![DexCom, Inc. (DXCM) Securities Class Action Lawsuit Update [November 11, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/dxcm-alert-plus-banner.webp)

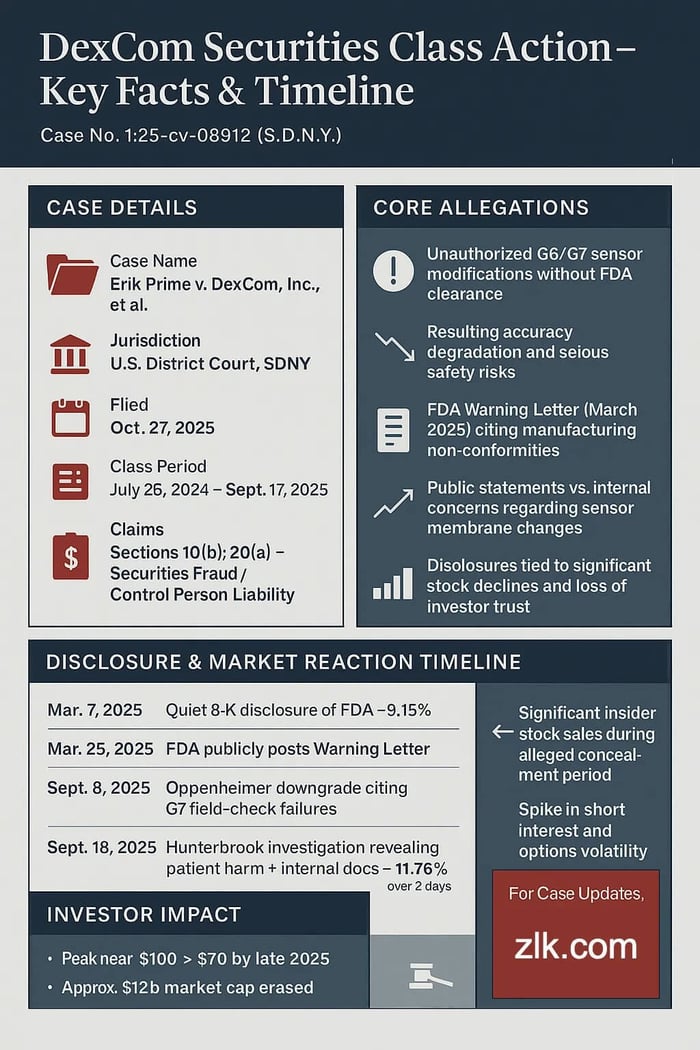

Case Name: Prime v. Dexcom, Inc., et al.

Case No.: 1:25-cv-08912

Jurisdiction: U.S. District Court, Southern District of New York

Filed on: October 27, 2025

Class Period: July 26, 2024 – September 17, 2025

Introduction

DexCom promised diabetic patients — and investors — a revolution in glucose monitoring characterized by precision, reliability, and life-changing accuracy. However, federal court filings now reveal a darker reality: secret sensor modifications to the G6 and G7 devices that were never cleared by the FDA, resulting in wildly inaccurate readings, hospitalizations, and even deaths. All the while, executives touted these "enhancements" and sold millions in stock. The outcome is a securities class action that could redefine accountability in the medtech industry. For fund managers holding DXCM, the question isn't just about recovery — it's about whether trust in the entire CGM sector has been fatally compromised.

Erik Prime v. DexCom, Inc. et al. isn't another routine securities suit. It's a story of corporate ambition colliding with patient safety, told through FDA warning letters, leaked internal documents, and grieving families. Lead plaintiff Erik Prime alleges that between July 26, 2024, and September 17, 2025 (the Class Period), DexCom (NASDAQ: DXCM) systematically misled investors about material changes to its flagship G7 sensor — changes that made the device less accurate, more dangerous, and ultimately triggered a cascade of disclosures that erased billions in market value.

Claims focus on Sections 10(b) and 20(a) of the Securities Exchange Act, framed as classic fraud-on-the-market allegations with profound implications since real people allegedly died as a result of prioritizing margins over validation.

Backdrop and Business Context

DexCom didn't invent continuous glucose monitoring, but it perfected the wearable model. Founded in 1999 and IPO'd in 2005, the San Diego-based company capitalized on the diabetes epidemic to become a $30 billion-plus powerhouse. The G6 (2018) brought CGM to mainstream users, while the G7 (2023) was marketed as an unbreakable advancement with a smaller form factor, faster warm-up times, over-the-air updates, and seamless integration with insulin pumps from Tandem and Insulet.

