![Neogen Corporation (NEOG) Securities Class Action Lawsuit Update [September 10, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/neo-shareholder-lawsuit-blog-banner.webp)

Neogen Corporation said the integration was off to a great start. It wasn’t.

Caption: Operating Engineers Construction Industry and Miscellaneous Pension Fund v. Neogen Corporation, et al.

Case No.: 1:25-cv-00802

Jurisdiction: U.S. District Court, Western District of Michigan

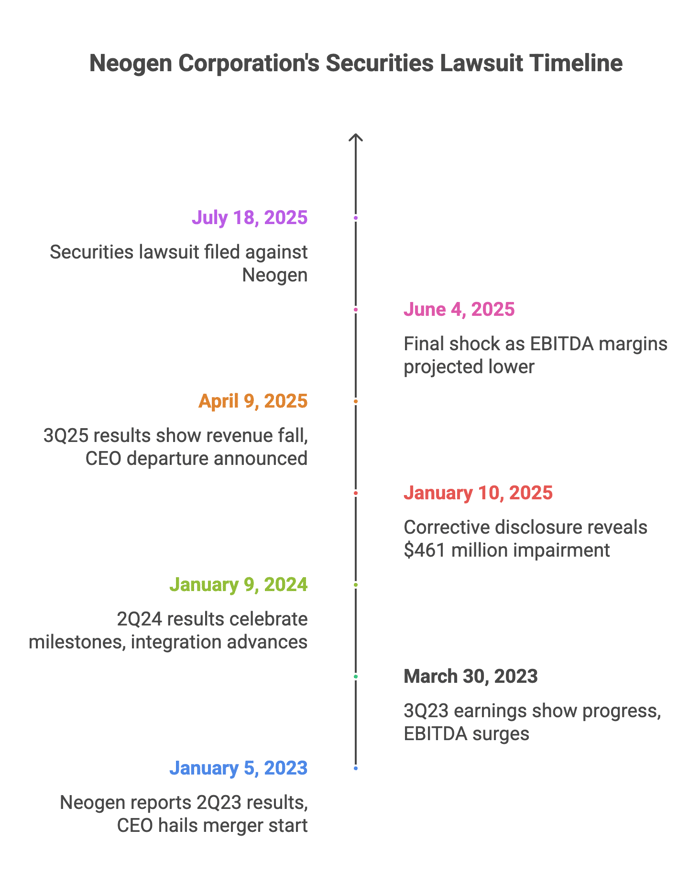

Filed on: July 18, 2025

Class Period: January 5, 2023 – June 3, 2025

Introduction

Neogen Corporation (NEOG) is facing a securities lawsuit. On July 18, 2025, a complaint was filed against Neogen and two of its top executives. Plaintiffs alleges that Neogen and executives John Adent and David Naemura misled investors about the integration of 3M’s Food Safety Division, acquired in a $5.3 billion deal closed in September 2022.

The class period spans January 5, 2023, to June 3, 2025, a stretch marked by glowing assurances of progress that masked deepening inefficiencies. What triggered the suit? A series of disclosures revealing goodwill impairments, slashed guidance, and operational stumbles that erased $4 billion in market value.

Investors now face the stark reality of a 79% stock plunge, culminating in a June 4, 2025, drop to $4.96 per share. This piece dissects the allegations, traces the business undercurrents, and weighs the implications—offering fund managers and class counsel a lens into potential recoveries and red flags ahead.

Backdrop and Business Context

Neogen Corporation, headquartered in Lansing, Michigan, has built its foundation on safeguarding the food chain. Founded in 1982 as a spin-off from Michigan State University, the company went public in 1989, trading under NEOG on NASDAQ. It operates in two segments: Food Safety, which develops diagnostic tests for pathogens, allergens, and residues in human and animal feed; and Animal Safety, supplying veterinary instruments, pharmaceuticals, and genomics services.

Growth came through acquisitions, a strategy that peaked with the 2022 merger of 3M’s Food Safety Division. Valued at $5.3 billion, the deal promised synergies—combining Neogen’s consumables with 3M’s established diagnostics. Analysts called it a “great decision,” envisioning a resilient portfolio where 95% of revenues stemmed from recurring products. Yet, the integration’s complexity, involving systems, manufacturing, and supply chains, set the stage for the alleged misconduct. By 2023, as macroeconomic pressures mounted, the merger’s hidden fractures began to surface, turning a milestone into a millstone.

Investor Harm and Market Reaction

The toll is quantifiable, the pain acute. From a peak of $23.84, NEOG’s descent to $4.96 vaporized $18.88 per share, or $4 billion in capitalization. The January 10, 2025, disclosure triggered a 5% drop; April 9’s revelations, a 28% plunge on massive volume; June 4’s margin warning, another 17% slide.

