![Molina Healthcare, Inc. (MOH) Securities Class Action Update [November 19, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/moh-banner-image.webp)

Overly Optimistic Guidances Lead to Plummeting Stock and Significant Investor Losses

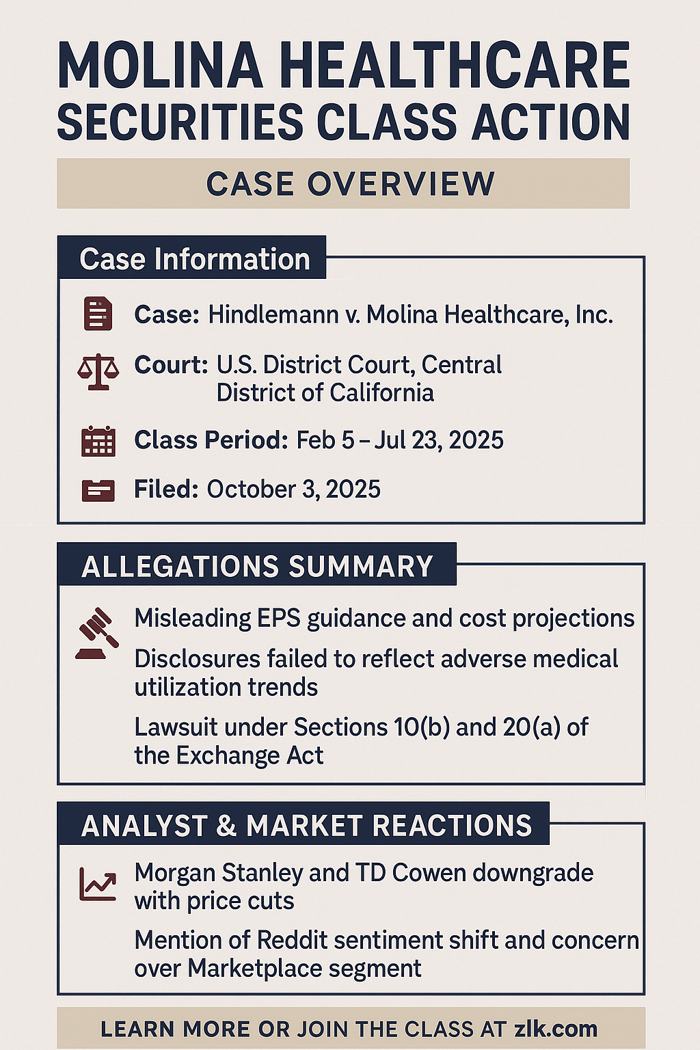

Case Name: Hindlemann v. Molina Healthcare, Inc., et al.

Case No.: 2:25-cv-09461

Jurisdiction: U.S. District Court, Central District of California

Filed on: October 3, 2025

Class Period: February 5, 2025–July 23, 2025

Introduction

Molina Healthcare, Inc. (NYSE: MOH) finds itself at the center of a federal securities class action. The lawsuit alleges that Molina misled investors about its medical cost trends and earnings projections, particularly in its Marketplace business, only to sharply revise its full‑year 2025 guidance downward. On July 24, 2025, following these disclosures, Molina’s shares fell 16.84%, signaling serious investor losses and renewed scrutiny of its financial assumptions. This case underscores the risks of premium‑cost misalignment in managed-care operations.

Backdrop and Business Context

Molina Healthcare primarily serves low-income Americans through Medicaid, Medicare, and state-based insurance exchanges (Marketplace). Its business model depends heavily on managing premium inflows against medical cost outflows. Given its exposure to government-sponsored healthcare, small miscalculations in projected medical utilization or cost trends can dramatically erode margins. At the beginning of 2025, Molina projected strong performance, but that view would soon collide with a harsher reality — namely, accelerating medical costs that outpaced its rate assumptions.

Promises Made vs. Reality

In its July 7, 2025 press release, Molina reported preliminary Q2 adjusted earnings of $5.50 per share and reset its full-year 2025 guidance to $21.50–$22.50 (down from its earlier “at least $24.50”). CEO Joseph Zubretsky acknowledged, “The short-term earnings pressure … results from what we believe to be a temporary dislocation between premium rates and medical cost trend which has recently accelerated.” What the class‑action complaint argues is that Molina’s internal assessments were less sanguine: the company allegedly failed to properly account for rising utilization across its business lines, especially behavioral health, pharmacy, and inpatient/outpatient services. Ultimately, the guidance revision called into question the integrity of its earlier rate models.

