Shareholder Alert: California Court Allows Stitch Fix Fraud Claims to Proceed, Dismisses Control Person Claims

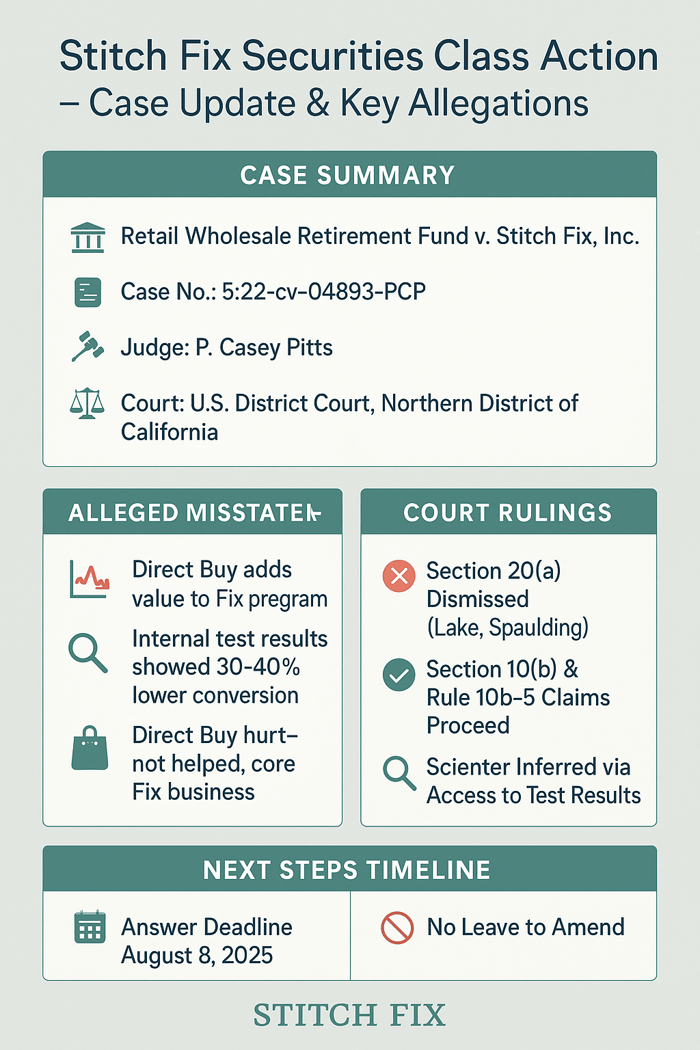

Case Name: Retail Wholesale Retirement Fund v. Stitch Fix, Inc.

Case No. 5:22-cv-04893-PCP

Jurisdiction: U.S. District Court, Northern District of California

Judge P. Casey Pitts

Summary

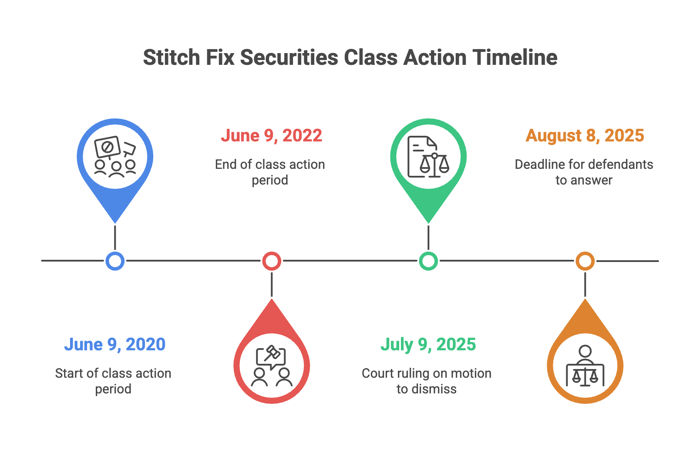

On July 9, 2025, Judge P. Casey Pitts partially granted a motion to dismiss in Retail Wholesale Retirement Fund v. Stitch Fix, Inc., dismissing with prejudice Section 20(a) claims against former executives Katrina Lake and Elizabeth Spaulding. The Court allowed Section 10(b) and Rule 10b-5 claims against Stitch Fix, Lake, and Spaulding to move forward, finding four statements about the Direct Buy program’s benefits were misleading based on internal test results showing harm to the core Fix business.

