105-NW

Jurisdiction: U.S. District Court, Northern District of California

Filed on: July 21, 2025

Class Period: February 2, 2024 – October 22, 2024

Introduction to Alto Neuroscience Lawsuit

Alto Neuroscience, Inc. (ANRO) is facing a securities lawsuit connected to their initial public offering (IPO). Investors who bought into the hyper during Alto’s IPO didn’t expect their investment to unravel so spectacularly. On July 21, 2025, a complaint was filed against the Company and nine of its top executives and/or directors.

At the heart of the allegations: misleading hype around ALTO-100's efficacy and prospects. Plaintiff claims the company overstated the drug's potential, leading to inflated stock prices that cratered upon the truth's emergence. Per the complaint, the truth was revealed on October 22, 2024, when Alto issued a press release that it’s lead drug candidate did not meet primary endpoints. This disclosure triggered a 69.99% drop, with shares closing at $4.36 the next day.

For shareholders, this lawsuit represents more than legal recourse—it's a reckoning with the risks of betting on unproven biotech innovations.

Backdrop and Business Context

Alto Neuroscience emerged as a clinical-stage biopharmaceutical player focused on precision psychiatry. Headquartered in Mountain View, California, the company leverages a proprietary platform that analyzes brain biomarkers—via neurocognitive tests, EEG, and wearables—to match patients with treatments. This data-driven approach aimed to sidestep the trial-and-error plaguing CNS drug development.

Founded in 2019, Alto positioned itself as a disruptor in mental health therapeutics. Its pipeline centered on ALTO-100, a small molecule touted for promoting neuroplasticity by engaging a receptor not targeted by existing CNS drugs. By the IPO, ALTO-100 was in Phase 2b for MDD, a market ripe for innovation amid rising depression rates.

The IPO on February 2, 2024, marked Alto's public debut. Priced at $16 per share, it raised about $119.6 million after discounts. Executives pitched a future where biomarkers predict responders, accelerating approvals and commercial success. Yet, this narrative rested on early data and vast datasets—250 terabytes from clinical trials and licenses—fueling optimism but also vulnerability to trial failures.

Milestones included positive Phase 2a results in 2023, showing ALTO-100's safety and hints of efficacy in biomarker-defined subgroups. Post-IPO, Alto expanded trials, but the core bet was on ALTO-100's validation. In a sector where 90% of CNS drugs fail, Alto's biomarker strategy was both innovative and high-stakes—setting the stage for the alleged misconduct.

Promises Made vs. Reality

Alto's Offering Documents painted ALTO-100 as a game-changer. In the Registration Statement and Prospectus, the company claimed: "[W]e believe we can help patients avoid the often-lengthy process of trying multiple ineffective treatments... Our approach is designed to improve patient outcomes and increase the likelihood of clinical success."

Directly on ALTO-100: It "has shown evidence of a pro-neurogenesis/neuroplasticity mechanism of action" and "binds a receptor not targeted by other [CNS] therapeutics, which would make it first-in-class if approved." Executives like CEO Amit Etkin reinforced this in roadshows, emphasizing biomarker-driven precision to "substantially improve upon the traditional, all-comer approach."

Reality struck differently. The Phase 2b trial, enrolling 301 patients, failed to meet its primary endpoint—a change in Montgomery-Åsberg Depression Rating Scale (MADRS) scores versus placebo. As the complaint alleges, internal data likely revealed ALTO-100's limitations earlier, but disclosures omitted these risks.

This disconnect echoes biotech pitfalls: Early signals hyped as certainties, only for larger trials to expose flaws. Investors argue these statements weren't mere optimism—they were materially misleading, concealing ALTO-100's diminished efficacy.

Timeline of Alleged Misconduct and Disclosures

Class Period: February 2, 2024 – October 22, 2024

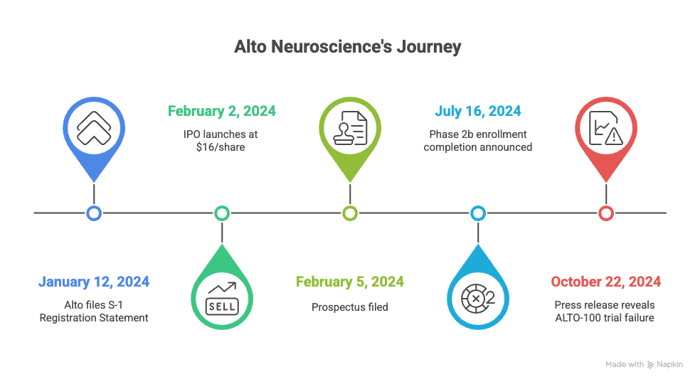

- January 12, 2024: Alto files its S-1 Registration Statement, touting ALTO-100's novel mechanism and biomarker platform. Amendments follow, declared effective February 1.

- February 2, 2024: IPO launches at $16/share. Stock begins trading on NYSE as ANRO, amid promises of precision psychiatry revolution.

- February 5, 2024: Prospectus filed, incorporating Registration Statement. Per the complaint, no red flags on ALTO-100's risks beyond standard boilerplate.

- July 16, 2024: Alto announces Phase 2b enrollment completion, reiterating confidence. Stock holds steady around $12-15.

- October 22, 2024: Bombshell press release: "ALTO-100 in patients with [MDD] did not meet its primary endpoint... compared to placebo." Shares plummet 69.99% to $4.36 on October 23.

Investor Harm and Market Reaction

The harm was swift and severe. From IPO highs near $16, ANRO traded above $10 through mid-2024. The October 22 disclosure erased $10.17 per share overnight—69.99%—wiping out over $200 million in market cap.

