![Blue Owl Capital Inc. (OWL) Securities Class Action Lawsuit Filed [December 9, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/owl-new-case-banner-1.webp)

Introduction to Blue Owl Capital Inc. (OWL) Securities Class Action Lawsuit

A securities fraud class action has been filed against Blue Owl Capital Inc. (NYSE: OWL), in the United States District Court for the Southern District of New York, covering investors who acquired securities between February 6, 2025 and November 16, 2025. Investors allege the company told the market that redemptions were not pressuring its asset base at its business development companies and that liquidity was sufficient, while also touting a healthy credit portfolio with no meaningful stress. The complaint says the truth surfaced through a series of corrective disclosures as earnings missed expectations, a merger announcement effectively blocked redemptions at a key vehicle, and reporting revealed investor withdrawals and potential losses for certain investors. As these events unfolded between October 30 and November 16, 2025, Blue Owl's NYSE: OWL stock fell sharply on heavy trading. Investors claim they suffered significant losses when the market learned facts that contradicted the company's earlier statements, and assert claims under Sections 10(b) and 20(a) of the Securities Exchange Act of 1934 and Rule 10b-5.

Blue Owl Capital Inc. (OWL) Securities Lawsuit Case Details

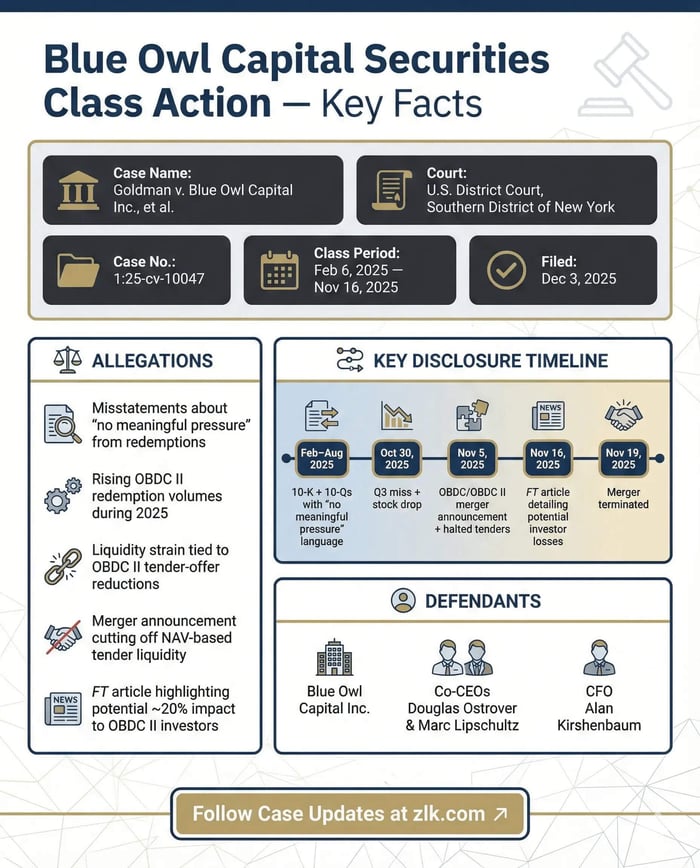

Case Name: Goldman v. Blue Owl Capital Inc. et al.

Case No.: 1:25-cv-10047

Jurisdiction: U.S. District Court, Southern District of New York

Filed on: December 3, 2025

Blue Owl Capital Inc. (OWL) Company Profile

Blue Owl is an asset management firm specializing in alternative investment solutions, primarily private credit (direct lending), with platforms in Credit, GP Strategic Capital, and Real Assets, that manages business development companies and other alternative investment vehicles, and is publicly traded on the NYSE. As of fiscal 2024, it reported over $251 billion in assets under management, with 40% tied to its Direct Lending business, reflecting its focus on private credit across business development companies.

Blue Owl Capital Inc. (OWL) Securities Lawsuit Class Period

February 6, 2025-November 16, 2025, inclusive.

All persons and entities that purchased or otherwise acquired Blue Owl securities between February 6, 2025 and November 16, 2025, inclusive, including common stock traded on NYSE: OWL. All such investors may be eligible to join the Blue Owl Capital Inc. (OWL) class action lawsuit.

