![CarMax, Inc. (KMX) Securities Class Action Update [November 12, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/kmx-update-banner-v2.webp)

CarMax Accused of Masking Tariff-Driven Sales as Sustainable Growth

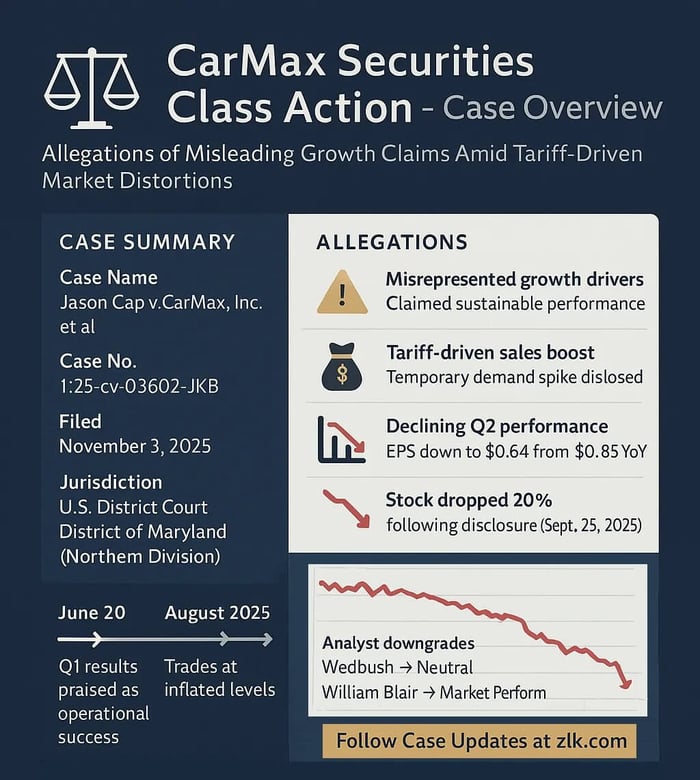

Case Name: Cap v. CarMax, Inc., et al.

Case No.: 1:25-cv-03602-JKB

Jurisdiction: U.S. District Court, District of Maryland

Filed on: November 3, 2025

Class Period: June 20, 2025–September 24, 2025

Introduction

CarMax promised a seamless ride for investors. What it delivered, according to plaintiff Jason Cap, was a detour into inflated earnings, misleading growth forecasts, and temporary market illusions. Filed in the U.S. District Court for the District of Maryland (Case No. 1:25-cv-03602-JKB), the class action alleges that CarMax, along with CEO William D. Nash and CFO Enrique N. Mayor-Mora, misrepresented the company’s financial health between June 20, 2025, and September 24, 2025, leading to a precipitous stock drop.

Investors contend that CarMax overstated long-term growth, attributing short-term gains to operational prowess rather than tariff-driven consumer buying. When reality set in, the company’s second-quarter disclosure on September 25, 2025, revealed declining retail and wholesale unit sales and net earnings per share falling to $0.64 from $0.85 year-over-year. CarMax’s stock plummeted 20% in one day, a shockwave felt across the NYSE. For fund managers and class action counsel, this case raises questions about internal controls, executive responsibility, and the market’s reliance on public statements.

Backdrop and Business Context

CarMax, headquartered in Richmond, Virginia, bills itself as the nation’s largest used car retailer, a brand built on scale, digital integration, and an omnichannel approach. Publicly traded on the NYSE under KMX, CarMax has historically relied on steady retail comps and operational efficiency to drive investor confidence.

Leading up to the alleged misconduct, CarMax reported multiple quarters of growth, highlighting its “best-in-class” omni-channel experience. Its leadership, Nash and Mayor-Mora, emphasized operational leverage and efficiency in both press releases and earnings calls. However, behind the polished statements, temporary market factors—most notably tariff speculation influencing consumer purchases—may have skewed results. The class action claims that this nuance was never fully disclosed to investors, painting a rosier picture than reality warranted.

