![XPLR Infrastructure (XIFR) Securities Class Action Lawsuit Update [August 18, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/xplr-infrastructure-xifr-lawsuit-blog-banner.webp)

Introduction to XPLR Infrastructure (XIFR) Securities Class Action Lawsuit

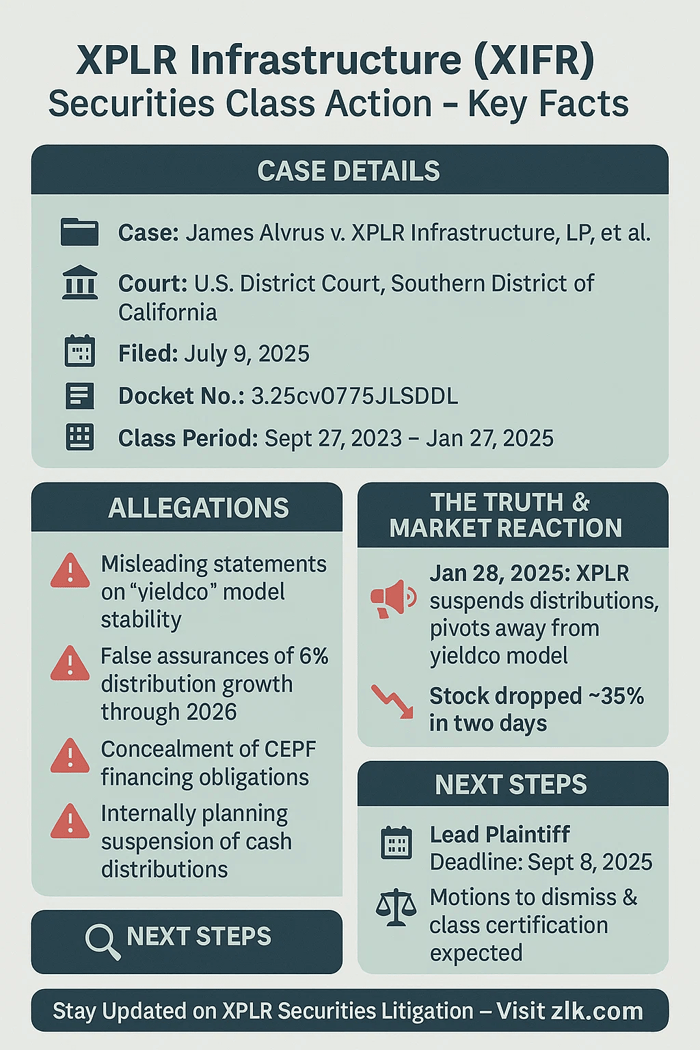

A securities class action has been filed against XPLR Infrastructure, LP (NYSE: XIFR), formerly known as NextEra Energy Partners, LP. The suit is behalf of people who got XPLR stock between September 27, 2023 and January 27, 2025 (the “Class Period”).

Plaintiffs accuse defendants of making materially false and misleading statements and failing to disclose adverse facts about the sustainability of XPLR’s business model and its ability to maintain unit holder cash payouts through at least 2026.

On January 28, 2025, XPLR announced it would suspend all distributions to common unitholders and pivot away from its yieldco model. The price of XPLR’s common units fell sharply following the announcement. Now, investors are suing.

XPLR Infrastructure (XIFR) Securities Lawsuit Case Details

Case Name: Alvrus v. XPLR Infrastructure, LP, et al.

Docket Number: 3:25cv01755JLSDDL

Court: U.S. District Court, Southern District of California

Filing Date: July 9, 2025

XPLR Infrastructure (XIFR) Company Profile

XPLR is engaged in the acquisition, ownership, and management of contracted clean energy projects in the United States, including wind and solar facilities, and previously, a natural gas pipeline. It was controlled by NextEra Energy, Inc. during the Class Period.

Class Period

September 27, 2023 – January 27, 2025

XIFR investors who purchased XIFR common stock during the class period might be eligible to join the XPLR infrastructure securities class action lawsuit.

Allegations in the XPLR Infrastructure (XIFR) Class Action Lawsuit

Plaintiffs say XPLR, NextEra energy, Inc., and some of XPLR’s executives made false and misleading statements about XPLR’s business. The case focuses on XPLR’s execs repeated assurance the company’s “yieldco” business model was secure. The also said unitholder cash distributions would continue to grow at an annual rate of approximately 6 percent through at least 2026. These assurances appeared in a series of public statements, including press releases, SEC filings, and quarterly earnings calls.

