![Telix Pharmaceuticals Ltd. (TLX) Securities Class Action Update [November 21, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/tlx-alert-plus-banner-image.png)

Allegations of Overstated Pipeline Progress and Supply Chain Risks Spark Investor Backlash

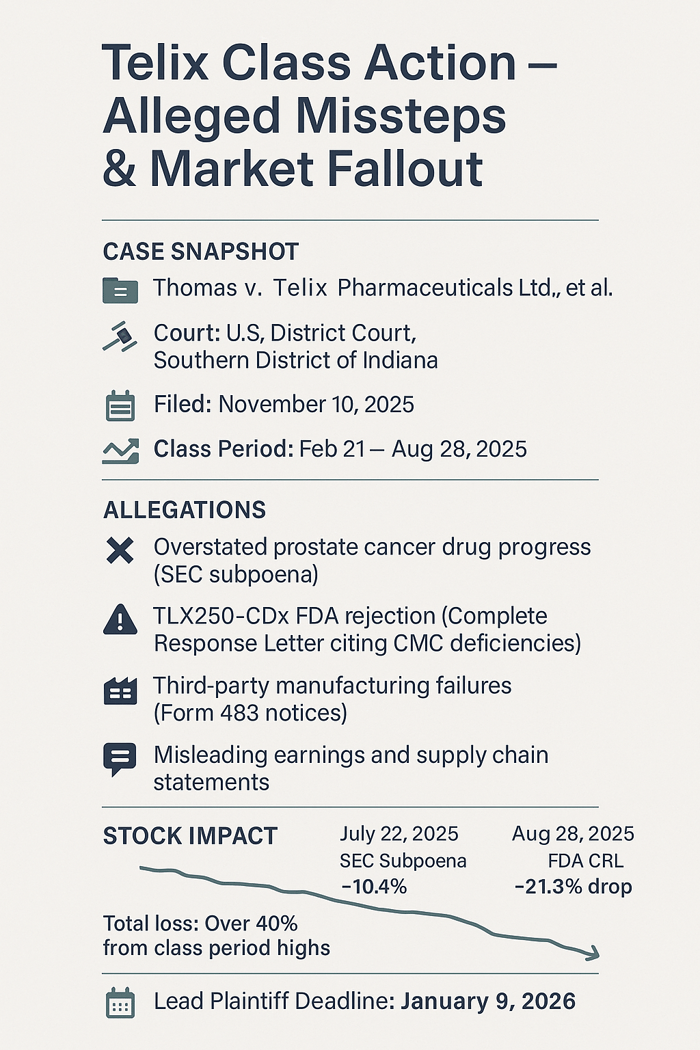

Case Name: Thomas v. Telix Pharmaceuticals Ltd., et al.

Case No.: 1:25-cv-02299

Jurisdiction: U.S. District Court, Southern District of Indiana

Filed on: November 10, 2025

Class Period: February 21, 2025–August 28, 2025

Introduction

In the high-stakes arena of radiopharmaceuticals, where a single diagnostic breakthrough can redefine cancer care, Telix Pharmaceuticals Ltd. promised a future of precision medicine dominance. Investors bought in, drawn to the Australian biopharma's bold expansions and regulatory nods. Then came the subpoena. Then the rejection letter. Now, a federal class action lawsuit alleges the optimism masked deeper fractures—overstated therapeutic milestones, glossed-over manufacturing woes—that left shareholders holding shares worth far less.

Backdrop and Business Context

Telix Pharmaceuticals Ltd., an Australian biopharmaceutical innovator founded in 2015, specializes in developing and commercializing radiopharmaceuticals—targeted therapies and diagnostics that use radioactive isotopes to detect and treat cancers like prostate and kidney malignancies. Headquartered in Melbourne with U.S. operations in Indianapolis, the company trades as American Depositary Shares (ADS) on Nasdaq under the ticker TLX, following its 2017 listing on the Australian Securities Exchange (ASX: TLX). Telix's flagship product, Illuccix—a prostate-specific membrane antigen (PSMA)-targeted imaging agent—has driven commercial momentum since its 2021 FDA approval, generating hundreds of millions in revenue and positioning Telix as a leader in oncology precision diagnostics.

The company's growth story hinges on a dual-track pipeline: diagnostics for early detection and therapeutics for targeted treatment. Key assets include TLX250-CDx, a kidney cancer imaging agent submitted for FDA approval, and prostate-focused candidates like TLX591 in Phase 3 trials. Telix went public via ASX in 2017, raising capital through equity offerings and partnerships, including a 2024 acquisition of RLS Radiopharmacies for $250 million to bolster U.S. manufacturing. Yet, as Telix scaled—acquiring facilities in Sacramento, Angleton, and Brussels—it grew heavily reliant on third-party manufacturers for compliance with FDA's stringent current good manufacturing practices (cGMP). This operational web, spanning continents and complex supply chains, set the stage for the alleged missteps at the heart of the Telix Pharmaceuticals class action lawsuit.