Promises Made vs. Reality

In a June 20, 2025 press release, CarMax touted:

“We delivered our fourth consecutive quarter of positive retail comps and double-digit year-over-year earnings per share growth [...] This positions us to continue to drive sales, gain market share, and deliver significant year-over-year earnings growth for years to come.”

On the Q1 2026 earnings call, Nash expanded on this optimism:

“[W]e feel really good […] this quarter's performance, it's driven some by the macro factors, but I also think it's driven some by with what we have can control […] the quarter started off strong and then we saw an uptick at the end of the quarter when there was speculation about the tariffs […] But I would just go back to even before we saw that the initial uptick, the business was growing -- was doing well […] this performance is both part market driven. I think it’s also driven by us […] We would expect to grow sales and gain share this year, and nothing has changed that outlook.”

According to the complaint, these statements were materially misleading. Defendants allegedly failed to disclose that Q1 gains were largely a short-term lift from tariff speculation, not a durable uptick in consumer demand. By the second quarter, sales dropped, inventory depreciation eroded pricing competitiveness, and net earnings per share fell sharply. Investors were blindsided; the promise of sustained growth dissolved into an abrupt correction.

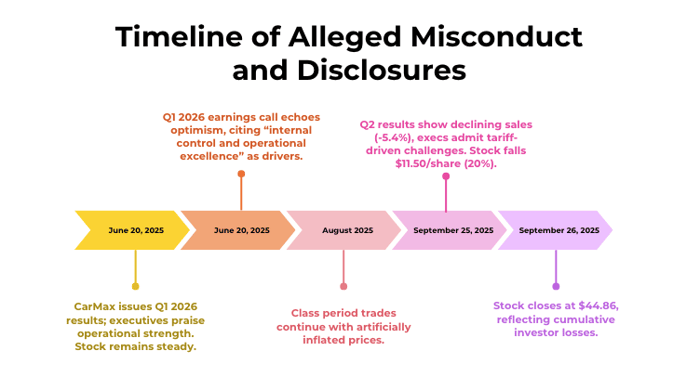

Timeline of Alleged Misconduct and Disclosures

Class Period: June 20, 2025 – September 24, 2025, inclusive.

- June 20, 2025: CarMax issues Q1 2026 results; executives praise operational strength. Stock remains steady.

- June 20, 2025: Q1 2026 earnings call echoes optimism, citing “internal control and operational excellence” as drivers.

- August 2025: Class period trades continue with artificially inflated prices.

- September 25, 2025: CarMax releases Q2 results, showing declining retail unit sales (-5.4%), net EPS drop to $0.64, and executives acknowledge challenges due to tariff-driven consumer behavior. Stock falls $11.50/share (20%).

- September 26, 2025: Continued market reaction; stock closes at $44.86, reflecting cumulative investor losses.

The sequence underscores a pattern alleged in the complaint: short-term gains misattributed to operational skill, followed by a corrective disclosure that triggered a market shock.

Investor Harm and Market Reaction

Investors who purchased CarMax shares at artificially inflated prices reportedly suffered significant damages. According to Schedule A attached to the complaint, lead plaintiff Jason Cap transacted multiple times during the class period, purchasing at $58.15 and $57.99 per share and later selling below or after sharp declines. The market’s immediate response—a 20% single-day drop—illustrates the tangible financial harm alleged.

Analyst downgrades followed the second-quarter disclosure. Multiple brokerage reports highlighted misalignment between CarMax’s stated growth drivers and the actual influence of macro factors like tariff speculation. Institutional investors reportedly re-evaluated exposure, compounding sell-offs.

Litigation and Procedural Posture

The complaint asserts claims under Section 10(b) and Rule 10b-5 for alleged misrepresentations and omissions, and Section 20(a) against the individual defendants as controlling persons. Scienter hinges on executive knowledge or reckless disregard for the misleading nature of public statements. No confidential witnesses cited, but the complaint references internal knowledge and operational awareness inconsistent with public statements.

No trial date has been set. Plaintiff seeks monetary damages, and costs, with the market relying on judicial interpretation of loss causation and reliance principles.