Manufacturing scaled aggressively, with new high-volume plants in Mesa, Arizona, and Malaysia targeting gross margins surpassing 70%. By 2024, the G7 represented the future, with executives stating that transitioning users from G6 to G7 would drive "steady progress towards our long-term cost targets." What was left unsaid is that these cost reductions allegedly involved swapping sensor components without notifying the FDA — a violation that rendered the medical device adulterated under federal law. Facing competition from Abbott's FreeStyle Libre, DexCom placed all bets on G7 dominance, which the lawsuit claims was rigged from the outset.

Promises Made vs. Reality

Kevin Sayer claimed on a July 25, 2024 earnings call, “We’ve built upon the performance of G7, making it even better." CFO Sylvain added that the company “continued ramp up of our high-volume manufacturing facilities” and promised “steady progress towards our long-term cost targets."

During the October 2024 earnings call, Sayer reiterated, "The accuracy of DexCom is tried and true and proven to these patients.” He added, “We update our hardware and our app experience, our interfaces with them on a regular basis to enrich the experiences of their customers. And we believe we do that better than anybody else.” The Q3 10-Q filing echoed this narrative, stating product development focused on improved performance, convenience, and market value.

However, the FDA’s March 2025 Warning Letter disclosed that DexCom “modified the G6 and G7 sensors” without prior regulatory approval, causing "larger inaccuracies" and heightened risks for insulin-dependent users.

Hunterbrook Media’s September 2025 investigation titled Dexcom’s Fatal Flaw exposed further details through FOIA documents, ex-employee accounts, and patient death reports directly linked to these unauthorized changes. One former engineer cautioned management about membrane materials diminishing accuracy by up to 20% under certain conditions, but management proceeded to ship the devices regardless. This contrast between public optimism and private alarm underpins the lawsuit’s core.

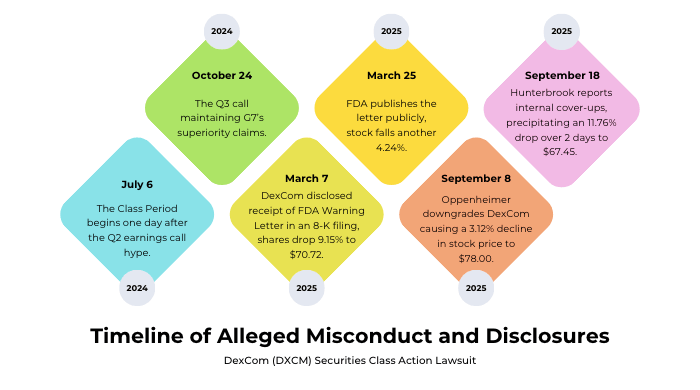

Timeline of Alleged Misconduct and Disclosures

Class Period: July 26, 2024 – September 17, 2025, inclusive.

The alleged deception spanned systematic misrepresentations until the truth surfaced: on July 26, 2024, the Class Period began one day after the Q2 earnings call hype; October 24, 2024, saw a Q3 call maintaining G7’s superiority claims.

- On July 25, 2024, DexCom hosted a Q2 earnings call where management touted purported enhancements to the G7 and the ramping up of manufacturing facilities, and filed the Q2 2024 10-Q.

- On October 24, 2024, DexCom hosted a Q3 earnings call and filed the Q3 2024 10-Q, with management continuing to tout G7's "accuracy" and "higher quality".

- On February 13, 2025, DexCom hosted a conference call to discuss its Q4 and FY 2024 results, where management stated the G7 was the "most accurate sensor available" and promised continued enhancements to its accuracy and reliability.

- On March 7, 2025, DexCom quietly disclosed receipt of the FDA Warning Letter in an 8-K filing, causing shares to drop 9.15% to $70.72. When the FDA published the letter publicly on March 25, 2025, the stock fell another 4.24%.

- On September 8, 2025, Oppenheimer downgraded DexCom to "perform," citing field checks revealing G7 sensor failures, causing a 3.12% decline in stock price to $78.00. The September 18, 2025, Hunterbrook report titled "Dexcom’s Fatal Flaws" detailed hospitalizations, deaths, and internal cover-ups, precipitating an 11.76% drop over two days to $67.45.

