Table of Contents

In 2015, the Financial Industry Regulatory Authority sanctioned LPL Financial (a major U.S. broker-dealer) because LPL didn’t properly supervise brokers who misled clients about complex investments. The case wasn’t headline material. No celebrity CEO, no billion-dollar Ponzi scheme. But for the retirees and first-time investors who lost savings they thought were safe, it was everything.

The misconduct wasn’t about fraud in the cinematic sense. It was about unsuitable recommendations, hidden risks, and a system that didn’t catch the problem until after the damage was done. FINRA ordered the firm to pay $10 million. The investors didn’t get their full money back. But they got something . . . because FINRA acted.

That’s why FINRA matters so much -- especially when the stakes feel small to everyone except the person who lost everything.

A Watchdog Built Inside the Fence

FINRA isn’t the SEC. It isn’t a judge. And it doesn’t pass laws. But in many cases, it’s the most immediate layer of accountability for the people managing your investments. FINRA operates under the supervision of the U.S. Securities and Exchange Commission (SEC), which must approve its rules and can overrule its decisions.

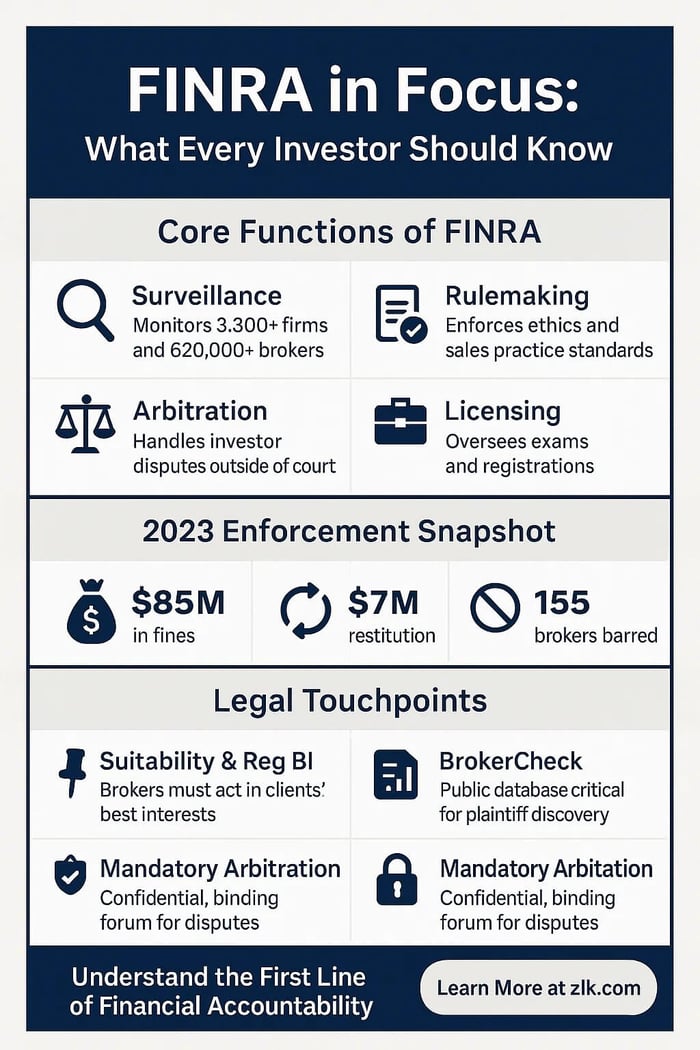

Officially, FINRA is a Self-Regulatory Organization (SRO). SROs are a private entity with a public mandate. FINRA’s predecessor was created after Securities Exchange Act of 1934, which allowed for financial SROs. It got restructured in 2007, resulting in FINRA. The Authority now writes the rulebook for all sorts of financial professionals involved with the market. It also enforces ethical standards and administers arbitration forums for disputes between investors and firms.

FINRA’s got over 3,300 brokerage firms and more than 620,000 registered individuals under its eye. Every financial advisor who sells securities must pass FINRA-administered exams. Every brokerage firm must comply with FINRA rules. And many customer complaints that don’t rise to the level of federal litigation plays out in FINRA arbitration, not a courtroom.

FINRA isn’t a passive observer. In 2023 alone, it levied over $85 million in fines, ordered $7 million in restitution, and barred 155 brokers from the industry. Its reach is real. Its power is structural. And in securities litigation—especially where broker misconduct or firm oversight is involved—you cannot tell the full story without FINRA.

Where FINRA Ends and Class Actions Begin

Most federal securities lawsuits fall under SEC Rule 10b-5, targeting publicly traded companies and alleged corporate fraud. These are the big-ticket cases . . . the sort where stock prices drop overnight after bad news, and shareholders claim they were misled.

But a significant subset of securities cases—especially those involving retail investors, high-risk products, or bad financial advice—are deeply intertwined with FINRA’s regulatory structure.

Key FINRA-related legal concepts include:

- Suitability: Brokers must recommend investments appropriate for the customer’s financial profile;

- Best Interest Obligations: Under Reg BI, brokers must prioritize the customer’s interests;

- Supervisory Failures: Firms must supervise their brokers and can be liable for lapses.

For instance, consider a rule known as Regulation Best Interest (Reg BI). It’s a standard enforced by both the SEC and FINRA. Reg BI is an SEC rule, but FINRA plays a critical role in enforcing it through its disciplinary and examination functions. Under Reg BI, brokers must act in the best interests of their customers, disclosing conflicts, assessing client needs, and recommending only those investments that fit.