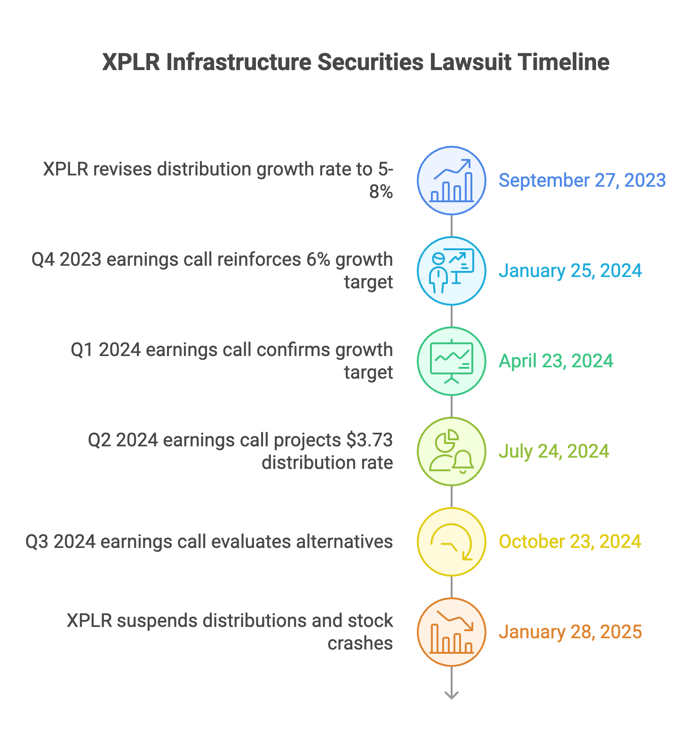

On September 27, 2023, XPLR issued a press release revising its limited partner distribution growth rate to a range of 5 to 8 percent per year, explicitly targeting 6 percent “through at least 2026.” The release emphasized that the planned sale of natural gas pipelines and the scheduled buyouts of convertible equity portfolio financings (CEPFs) due through 2025 meant that no growth equity would be needed until 2027. This message was reinforced on the January 25, 2024 Q4 2023 earnings call, when Ketchum told investors the partnership was “executing against the partnership’s transition plans” while maintaining the 6 percent growth target through at least 2026. Crews added that proceeds from the Texas Pipeline portfolio sale were sufficient to complete the NEP Renewables II CEPF buyouts scheduled for June 2024 and June 2025, again asserting that growth equity would not be required until 2027.

The same theme carried forward on April 23, 2024, when Crews, on the Q1 2024 earnings call, reiterated the 6 percent distribution growth target, confirmed adequate proceeds for the upcoming CEPF buyouts, and described the nearterm CEPF plan as “well understood.” He repeated that the partnership did not expect to require growth equity until 2027. On July 24, 2024, during the Q2 2024 earnings call, Bolster affirmed the 6 percent growth target “through at least 2026” and projected a Q4 2024 annualized distribution rate of $3.73 per common unit. Ketchum assured analysts, “we have time” in 2024 and “don’t have growth equity needs until ’27.”

By October 23, 2024, on the Q3 2024 earnings call, Bolster disclosed that XPLR was evaluating alternatives to address remaining CEPF obligations and intended to conclude its review by Q4 2024, at which time it would provide updated distribution and runrate cash available for distribution (CAFD) expectations. Throughout this period, the company’s SEC filings echoed these public statements, presenting the distribution growth target as sustainable and supported by sufficient liquidity to meet CEPF obligations without issuing growth equity before 2027.

The complaint alleges that these repeated assurances — viewed in light of the company’s financial condition — were materially false and misleading when made. Internally, the Company was already struggling to sustain XPLR's yieldco business model, lacked the means to resolve CEPF financings before maturity without significant dilution, and defendants planned to suspend cash distributions to redirect funds toward those financing obligations.

The Truth Emerges

On January 28, 2025, XPLR announced a “strategic repositioning,” moving away from its yieldco structure and halting cash distributions to common unitholders for an indefinite period. The company stated that retained cash flows would be used to buy out certain CEPFs and invest in existing assets.

Market Reaction

XPLR’s stock crashed after January 2025 revelation. The stock plunged nearly 35 percent in two days.

Next Steps

Lead Plaintiff Deadline: Submissions for lead plaintiff are due by September 8, 2025.

The Court will appoint a lead plaintiff and counsel.

Procedural steps may include motions to dismiss and class certification.

To learn if you are eligible for recovery under the XPLR securities class action lawsuit, visit the case submission page here.

Disclaimer - This summary is based solely on allegations in the filed complaint. It is provided for informational purposes only and does not constitute legal advice. No outcome is guaranteed. Investors should consult their own counsel regarding rights or potential claims.

![Centene Corporation (CNC) Securities Class Action Lawsuit Update [August 18, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/cnc-banner-imagewebp.png)