Allegations in the Blue Owl Capital Inc. (OWL) Securities Class Action Lawsuit

The lawsuit targets Blue Owl Capital Inc. and executives Douglas I. Ostrover (Co-Chief Executive Officer), Marc S. Lipschultz (Co-Chief Executive Officer), and Alan Kirshenbaum (Chief Financial Officer). According to the complaint, under the federal securities laws, they told investors during the class period that redemptions were not meaningfully pressuring the company's asset base and that liquidity was sufficient, while promoting the strength of the credit portfolio.

On February 21, 2025, in its FY 2024 Form 10-K, Blue Owl stated that 91% of GAAP and FRE management fees came from Permanent Capital and the rest predominantly from long-dated capital, "with no meaningful pressure to our asset base from redemptions" at its business development companies. The same filing asserted that based on management's experience, current liquidity and fee cash flows would be sufficient to meet anticipated working capital needs for at least the next 12 months.

The company repeated this theme through 2025 in its financial results. On May 5, 2025, the Q1 10-Q said approximately 88% and 89% of GAAP and FRE management fees were from Permanent Capital, again with "no meaningful pressure on our asset base from redemptions." On August 1, 2025, the Q2 10-Q reported roughly 86% and 87% of GAAP and FRE fees from Permanent Capital and repeated there was "no meaningful pressure on our asset base from redemptions."

As the year progressed, executives continued to emphasize portfolio health. On October 30, 2025, during an earnings call, Co-CEO Marc S. Lipschultz said the credit portfolio's health "remains excellent" with no signs of meaningful stress. The complaint alleges that, in reality, Blue Owl was experiencing meaningful pressure from BDC redemptions, faced liquidity-related undisclosed issues, and was likely to limit or halt redemptions at certain BDCs, including OBDC and OBDC II, rendering the company's positive statements materially misleading under Rule 10b-5 or lacking a reasonable basis.

The Truth Emerges

The picture began to change on October 30, 2025, when Blue Owl reported third-quarter results, a corrective disclosure, that missed expectations. The company disclosed fee-related earnings of $376.2 million that missed consensus estimates, fee-related earnings margins of 57.1% that missed expectations by roughly 20 basis points, and performance revenue that fell 33% year over year to $188,000. Management characterized some of the impact as "short-term noise" tied to mark-to-market on swaps around debt.

Days later, on November 5, 2025, Blue Owl's listed BDC, OBDC, and OBDC II announced a merger agreement that revealed OBDC II did not anticipate conducting additional quarterly tender offers prior to closing, effectively blocking redemptions and signaling a tender offer suspension. The narrative culminated on November 16, 2025, when the Financial Times reported that OBDC II investors would be blocked from redemptions until the merger completed and could face a reduction in investment value (a NAV discount of approximately 20%). The article also disclosed that investors had pulled $150 million from OBDC II through the first nine months of 2025, a 20% increase from the prior year (i.e., redemptions), and quoted OBDC's CFO Jonathan Lamm acknowledging that if shareholders voted down the deal, OBDC II might be forced to limit redemptions (a potential tender offer suspension) and that investors could take a haircut. These revelations cut against earlier assurances of sufficient liquidity that the company had cited to describe a lack of pressure on its asset base.

Market Reaction

The market reacted swiftly to each disclosure. On October 30, 2025, after results were released before the market opened, Blue Owl's share price fell $0.70, or 4.23%, to close at $15.86 on unusually heavy trading volume. Following the after-hours merger announcement on November 5, 2025, the stock declined the next day, November 6, 2025, by $0.74, or 4.72%, to close at $14.95, again on heavy volume on this corrective disclosure. After the November 16, 2025 Financial Times article, shares fell on November 17, 2025 by $0.85, or 5.8%, to close at $13.77, with unusually heavy trading (approximately 4-6% declines on disclosure dates).

Next Steps

Submissions for lead plaintiff are due: February 2, 2026.

The Court will issue its order for lead plaintiff and counsel in the weeks after submissions are due.

The Court will then consider motion for class certification.

The Court will later consider a Motion to Dismiss.

To learn if you are eligible for recovery under the OWL securities class action lawsuit, visit the case submission page here.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Sprouts Farmers Market, Inc. (SFM) Securities Class Action Lawsuit Filed [December 1, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/sfm-new-case-banner-image.png)

![DeFi Technologies Inc. (DEFT) Securities Class Action Lawsuit Filed [December 5, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/deft-new-case-alert-banner-image.webp)

![Bitdeer Technologies Group (BTDR) Securities Class Action Lawsuit Filed [December 5, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/btdr-new-case-banner.webp)