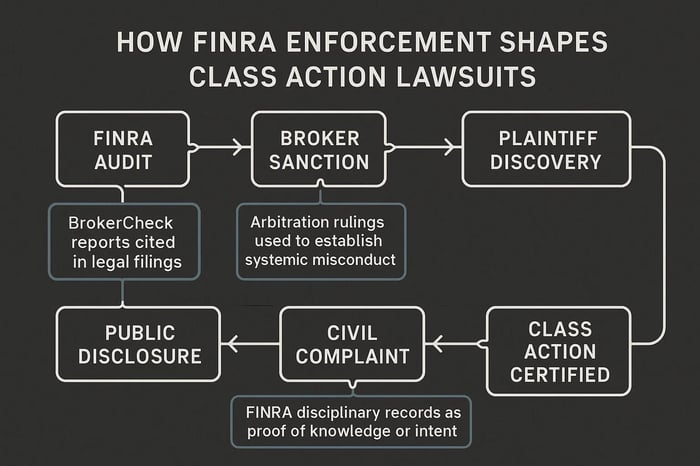

When firms breach that duty, FINRA investigations often lead the charge. But private plaintiffs—especially in class action suits—rely on the paper trail created by FINRA’s work. Public disciplinary reports, audit findings, and broker disciplinary histories help prove knowledge, intent, and systemic failure.

Even when a lawsuit isn’t filed under FINRA rules, the story starts there.

When the Courtroom Is Closed: FINRA Arbitration

One of the most defining—and controversial—aspects of FINRA’s power is its arbitration system.

Almost every investor who opens a brokerage account signs a mandatory arbitration clause. That clause posits that if something goes wrong, you can’t sue us in court. You have to go through FINRA.

This means:

- No jury

- Limited discovery

- Confidential decisions

- Narrow grounds for appeal

Supporters argue that arbitration is faster and cheaper. Critics point out that it’s opaque and sometimes biased, especially when industry-affiliated arbitrators are involved.

But regardless of opinion, arbitration is the default path for most retail investor claims. In 2022, FINRA received 2,671 new case filings. About 40% of cases that reached a hearing resulted in an award for the investor.

In a 2022 example, FINRA awarded nearly $1 million to customers who had been steered into unsuitable option strategies by a broker chasing commissions. The customers’ claim never made it to court. It was FINRA—or nothing.

For securities law attorneys, knowing how to navigate FINRA’s procedural terrain—how to frame claims, how to read panel tendencies, how to leverage enforcement records—is often as important as knowing how to file in federal court.

Case Story: FINRA v. Oppenheimer & Co.

In Department of Enforcement v. Oppenheimer & Co., Inc. (2016), FINRA brought an action against the firm for failing to supervise brokers who sold leveraged ETFs to clients who didn’t understand the risk. These products are designed for short-term trading and can cause rapid losses if held too long. But brokers sold them to retirees and conservative investors as if they were standard holdings.

The issue was the investments weren’t suitable for those clients. The firm’s internal controls failed to flag the pattern. FINRA stepped in, fined the firm $2.25 million, and required restitution of $716,000 to affected customers.

The decision did more than penalize bad behavior. It established a standard—that firms can’t look away when brokers chase commissions with risky tools. That ruling has since been cited in civil complaints and arbitration proceedings involving similar facts.

This is the quiet power of FINRA: it doesn’t always get headlines, but it builds the floor that future accountability stands on.

The Structural Role FINRA Plays

FINRA is not a neutral observer. It actively shapes the ecosystem in which securities cases are brought, argued, and resolved. Consider the following:

- BrokerCheck: FINRA’s public database, reveals disciplinary history and customer complaints. Plaintiffs’ attorneys use it to assess credibility and identify patterns of misconduct.

- Supervisory Failures: documented in FINRA sanctions, can form the basis for control-person liability or negligent supervision claims.

- Arbitration Awards: can reveal systemic misconduct that supports class actions or SEC referrals.

And because FINRA enforcement is often faster than federal litigation, its findings can influence market reaction, media narratives, and shareholder sentiment long before a judge issues an order.

For attorneys pursuing securities fraud claims, understanding FINRA’s rules, enforcement priorities, and historical posture is essential. It’s not just background. It’s the framework.

A Closing Reflection on Responsibility

When investors ask, “How did this happen?” they’re rarely wondering about Latin phrases or jurisdictional rules. They’re asking why no one stopped the harm sooner. In theory, that’s FINRA’s job. But the truth is more complicated.

Because FINRA is industry-funded, some critics say it pulls punches. Because it’s faster than courts, others say it moves too quietly. Because it governs the first layer of contact between investors and the market, it’s easy to blame when trust breaks.

And yet, without FINRA, there would be fewer answers. Less oversight. Fewer paper trails. No arbitration forums. No enforcement records. No BrokerCheck.

It may not catch everything. It may not move fast enough. But when the question is “Who should have seen this coming?”, FINRA is often the first name on the list.

And that makes it indispensable—especially when the courtroom is just the second act.

![iRobot Corporation (IRBT) Securities Class Action Lawsuit Update [August 15, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/irobot-securities-lawsuit-blog-banner.webp)

![Rocket Pharmaceuticals, Inc. (RCKT) Securities Class Action Lawsuit Update [July 16, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/rocket-pharma-rckt-securities-lawsuit-blog-banner.webp)

![Centene Corporation (CNC) Securities Class Action Lawsuit Update [August 18, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/cnc-banner-imagewebp.png)