Table of Contents

- How Do Companies Make the Leap From Private to Public?

- What Happens in an IPO?

- What Have the Courts Said About IPOs?

- What Should Investors Expect During an IPO? What are the Risks?

-

- A Final Reflection

- Frequently Asked Questions About IPOs

- What does IPO stand for in finance?

- How does the IPO process work?

- What role do underwriters play in an IPO?

- What’s an IPO prospectus?

- What’s lock-up period in an IPO?

- How is an IPO price figured out?

- Why do companies even want to go public through an IPO?

- What risks should investors think about before getting IPO stock?

- Do any government agencies regulate IPOs?

- What’s the difference between an IPO and a direct listing?

- What is the difference between a public company and a privately held company?

- What is a preliminary prospectus?

- Who decides how many IPO shares are sold and sets the share price?

- What is the underwriting process, and how does it work?

- How does an investor purchase shares in the initial public offering?

- What’s the difference between an IPO and debt financing?

- What happens if a company misleads the public on its IPO paperwork?

- You Can Also Read

The letters IPO get tossed around like everyone should already know what they mean. But, they’re actually quite complex to navigate and understand! What is an IPO?

An initial public offering (IPO) is the moment when a private company sells stock to the public for the first time, as a publicly traded company. It’s billed as a launch into legitimacy, a way for everyday investors to buy in. But behind the ticker symbol and celebratory bell-ringing is a process that is tightly regulated, full of risk, and often misunderstood.

How Do Companies Make the Leap From Private to Public?

A company begins in private hands—founders, employees, company insiders, and a set of early investors. In this closed circle, information flows freely. When a company decides it’s ready to “go public,” it chooses to swap privacy for disclosure. Every number, every risk, every relationship with customers or suppliers now must be laid bare in an SEC filing called a registration statement (also called Form S-1).

So why would any company go through all that hassle and paperwork? When a private company undergoes an IPO, it can generate major cash – and fast. Companies use that cash infusion for all sorts of things: paying down debt, expanding operations, or even providing some liquidity for private investors from the firm’s early days. The IPO is both a financial milestone and a legal one. Suddenly the company belongs to the market itself, including ordinary investors.

What Happens in an IPO?

A company hires underwriters (usually a big brokerage firm or bank) to manage the offering. These investment bankers usually have lots of IPO experience, and so they help set the share price range, gauge investors' interest, and ultimately allocate shares. Executives pitch their new company to institutional investors.

Once the Securities and Exchange Commission (SEC) reviews and declares the registration statement effective, the company and its bankers pick a final offering price. Shares are sold at the offering price, trading begins, and—if all goes to plan—the market rewards the company with liquidity and credibility. But not all IPOs soar. Some stumble out of the gate, and others collapse within months as reality undercuts the hype.

Because IPOs transform private companies into public ones, they carry not just financial but legal consequences. Courts have repeatedly weighed in on what companies must disclose during this critical moment.

What Have the Courts Said About IPOs?

Courts have long wrestled with how much companies must disclose at the IPO stage. In Gustafson v. Alloyd Co. (1995), the Supreme Court clarified that Section 12(a)(2) of the Securities Act, which provides a recission remedy for liability for misstatements in prospectuses, applies only to public offerings—not to private deals. That distinction cemented the IPO as a uniquely scrutinized moment in a company’s life.

More recently, in Omnicare, Inc. v. Laborers District Council (2015), the Court examined how opinions expressed in registration statements could mislead investors. The case made clear that IPO disclosures aren’t just about hard numbers—they also involve judgments and beliefs. If those judgments lack a reasonable basis, liability may follow.

These decisions underscore a simple point: the IPO is not just a business transaction. It is a legal event, one that courts will revisit if disclosures prove incomplete or misleading. If disclosures in an IPO registration statement are false or misleading, investors may bring lawsuits under Section 11 of the Securities Act to recover losses.

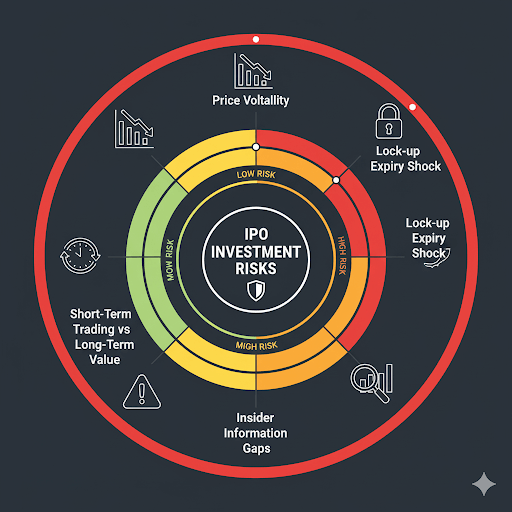

What Should Investors Expect During an IPO? What are the Risks?

For investors, IPOs can look like golden tickets—getting in on the ground floor of the next Amazon or Google. But the truth is messier. Prices are often volatile in the early days. Insiders may hold information advantages. And lock-up agreements, which prevent early investors from selling for a set period, can create sudden waves of supply once they expire.

The IPO also shifts the company’s priorities. Quarterly earnings reports and analyst expectations now hover over management. Decisions that once could be made quietly must now be justified to a market that can punish missteps instantly. For some companies, the scrutiny brings discipline. For others, it becomes a weight.