Timeline of Alleged Misconduct and Disclosures

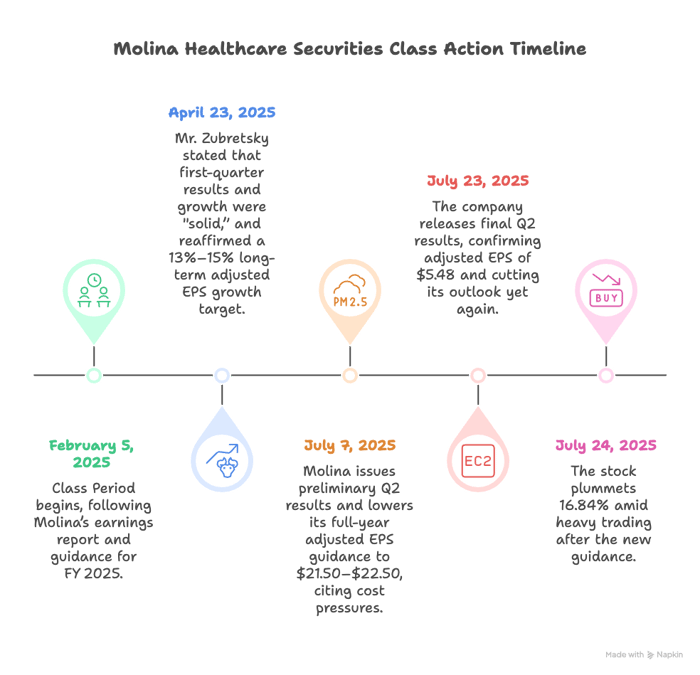

- February 5, 2025: Class Period begins, following Molina’s earnings report and guidance for FY 2025.

- April 23, 2025: Mr. Zubretsky stated that first-quarter results and growth were "solid,” and reaffirmed a 13%–15% long-term adjusted EPS growth target.

- July 7, 2025: Molina issues preliminary Q2 results and lowers its full-year adjusted EPS guidance to $21.50–$22.50, citing cost pressures.

- July 23, 2025: The company releases final Q2 results, confirming adjusted EPS of $5.48 and cutting its outlook yet again.

- July 24, 2025: The stock plummets 16.84% amid heavy trading after the new guidance.

Investor Harm and Market Reaction

The class‑action complaint alleges that investors paid inflated prices based on overly optimistic guidance. According to public filings, Molina lowered its earnings outlook twice within a month. On the day of the plunge, Molina’s negative earnings outlook triggered significant selling, validating the class’s loss causation theory. For shareholders, the drop erased a substantial portion of their investment in just days.

Litigation and Procedural Posture

The complaint invokes Section 10(b) of the Securities Exchange Act and Rule 10b-5, alleging false or misleading statements and omissions. It also brings a Section 20(a) claim against Molina’s senior executives — namely, its CEO and CFO — for their roles in controlling and disseminating the misleading guidance. Plaintiff Jeffrey Hindlemann positions himself as representative of all investors who bought shares during the Class Period and suffered damages when the truth emerged.

Shareholder Sentiment

On Reddit, sentiment turned sharply negative after the guidance cuts. Discussions in r/ValueInvesting highlighted frustration with the rapid decline, with users noting the stock was "down almost 50% in a month" despite ongoing profitability and elevated price targets, questioning whether government-dependent rate increases were adequately priced in. In r/Healthcare_Anon, investors dissected the financial mechanics of the second guidance revision, analyzing the revised $19 EPS floor and its implications for consolidated medical care ratio (MCR) and pretax margins, particularly tied to Marketplace trends and new information from the June close process. These perspectives illustrate a growing realization among retail shareholders that Molina’s prior communications may have underplayed downside risk.

Analyst Commentary

Wall Street financial analysts were quick to react. Morgan Stanley cut its rating on Molina to “Equal-Weight” and slashed its price target from $364 to $266, citing deteriorating cost assumptions. Meanwhile, TD Cowen downgraded MOLINA from “Buy” to “Hold,” setting a target of $203, after raising its estimate for Molina’s medical loss ratio (MLR) to ~89.5%. These cautionary views reinforce the class’s core argument: that Molina’s cost assumptions were overly optimistic and materially misleading.

SEC Filings & Risk Factors

In its July 7, 2025 press release, Molina referenced “medical cost pressures in all three lines of business” and forecasted a “short-term earnings pressure” tied to a “dislocation between premium rates and medical cost trend.” While these disclosures appear transparent, the class‑action complaint contends Molina failed to meaningfully disclose the depth of its adverse cost trends. Specifically, it argues that Molina’s risk disclosures did not adequately emphasize how sensitive its business model is to utilization spikes in behavioral health, pharmacy, and inpatient services. The lawsuit also suggests that Molina’s forecast revisions only came after internal data revealed that its previously optimistic assumptions were not holding.

Conclusion: Implications for Investors

The Molina Healthcare class action is a stark reminder that in managed care, the margin for error is thin. Investors tend to trust forward guidance — but when that guidance is built on assumptions that don’t reflect surging utilization or cost inflation, the result can be brutal. Misaligned assumptions, especially in government‑backed health insurance, can lead to significant investor losses. As Molina fights this litigation, the broader sector may see an increased focus on the reliability of medical cost assumptions and the transparency of guidance. The lesson is clear: in volatile lines of business, aggressive growth narratives should be backed by equally rigorous risk modeling.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![CarMax, Inc. (KMX) Securities Class Action Update [November 12, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/kmx-update-banner-v2.webp)

![Telix Pharmaceuticals Ltd. (TLX) Securities Class Action Update [November 21, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/tlx-alert-plus-banner-image.png)

![DexCom, Inc. (DXCM) Securities Class Action Lawsuit Update [November 11, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/dxcm-alert-plus-banner.webp)