When people glance at a company’s financials, they usually stop at the income statement or the balance sheet. Those are the stars of the show—the headlines, the glossy numbers that seem to say everything. But there’s another document, one that sits a little quieter, that often tells the truth better than any press release: the statement of cash flows. It doesn’t care about accruals or accounting magic. It asks the simple question: where did the money actually come from, and where did it go?

For investors, that question matters more than almost anything else. A business can report profit all day long, but if cash isn’t coming in, the whole structure eventually caves. And when you start to pay attention to this statement, you begin to see patterns others miss.

How Does a Statement of Cash Flow Track Money?

The statement of cash flows divides itself into three paths. One traces the company’s ordinary work—selling products, paying wages, collecting from customers, keeping the lights on. Another follows the longer bets: buying equipment, acquiring another company, or selling off a piece of the business. And the last shows how the company funds itself—raising debt, issuing stock, paying dividends, repurchasing shares.

Those sections aren’t filler. They tell you if a company is sustaining itself or just keeping up appearances. Net income might look fine, but if operating cash flow is negative quarter after quarter, you have to wonder how long the façade can hold.

What Happens to Companies Who Manipulate their Statements?

What Happens to Companies Who Manipulate their Statements?

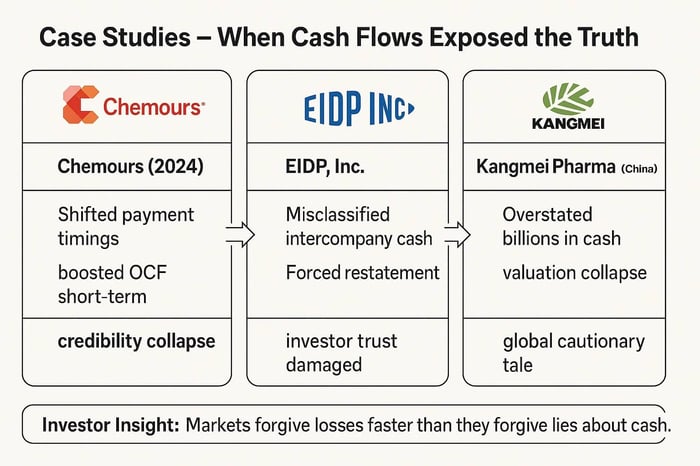

This isn’t just theory. Courts and regulators have had to deal with cash flow statements that didn’t line up with reality. In 2024, Chemours faced scrutiny over allegations that management adjusted the timing of payments and collections in ways that boosted reported operating cash flow. On paper, the company looked stronger than it really was. When those tactics came to light, investor trust evaporated. Shares fell, and the company was forced to defend itself against claims that it misled the market.

In recent years, companies have had to restate financials after misclassifying cash from intercompany loans. Something similar happened this year with EIDP, Inc., which had to restate its financials after misclassifying cash from said intercompany loans. The restatement wasn’t just an embarrassing correction—it was a reminder that when the lines between operating, investing, and financing blur, investors lose the ability to judge the health of the business. Restatements like that often trigger scrutiny from the SEC, and they almost always hurt credibility.

Even abroad, the lesson has been sharp. Kangmei Pharmaceutical in China overstated its cash holdings by staggering amounts. When regulators untangled the numbers, billions of value vanished, and investors were left holding shares built on fiction. Different market, different laws, same underlying truth: when cash flows are misrepresented, it’s investors who pay.

These cases show how misclassified or manipulated cash flows can mislead the market — and why the SEC treats cash flow accuracy as a priority in financial reporting enforcement.

Are Statements of Cash Flow Required?

American law makes the statement of cash flows a required part of the story. Since the 1980s, accounting standards have demanded it, and the SEC enforces that requirement through the reporting rules of the Securities Exchange Act. The logic is simple: cash is not just an accounting entry. It is survival. Misclassifying it or hiding it distorts the market’s ability to judge a company’s future, and that distortion can become securities fraud if investors are misled.