Underlying Lawsuit

Plaintiffs represent Stitch Fix shareholders from June 9, 2020, to June 9, 2022. The complaint alleged StitchFix, Lake (founder and ex-CEO), and Spaulding (ex-president and CEO) violated Section 10(b) of the Securities Exchange Act and SEC Rule 10b-5. The complaint also alleged Lake and Spaulding violated Section 20(a) of the Act.

The lawsuit focuses on Stitch Fix’s Direct Buy program (initially called “Shop” and later branded “Freestyle”). Direct Buy allowed customers to purchase individual items directly; by contrast, in the Fix program stylists curated clothing boxes for subscribers. Plaintiffs say Defendants misrepresented Direct Buy as an complementary to the Fix program, which is the company’s core business. Direct Buy was meant to add value to the Fix business, not cannibalize from it.

From June 2020 to September 2021, StitchFix kept telling investors (in various earnings calls, letters, and conference) that Direct Buy would add value to Fix, attract new customers, and increase spending. The company assured investors Direct Buy would not harm the core Fix business. However, internal testing allegedly undermined those claims. Those tests showed Direct Buy customers converted to Fix at 30-40% lower rates than expected, spent less, and were less likely to return compared to Fix customers. These tests indicated Direct Buy was, in fact, cannibalizing Fix. Once investors learned the truth, StitchFix’s stock price dropped 90%.

Defendants’ Motion to Dismiss Arguments

Defendants sought dismissal under Rule 12(b)(6), asserting:

Falsity: Statements about Direct Buy’s complementarity applied only to existing customers, not prospective ones, and lacked specific contradictory test results. Thus, the statements were not necessarily false.

Scienter: No evidence showed Defendants knew of negative test results by December 2020, negating intent or recklessness.

Safe Harbor/Puffery: The alleged false statements were forward-looking or vague corporate optimism, so they’re protected under the PSLRA.

Plaintiffs’ Opposition

Plaintiffs said Direct Buy was used by both current and new customers, which made the company’s public statements misleading (especially given the internal testing results). Spaulding regularly saw these test results in weekly team presentations, while Lake had access through the company’s tracking system. Both executives were closely involved because Direct Buy was a major part of the company’s growth strategy. They thus had adequate knowledge to meet the scienter requirements.

Court’s Ruling

The Court dismissed, with prejudice, the Section 20(a) claims against Lake and Spaulding. Since Lake and Spaulding made the allegedly false statements themselves, there was no need for a control liability claim (under Section 20(a)). Section 10(b) and Rule 10b-5 claims against Stitch Fix, Lake, and Spaulding were upheld for four statements.

Court’s Rationale

Falsity

Four statements claiming Direct Buy was additive and complementary were deemed misleading. The complaint alleged Direct Buy was available to existing and prospective customers, and tests revealed new customers bought less and were 30-40% less likely to convert than Fix customers. Defendants’ failure to disclose these results violated their duty to avoid misleading investors. The Court rejected claims of puffery or safe harbor, as the statements cited specific data and outcomes.

Scienter

Spaulding’s weekly reviews of test results in Google Slides and Lake’s access to the A/B database, combined with Direct Buy’s “transformational” status, supported a strong inference of scienter. The Court found it implausible that executives were unaware of adverse data, meeting PSLRA standards.

Loss Causation

The Court accepted Plaintiffs’ claim of a $6 billion market value drop after Direct Buy’s negative impact was revealed, finding it sufficient at this stage.

Final Disposition and Next Steps

Section 20(a) claims are dismissed with prejudice. Section 10(b) and Rule 10b-5 claims against Stitch Fix, Lake, and Spaulding proceed. Defendants must answer by August 8, 2025. No leave to amend was granted due to prior amendments.