Shareholder Sentiment

Investor sentiment, as observed on X (formerly Twitter), Reddit, and Stocktwits, shifted dramatically post-disclosure. Prior to September 25, 2025, optimism pervaded threads, with users citing operational excellence and positive comps. After the Q2 release, discussions turned to the earnings miss and its implications for the used car market.

On Stocktwits, retail sentiment remained "extremely bullish" as of September 26, 2025, with users viewing the drop as a buying opportunity despite the miss: "At $45 seems like quite the steal. They are profitable and prints cash, have a fortress of a balance sheet." Message volume spiked to "extremely high" levels, reflecting heightened engagement.

On X, posts highlighted the stock's plunge and tariff effects, with users noting the breach of the 52-week low and bearish implications for peers like Carvana ($CVNA), reiterating a $37 price target: "There is absolutely no chance that Carvana $CVNA is thriving in the current environment given the deterioration in used car reselling market." Another user tied the weakness to broader economic signals: "the weakness in the used car market is a true reflection of consumer sentiment, it's a leading indicator of recession." Volume spikes and negative commentary indicate a rapid erosion of trust, aligning with the market’s reaction.

On Reddit's r/ValueInvesting, pre-earnings threads (e.g., August 2025) showed cautious optimism about used car sales strength, but post-Q2 discussions in r/carmax lamented the stock's 52-week low compared to Carvana's highs, with users attributing it to affordability and credit squeezes: "CarMax is a cyclical, profitable scale retailer getting squeezed by affordability/credit and trading at trough sentiment."

Analyst Commentary

Analyst reports highlighted divergence between CarMax’s statements and market reality. Prior to Q2 disclosure, target prices ranged from $60–$65, reflecting confidence in operational leverage. Post-disclosure, reactions focused on the earnings miss, tariff pull-forward effects, and structural challenges.

- Wedbush Securities downgraded KMX to Neutral post-earnings, citing weak results across key metrics and concerns over sustaining market leadership amid softening demand. They noted potential revisions to estimates, with shares down 46% YTD as of September 25, 2025.

- William Blair downgraded to Market Perform on November 6, 2025, warning of negative comparable sales for at least six months through May 2026, putting "material pressure on profits." They highlighted a "disconnect" between CarMax’s performance and the broader used car market, compounded by CEO Nash's impending departure.

- Truist cut its price target post-Q2 miss, expressing doubts on CarMax's ability to drive growth, though 11 of 19 analysts still held Buy or higher ratings with an average target of $72.87 as of September 26, 2025.

Analysts flagged potential risk for investors relying solely on executive narratives, reinforcing litigation claims regarding material misstatements. Consensus FY2026 EPS estimates were reduced by 15-20% in the weeks following.

SEC Filings & Risk Factors

CarMax’s 10-Q for Q2 FY2026 acknowledged general market risks but omitted any direct reference to tariff speculation inflating short-term sales. Press releases and earnings calls emphasized operational execution rather than market contingencies. The lawsuit highlights these omissions as central to claims under federal securities laws, suggesting that management disclosures did not fully capture material risks affecting shareholder value.

Conclusion: Implications for Investors

The CarMax case underscores a perennial lesson: investor reliance on executive guidance carries risk, especially when macro factors masquerade as operational triumphs. For fund managers and class action counsel, the lawsuit emphasizes the importance of scrutinizing earnings drivers, inventory management, and management commentary. As the litigation unfolds, investors are watching closely—not just for potential recoveries, but for signals about corporate transparency and the limits of bullish executive narratives in shaping market expectations.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Molina Healthcare, Inc. (MOH) Securities Class Action Update [November 19, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/moh-banner-image.webp)

![DexCom, Inc. (DXCM) Securities Class Action Lawsuit Update [November 11, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/dxcm-alert-plus-banner.webp)

![Telix Pharmaceuticals Ltd. (TLX) Securities Class Action Update [November 21, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/tlx-alert-plus-banner-image.png)