In recent years, the SEC’s accountants have called out cash flow classification errors as a leading cause of restatements. It’s not just an obscure technicality. If a company moves transactions around—classifying something as “financing” instead of “operating,” or pushing payments between periods—it can make the core business look healthier than it is. For investors trying to decide whether to buy or sell, those distinctions matter.

Why Should Investors Care?

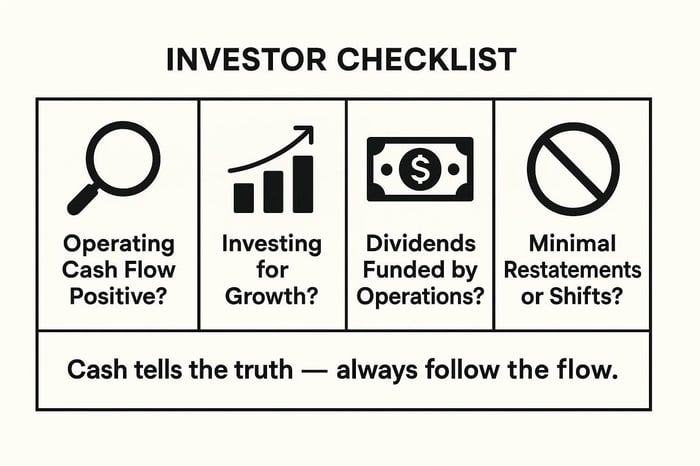

Imagine two companies. Both show the same revenue, both report the same net income. One has steady, positive operating cash flow—money coming in from customers, covering costs, leaving enough to reinvest. The other posts negative cash from operations every quarter, plugging the gap by borrowing more debt. On the surface, the earnings look identical. But in reality, only one of those companies is standing on solid ground.

That’s the kind of difference the statement of cash flows reveals. It also gives you hints about sustainability. A company may boast of generous dividends or flashy share repurchases. But if the financing section shows they’re funding those moves by piling on debt, you know to be cautious. The market can ignore that tension for a while, but eventually reality asserts itself.

For growth companies, the cash flow story can cut the other way. They may look unprofitable on paper but still show improving cash generation as they scale. Investors who understand that distinction can separate companies burning cash with no end in sight from those that are steadily building a path to stability.

Lessons Learned

The thread tying these stories together is that cash tells the truth—or at least comes closer to it than net income ever will. Misclassifications, manipulations, or omissions around cash flows almost always end badly. Investors get blindsided, regulators step in, courts have to sort through the rubble.

The companies that survive and thrive are the ones whose cash flows line up with their narratives. Growth backed by cash generation is real growth. Dividends backed by strong operations are real returns. Everything else is a short game.

Disclaimer: Attorney Advertising. Past results do not guarantee future outcomes.

You Can Also Read... |

FAQs

Must a public company file a statement of cash flows?

Yes. U.S. public companies are required to include a statement of cash flows in their SEC filings. It is part of the standard package of financial statements, alongside the balance sheet and income statement.

How does a statement of cash flows differ from a balance sheet?

The balance sheet is a snapshot in time, showing what the company owns and owes on a given date. The statement of cash flows is a motion picture. It shows how money moved during the period—what came in, what went out, and why.

What is Operating Cash Flow and how is it different from revenue?

Revenue is the total amount a company books from selling goods or services. Operating cash flow measures the actual cash collected and spent in those operations. A company can report high revenue but still have weak operating cash flow if customers haven’t paid or if expenses absorb the income.

What are financing activities and how do they differ from liabilities?

Financing activities describe the flow of cash related to raising and returning capital—issuing stock, paying dividends, repurchasing shares, borrowing or repaying debt. Liabilities, by contrast, are the company’s outstanding obligations recorded on the balance sheet at a point in time. One shows movement; the other shows position.

![Flywire Corporation (FLYW) Securities Class Action Lawsuit Update [September 15, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/flywire-securities-lawsuit-blog-banner.webp)