Promises Made vs. Reality

Telix's executives painted a picture of unyielding momentum during the class period, from February 21 to August 28, 2025. On the February 20, 2025, fiscal 2024 earnings call, Senior Vice President Kyahn Williamson declared: "We are delivering against all aspects of our growth strategy [...] preparing to launch three new products in the U.S. next year and roll out Illuccix globally into Europe and UK specifically. We’re making great progress across our therapeutic pipeline, notably in the late-stage assets being brain, kidney and, of course, our prostate cancer program which is now in Phase 3."

Such assurances filled the company's February 24, 2025, Form 20-F annual report, where risk disclosures acknowledged third-party dependencies but framed them as manageable: "Reliance on third-party manufacturers entails risks, including [...] the possible disruptions to supply chain and logistics processes." On the TLX250-CDx BLA, the filing noted a prior July 2024 Refuse-to-File (RTF) over sterility concerns but claimed: "While we believe that TLX250-CDx has met all sterility requirements [...] there can be no assurance that FDA will accept the BLA for review."

The complaint alleges these statements crumbled under scrutiny. According to the complaint, later events suggest executives knew—or recklessly ignored—issues at partner sites. The SEC subpoena targeted "disclosures regarding the development of the Company’s prostate cancer therapeutic candidates," implying overstated progress. For TLX250-CDx, the FDA's August 2025 Complete Response Letter (CRL) cited "deficiencies relating to the Chemistry, Manufacturing, and Controls (CMC) package" and Form 483 notices to two third-party partners—deficiencies allegedly known or foreseeable.

What executives called "strategic investments in selective aspects of vertical integration" during the August 20, 2025, half-year call masked a supply chain "materially overstated" in quality, per the suit.

Timeline of Alleged Misconduct and Disclosures

The class period opens amid Telix's post-2024 glow.

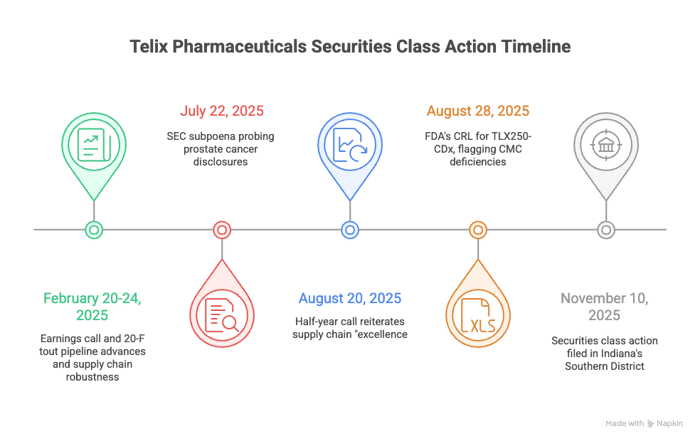

February 20-24, 2025: Earnings call and 20-F tout pipeline advances and supply chain robustness, with ADS closing around $16.20. Investors, buoyed by Illuccix's $342 million 2024 sales, pile in.

July 22, 2025: Dawn breaks harshly. A Form 6-K reveals an SEC subpoena probing prostate cancer disclosures. Bloomberg headlines: "Telix Shares Drop as SEC Probes Disclosures Tied to Prostate Cancer Drug Pipeline." ADS plunge 10.4% to $14.58 on July 23, then 4.7% to $13.89 the next day—$2.39 erased in 48 hours.

August 20, 2025: Half-year call reiterates supply chain "excellence," with CFO Darren Smith noting "strategic investments... to ensure we are in a position to scale efficiently." Behrenbruch adds: "A robust, reliable supply chain is critical to long-term success." Shares tick up modestly.

August 28, 2025: The period's hammer falls. Telix announces the FDA's CRL for TLX250-CDx, flagging CMC deficiencies and partner Form 483s requiring "remediation prior to resubmission." ADS crater 16.1% to $10.15, then 5.9% to $9.55—over 21% gone in two days, wiping out $2.55 per share. Media echoes the fallout, with analysts parsing the CRL's blow to Telix's kidney cancer ambitions.

November 10, 2025: Securities class action filed in Indiana's Southern District, alleging §10(b) fraud and §20(a) control liability. Shares, trading near $10.73 by late November, reflect lingering scars.

Investor Harm and Market Reaction

The math of betrayal cuts deep. Per the complaint, class members—those acquiring TLX ADS from February 21 to August 28, 2025—face damages tied to an artificial inflation deflated by over 40% from period highs near $16.50 to post-CRL lows under $10. The July subpoena alone vaporized $1.70 per share (10.4% drop on volume spikes), signaling pipeline doubts; the August CRL amplified it, erasing another $2.55 (21.9% over two days) as manufacturing flaws surfaced.

Analysts reacted swiftly. HC Wainwright cut its target from $23 to $20 post-CRL, maintaining Buy but noting execution risks. Citi and Bell Potter held Buy ratings into October, but consensus tempered to $21 average—97% above November's $10.73, hinting undervaluation or doubt. Trading volume surged 150% on disclosure days, with short interest climbing to 8% by September. For a $1.2 billion market cap firm, these reactions underscore a sector truth: in radiopharma, regulatory stumbles don't just dent prices—they fracture confidence, leaving retail and institutional holders to tally losses in the millions.