A Final Reflection

An IPO is often painted as a finish line—the confetti moment when years of work finally pay off. In truth, it is a starting line. From that day forward, the company operates under public law, public markets, and public judgment. The offering itself is a transaction; what follows is an open-ended story, shaped by competition, governance, and the unpredictable tide of investor sentiment.

For shareholders, the lesson is to treat IPOs not as guaranteed jackpots but as calculated risks. The disclosure documents are dense, but they are also the closest thing to a roadmap investors will get. Read them. Weigh the risks. Remember that behind the ringing bell, a company is stepping into a new, exposed life—one that is just beginning.

Frequently Asked Questions About IPOs

What does IPO stand for in finance?

IPO stands for “initial public offering.” It is the process by which a private company sells its shares to the public for the first time, usually by listing on a stock market exchange such as the NYSE or NASDAQ.

How does the IPO process work?

The IPO process begins when a company files a registration statement with the Securities and Exchange Commission (SEC). Investment banks, acting as underwriters, help the company's management team set the share price and market the stock to institutional investors. Once the SEC declares the registration effective, the company sells shares to the public and trading begins on the stock exchange.

What role do underwriters play in an IPO?

Underwriters are typically large investment banks that guide the IPO. They help prepare the prospectus, run investor roadshows, set the offering price, and allocate shares. Their role is to balance demand from investors with the company’s goal of raising capital.

What’s an IPO prospectus?

The IPO prospectus is part of the SEC registration statement. It contains detailed information about the company’s business, financials, risks, and the terms of the offering. Investors rely on the prospectus to make informed decisions before buying shares.

What’s lock-up period in an IPO?

A lock-up period is a contractual restriction that prevents insiders—such as company executives, employees, and early investors—from selling their shares immediately after the IPO. Lock-ups usually last 90 to 180 days, after which a surge in share supply can affect the stock price.

How is an IPO price figured out?

The IPO price is set during the book-building process, when underwriters gauge demand from institutional investors. They use this feedback, along with company fundamentals and market conditions, to set the final offering price.

Why do companies even want to go public through an IPO?

Companies go public to raise capital for growth, pay down debt, or provide liquidity for early investors. Going public also increases visibility and credibility, though it brings greater regulatory and market scrutiny.

What risks should investors think about before getting IPO stock?

Investors should consider the risk of volatility, the possibility of overvaluation, and the information gap between insiders and the public. Reviewing the company’s SEC filings, including risk factors in the prospectus, is critical before investing.

Do any government agencies regulate IPOs?

IPOs are regulated primarily by the Securities and Exchange Commission under the Securities Act of 1933. Companies must file detailed disclosures, and liability can attach if those disclosures are false or misleading. Stock exchanges like NASDAQ and NYSE also have listing requirements.

What’s the difference between an IPO and a direct listing?

In an IPO, new shares are created and sold to raise capital, often with underwriter support. In a direct listing, no new shares are issued; instead, existing shareholders sell their stock directly on the exchange, bypassing traditional underwriters.

What is the difference between a public company and a privately held company?

A public company has its shares listed on a stock exchange like the NYSE or NASDAQ, where anyone can buy or sell them. By contrast, a privately held company’s shares are owned by a limited group of founders, employees, or private investors, and are not available to the general public.

What is a preliminary prospectus?

A preliminary prospectus—sometimes called a “red herring”—is the first version of the IPO disclosure document filed with the SEC. It contains information about the company’s business, financial condition, and risks but may not include the final number of shares or the offering price. Investors and analysts use the preliminary prospectus to evaluate the company before the final prospectus is issued.

Who decides how many IPO shares are sold and sets the share price?

The number of IPO shares and the final price are determined jointly by the company and its underwriters. The company decides how much capital it wants to raise by selling a portion of the company’s shares to the public. Underwriters then use investor demand, market conditions, and valuation models to recommend the final share price.

What is the underwriting process, and how does it work?

The underwriting process is when investment banks (the underwriters) manage the IPO. They sign an agreement with the company, prepare the registration statement, market the offering to investors, and take on the risk of buying and reselling the company’s shares. Underwriting can be "firm commitment" (where underwriters buy and resell shares) or "best efforts" (where they only market them), with firm commitment being more common for large IPOs. This process ensures the company raises the capital it seeks while investors gain access to the new stock.

How does an investor purchase shares in the initial public offering?

Most investors buy IPO shares through brokerage firms that have access to the newly listed company's offering. Allocation is often limited, and priority is usually given to institutional investors or clients of the underwriters. Retail investors typically gain access once the shares begin trading on the exchange. Investors should realize IPO investments could carry risk and should consult a financial advisor before making those investments.

What’s the difference between an IPO and debt financing?

An IPO raises money by selling ownership stakes—shares of the company—to the public. Debt financing, on the other hand, means the company borrows money through loans or bonds and must repay it with interest. IPOs dilute ownership but don’t require repayment, while debt preserves ownership but creates ongoing financial obligations.

What happens if a company misleads the public on its IPO paperwork?

If a company misleads investors in its IPO filings, it can face lawsuits under the Securities Act of 1933, and investors may seek damages for false or incomplete disclosures. The SEC can also bring enforcement actions, leading to fines or other penalties.

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or investment advice. Securities laws are complex and subject to change. Consult a qualified professional for advice tailored to your situation.

![Fiserv, Inc. (FI) Securities Class Action Lawsuit Update [Sept 15, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/fiserve-shareholder-alert-blog-banner.webp)

![Replimune Group, Inc. (REPL) Securities Class Action Lawsuit [September 8, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/replimune-securities-lawsuit-blog-banner-v2.webp)