Market reactions were brutal. Pre-market trading on October 23 saw 60% drops, closing at $4.36. Subsequent volatility persisted, with shares dipping below $4 before partial recoveries on other pipeline news. For fund managers, this exemplifies biotech's binary risks—success lifts all, failure sinks the ship.

Litigation and Procedural Posture

The suit, filed in Northern California, asserts claims under Sections 11 and 15 of the Securities Act (negligent misstatements in Offering Documents) and Sections 10(b) and 20(a) of the Exchange Act (fraudulent statements), plus Rule 10b-5.

Defendants include Alto; CEO Amit Etkin; CFO Nicholas Smith; and directors Po Yu Chen, Christopher Nixon Cox, Chris Dimitropoulos, Andrew Dreyfus, Michael Liang, Aaron N.D. Weaver, and Gwill York. Scienter allegations hinge on executives' access to trial data and motive—post-IPO sales aren't detailed, but control over disclosures implies recklessness.

No confidential witnesses in the excerpt, but the complaint relies on public contrasts between promises and results. Filed on July 21, 2025, it's early-stage; lead plaintiff motions likely pending. If surviving, discovery could reveal internal emails on ALTO-100 doubts.

Shareholder Sentiment

Shareholders didn't mince words as ANRO's story soured. On platforms like X (formerly Twitter), Reddit, and StockTwits, reactions shifted from cautious optimism to outright frustration post-October 2024.

Before the drop, sentiment leaned positive. Users praised Alto's biomarker innovation: "ANRO could change psychiatry forever," one X post mused in September 2024, echoing pipeline updates. StockTwits buzzed with "buy the dip" calls amid minor volatility.

The October revelation flipped the script. "Total disaster—ALTO-100 flop tanks stock 70%. Lawsuit incoming?" queried a Reddit thread in r/stocks, garnering 200+ upvotes. On X, a post highlighted later positive news like EEG biomarker replication, but replies dripped skepticism: "Too little, too late after that MDD fail."

Trends showed a split. Long-term holders defended the platform such as one user commenting, "[o]ne trial down, but pipeline lives” while day traders lamented: "Burned on biotech again." StockTwits sentiment scores plunged to "bearish", with quotes like "[m]anagement overhyped, shareholders pay."

By 2025, as the lawsuit gained traction, posts trended toward recovery hopes. However, the overall arc traced betrayal, sentiment being early faith in precision medicine yielding to demands for accountability.

Analyst Commentary

Analysts turned sharply bearish after the ALTO-100 failure, slashing targets and questioning Alto's core thesis.

Pre-drop, optimism reigned. In August 2024, Wedbush rated Outperform with $29 target, citing "robust pipeline." Baird echoed at $29, praising biomarker replication.

Post-October 22, downgrades hit hard. Wedbush dropped to Neutral, target $4, with the miss raising fundamental doubts on the platform's predictive power. Baird followed suit, $29 to $10, noting efficacy concerns undermine confidence.

Consensus shifted: TipRanks averaged $9.25 (high $13, low $4), implying 138% upside from $4 lows but far below pre-fail highs. Zacks highlighted $4-15 range, a 181% potential rise yet signaling caution.

Later reports, like Fintel's $10.54 average, noted partial rebounds on other candidates. MarketBeat's seven analysts averaged $8.50, with "Moderate Buy" holds.

SEC Filings & Risk Factors

Alto's SEC filings disclosed risks, but plaintiffs argue they understated ALTO-100 specifics.

The S-1 Registration Statement (January 2024) warned generically: "Our product candidates may fail to show safety, tolerability, or efficacy[,]” with the general warnings that clinical trials are expensive, time consuming, and difficult to design. On biomarkers: "[O]ur approach to utilizing our Platform to identify biomarkers and conducting clinical trials in patient populations expressing certain biomarkers has not been validated and may not prove to be successful."

The Prospectus echoed that if the product candidates do not perform as expected in clinical trials, the business would be harmed. Yet, it touted ALTO-100's evidence of pro-neurogenesis without quantifying failure odds.

Post-IPO, the March 2024 10-K reiterated: "General economic... and other factors" could impact, but omitted ALTO-100 trial baselines. The October 22, 2024, 8-K press release admitted the miss: "ALTO-100 did not meet its primary endpoint," citing common AEs like headache but no efficacy.

Quarterlies (e.g., Q2 2024 10-Q) flagged "risks related to clinical development," but plaintiffs claim omissions: No warnings on memory-based biomarker's limitations or overstated prospects. Management's forward-looking statements hedged with "believe," but the suit contends these masked known weaknesses.

Filings like the 2023 10-K precursor noted 90% CNS failure rates yet positioned Alto as exceptional—fueling allegations of inadequate disclosure.

Conclusion: Implications for Investors

Biotech dreams die hard, but Alto's saga teaches vigilance. Red flags? Overreliance on unproven platforms, hyped early data, and generic risks masking specifics. For similar firms, such as precision medicine startups or CNS players, scrutinize biomarker validation and trial designs.

Investors: Diversify beyond binaries; probe scienter in lawsuits for recovery potential. Broader lesson: In volatile sectors, promises are placeholders until data delivers. Alto's fall isn't isolated—it's a cautionary echo for the next big thing. Watch the case; it could reshape how biotech companies disclose uncertainties.

![RxSight, Inc. (RXST) Securities Class Action Lawsuit Update [September 16, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/rxsight-securities-lawsuit-blog-banner-1.webp)

![Fiserv, Inc. (FI) Securities Class Action Lawsuit Update [September 25, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/fiserve-inc-securities-class-action-blog-banner.webp)