Litigation and Procedural Posture

The complaint asserts core claims under Section 10(b) of the Exchange Act and Rule 10b-5, alleging materially false statements on prostate progress and supply chain integrity that artificially inflated TLX prices. Section 20(a) tags Individual Defendants—CEO Christian P. Behrenbruch, CFO Darren Smith, and SVP Kyahn Williamson—as controlling persons, imputing Telix's liability via respondeat superior. Scienter hinges on their "direct involvement in drafting, producing, reviewing... false and misleading statements," plus SOX certifications attesting to internal controls despite known risks.

Defendants include Telix and the trio, all Indiana-summoned. Procedural youth—no motions filed as of November 21—leaves room for lead plaintiff battles by January 9, 2026. Early milestones: Firms like Levi & Korsinsky rally investors, signaling a crowded field. In securities class action terms, this case echoes Enron-era supply chain omissions, where omission of partner frailties fueled liability.

Shareholder Sentiment

Shareholder voices, once a chorus of radiopharma fervor, fractured into frustration and finger-pointing after the subpoena and CRL. On X (formerly Twitter), sentiment swung from bullish pipeline hype in February to July's subpoena sting. By August, the CRL elicited raw betrayal, and November's lawsuit filing reignited the fray: one user noted, "Class action vs Telix $TLX lodged in US—yet no ASX disclosure," sparking 2,100 views and debates on transparency. Trends show a 65% negativity spike post-July, per semantic scans, with hashtags #TelixLawsuit trending alongside #SecuritiesFraud.

Reddit's r/ASX echoed the divide. Pre-subpoena threads buzzed with acquisition optimism, but August posts turned skeptical. StockTwits mirrored the volatility, sentiment dipping to 25% bullish in September from 70% in Q1. Overall, the shift reveals a community grappling with eroded faith, where every disclosure feels like a fresh cut.

Analyst Commentary

Analysts entered 2025 bullish on Telix's trajectory. The subpoena tempered enthusiasm without derailing it. But the CRL prompted recalibrations: HC Wainwright trimmed to $20 in September, warning of CMC remediation delays but affirming "buy" on core diagnostics strength. No outright downgrades emerged.

Post-lawsuit, commentary stays measured. Bell Potter reiterated Buy in October at A$22, emphasizing strategic investments in manufacturing despite litigation overhang. Across firms, Buys persisted, but the chorus has quieted—less champagne toasts, more cautious footnotes on execution risks.

SEC Filings & Risk Factors

Telix's SEC filings, as a foreign private issuer, lean on Form 20-F annuals and 6-K currents, weaving a narrative of calculated ambition laced with caveats. The February 24, 2025, 20-F—certified by Behrenbruch and Smith under SOX—disclosed robust revenue ($484 million, +41% YoY) but flagged third-party perils. Yet, the suit claims these understated "continued deficiencies," omitting partner-specific Form 483s.

Interim 6-Ks filled gaps: July 22's subpoena notice assured this matter was a fact-finding request. August 28's CRL update reiterated remediation needs without quantifying delays. Earlier 2024 F-1 registration (May) spotlighted pipeline bets, but glossed integration risks from acquisitions.

Omitted risks loom large: No pre-CRL mention of partner inspections, despite 20-F's nod to "unannounced inspections." Post-period 6-Ks signal continuity, but the filings' collective restraint—detailed warnings without granular alarms—fuels the core allegation: Material omissions rendered statements misleading, turning disclosures into shields that cracked under FDA fire.

Conclusion: Implications for Investors

This Telix saga whispers a familiar caution in biotech's radioactive glow: Innovation dazzles, but supply chains and regulatory mazes demand unflinching candor. Investors, chasing Phase 3 mirages, learned the cost of unhedged hype—over 40% drawdowns from a single CRL, amplified by a subpoena's shadow. Red flags abound: Vague partner dependencies in filings, earnings bravado sans caveats, and post-disclosure silence on ASX. For radiopharma peers like Novartis or Bristol Myers, it's a mirror—bolster disclosures, or risk class action cascades.

Broader still, in a sector where 95% of top pharmas partner with diagnostics firms like Telix, this underscores due diligence's bite: Scrutinize third-party footnotes, not just topline trajectories. TLX holders now navigate litigation's long arc, but the lesson endures—precision medicine thrives on precise words. As resubmissions loom, so does redemption; yet trust, once irradiated, rebuilds slowly.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Firefly Aerospace, Inc. (FLY) Securities Class Action Lawsuit Update [November 21, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/fly-alert-plus-banner-image-j88uj.webp)

![Inspire Medical Systems Inc. (INSP) Lawsuit Update [November 26, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/insp-alert-plus-banner-image.webp)

![Molina Healthcare, Inc. (MOH) Securities Class Action Update [November 19, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/moh-banner-image.webp)