Each disclosure peeled back layers of manufacturing issues, unauthorized modifications, and patient harm, from which the stock has yet to recover.

Investor Harm and Market Reaction

The cumulative financial damage is stark: from a peak near $100 per share, prices fell below $70. The four major disclosures erased approximately $12 billion in market capitalization. Insider sales exacerbated the impact, with Sayer selling 65,857 shares for about $5.19 million, Sylvain offloading 30,905 shares for approximately $2.27 million, and Leach selling 18,200 shares for nearly $1.33 million, all allegedly privy to concealed truths. Short interest surged after the Hunterbrook revelations, and options implied volatility reached levels not seen since the COVID-19 pandemic onset. Shareholders face significant capital loss risks unless a meaningful settlement is achieved.

Litigation and Procedural Posture

The complaint alleges violations of Section 10(b) and Rule 10b-5 (false statements and omissions) and Section 20(a) (control person liability), with scienter supported by operational centrality of G7, timing of insider sales, and disclosures of FDA findings. Plaintiffs rely on FDA documents and FOIA-obtained internal records.

The lead plaintiff deadline is December 26, 2025. Discovery may reveal internal communications, validation reports, and investigations into adverse patient outcomes.

Shareholder Sentiment

The diabetes community vocalized outrage prior to litigation. On social media platforms like X (formerly Twitter), accounts publicly condemned DexCom for secretly altering devices essential for survival, citing FDA statements on component changes that reduced accuracy. This sparked viral engagement with tens of thousands of likes.

Reddit’s r/dexcom forum became a hub for anguished posts reporting personal losses and calls to divest from DexCom stock. Stocktwits sentiment flipped abruptly from optimism to skepticism following Hunterbrook’s disclosures, with ex-DexCom engineers alleging management’s knowledge of membrane changes since Q3 2024, prioritizing profits over users' lives.

Analyst Commentary

Analyst consensus and price-target averages fell materially after the disclosures; public analyst-consensus pages (Yahoo!Finance) show multiple price-target cuts and mixed buy/hold coverage. After the disclosures, several firms cut price targets and issued downgrades or more cautious notes, indicating reduced analyst bullishness.

The September Oppenheimer downgrade for DexCom cited field checks that raised concerns about G7 accuracy/performance. Hunterbrook’s report deepened the sell-off. Independent analysts and outlets described the regulatory and product-quality risks as capable of materially altering DexCom’s outlook; several firms like Oppenheimer and Argus either cut price targets or issued more cautious notes. Patient and investor trust was gone.

SEC Filings & Risk Factors

In its Q2 2024 and Q3 2024 Form 10-Q filings, Dexcom incorporated risk-factor disclosures referencing the necessity of regulatory reviews and the possibility of product-performance issues. For example, the Q3 2024 10-Q stated that there were “no material changes” to the risk factors disclosed in the 2023 10-K.

In the Form 8-K filed shortly after the March 2025 FDA Warning Letter, the company disclosed receipt of the Warning Letter and referred to “non-conformities in manufacturing processes and quality management systems” — but did not publicly describe unapproved

Publicly-filed class-action complaints assert that the quarterly reports included SOX certifications by CEO Kevin Sayer and CFO Jereme Sylvain, but that the disclosures did not call attention to the alleged unauthorized changes to the G7 sensor.

Conclusion: Implications for Investors

The DexCom case underscores the dangers of “move fast and break things” philosophy in medtech. When the product sustains life, unvalidated cost-cutting creates severe risks to patients rather than innovation breakthroughs.

Investors who missed FDA Warning Letters and related regulatory signals did so at their peril. The case is a powerful reminder to scrutinize FDA 483s, warning letters, and FOIA records in due diligence. For competitors Abbott, Medtronic, and Senseonics, this scandal signals heightened regulatory scrutiny and patient advocacy.

The G7 controversy may depress DexCom's market valuation for years, turning a former growth favorite into a cautionary tale.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Synopsys, Inc. (SNPS) Securities Class Action Lawsuit Update [November 11, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/snps-alert-plus-banner-image-v2.png)

![CarMax, Inc. (KMX) Securities Class Action Update [November 12, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/kmx-update-banner-v2.webp)

![Molina Healthcare, Inc. (MOH) Securities Class Action Update [November 19, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/moh-banner-image.webp)