Analysts reacted swiftly. William Blair downgraded to Market Perform on July 29, 2025, citing persistent issues. Guggenheim cut its price target to $10 from $13, maintaining Buy but acknowledging risks. Piper Sandler lowered to $5 from $6.40, Neutral. Market sentiment shifted: retail on Stocktwits turned “extremely bullish” pre-earnings to cautious post-drop, with volumes spiking. The harm extends beyond numbers—pension funds like the plaintiff, managing millions, saw portfolios gutted, fueling demands for remedies under Sections 10(b) and 20(a).

Litigation and Procedural Posture

The suit invokes Sections 10(b) and 20(a) of the Exchange Act, plus Rule 10b-5, alleging materially false statements about integration progress. Defendants: Neogen, Adent (CEO), and Naemura (CFO/COO). Scienter is inferred from their oversight roles and knowledge of core operations; no insider sales are detailed in the complaint excerpt, but access to non-public data supports claims of concealment.

No confidential witnesses appear in the provided pages, but the suit relies on public timelines. Procedural milestones: Filed July 18, 2025; jury trial demanded. Venue in Michigan ties to Neogen’s headquarters. As a class action, lead plaintiff motions loom, with potential for motions to dismiss testing loss causation and falsity. Broader stakes: if proven, recoveries could address the $4 billion wipeout, underscoring accountability in post-merger disclosures.

Shareholder Sentiment

Across platforms, shareholders grapple with betrayal and opportunity. On X (formerly Twitter), chatter around NEOG’s kin—misaligned but reflective—shows frustration with volatility. One user lamented a similar stock’s 75% drop despite a settlement: “How can a stock win a $15-$20 million lawsuit... and drop 80%? Some serious rigging.” Another eyed recovery: “This stock is at a discount... Massive Latest Drop.”

Reddit threads echo caution. In r/stocks, a 2022 post queried “how far can it fall” post-merger, with users warning of shorting pressures and “bloody hands from catching that falling knife.” A January 2025 note in r/UnderTheRadar highlighted CEO buys at $11, contrasting analyst skepticism. Sentiment shifted post-disclosures: pre-2025 optimism frayed into doubt, with users in r/dividends debating the 3M split-off as a “good option to exit” amid lawsuit fears.

On Stocktwits, sentiment swung from “extremely bullish” before April’s drop to “neutral” after, with volumes “high.” Posts decried the 59.3% YTD decline: “Neogen is down... trading 72.3% below its 52-week high.” Trends reveal a divide—long-term holders cling to turnaround hopes, while others flee, labeling it a “narrative violation.” The mood: weary resilience, with calls for management accountability growing louder.

Analyst Commentary

Professional voices have cooled, reflecting the integration’s toll. Post-June 2025 drop, William Blair downgraded NEOG to Market Perform on July 29, 2025, from Outperform, citing margin pressures and leadership changes. Guggenheim lowered its target to $10 from $13, retaining Buy but noting “elevated costs” from inefficiencies.

Piper Sandler adjusted to $5 from $6.40, Neutral, emphasizing the Q4 margin warning’s drag. Seeking Alpha pieces framed NEOG as a “bottom fishing” play, with potential via asset sales but risks in debt-laden turnaround. Average target: $6.50, implying modest upside from $5.66, with a consensus Hold from four analysts.

Pre-disclosures, optimism reigned—William Blair’s Outperform echoed merger synergies. Post-drop, commentary turned reflective: Zacks cut Q1 2026 EPS to $0.03 from $0.05. Broader take: while defensive traits (consumables revenue) persist, integration scars warrant caution, with upgrades hinging on efficiency gains.

SEC Filings & Risk Factors

Q2 2025 10-Q (filed January 2025) detailed the $461 million charge, attributing it to “integration challenges” and market conditions. An 8-K on April 9, 2025, announced Adent’s departure and guidance cuts, disclosing material weaknesses in controls over financial reporting.

Omitted, per the suit: the immediacy and severity of inefficiencies. Management discussions in MD&A sections touted progress—such as huge strides in 2024—while burying warnings. Post-June 2025, an 8-K reiterated margin drops, underscoring the gap between boilerplate risks and alleged realities.

Conclusion: Implications for Investors

This case etches a reminder: mergers glitter, but integrations grind. For investors in acquisitive firms—think healthcare or tech sectors—scrutinize post-deal disclosures beyond surface synergies. Red flags? Repeated guidance cuts, impairment charges, leadership exits. Broader relevance: in a post-SPAC era of hasty combinations, due diligence on controls and timelines proves paramount. Fund managers might hedge via options; class counsel, pursue robust scienter evidence. Neogen’s saga isn’t closure—it’s a reckoning, urging vigilance where promises meet performance.

![Alto Neuroscience, Inc. (ANRO) Securities Class Action Lawsuit Update [September 10, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/anro-shareholder-alert-blog-banner.webp)

![Replimune Group, Inc. (REPL) Securities Class Action Lawsuit [September 8, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/replimune-securities-lawsuit-blog-banner-v2.webp)