iRobot’s Standalone Reboot Crumbled. Investors Got Left in the Dust. August 24, 2025

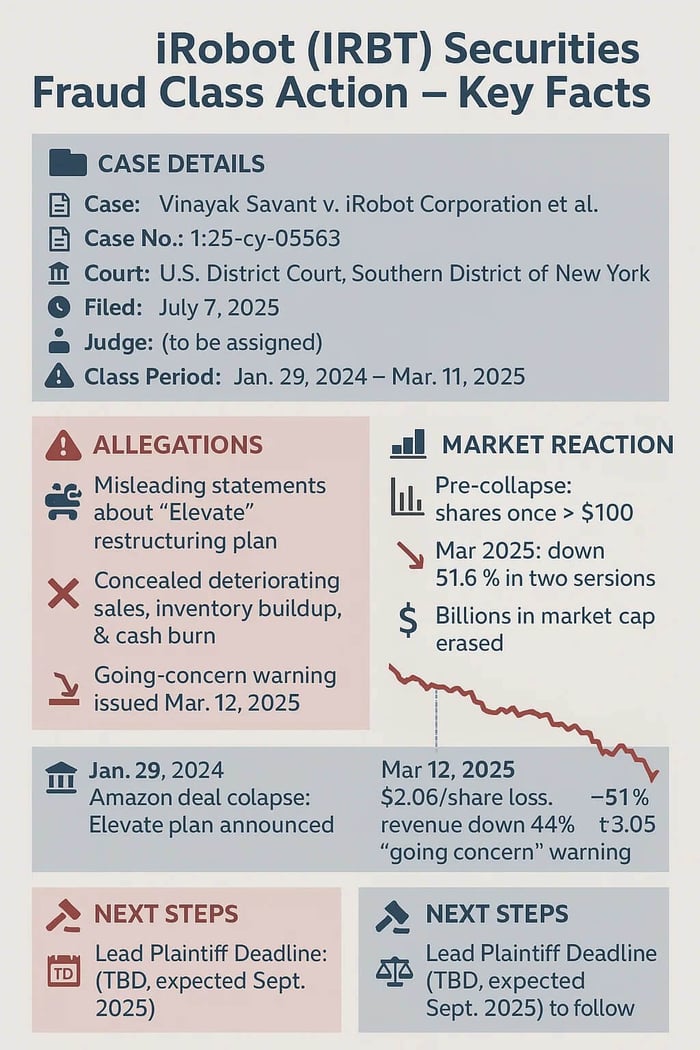

Caption: Savant v. iRobot Corporation, et al.

Case No.: 1:25-cv-05563

Jurisdiction: U.S. District Court, Southern District of New York

Filed on: July 7, 2025

Class Period: January 29, 2024 – March 11, 2025

Introduction

iRobot Corporation (the Roomba company) is facing down a securities lawsuit. It is accused of misleading shareholders about its ability to survive as a standalone company. On July 7, 2025, a complaint was filed against iRobot and four of its top executives (Glen D. Weinstein, Gary S. Cohen, Julie Zeiler, and Karian Wong).

Plaintiffs say the the Roomba manufacturer overhyped its “Elevate” restructuring plan, unveiled after the collapse of Amazon’s planned acquisition. From January 2024 through March 2025, management kept touting Elevate as a fantastic stabilizing reset. The lawsuit says this was just more hot air. iRobot’s fundamentals were deteriorating, and executives allegedly knew it.

The reckoning came on March 12, 2025. The company’s financials got vacuumed: iRBT reported a $2.06 per share loss, revenue plummeted 44% year-over-year. iRobot issued a “going concern” warning: usually a sign of crumbling financials and bad news to come. Analysts canceled the investor call. Within two sessions, the stock collapsed 51.6%, landing at $3.055. For shareholders who once believed in the Roomba story, the drop confirmed their worst fears.

Now, investors are suing.

Backdrop and Business Context

iRobot’s story stretches back more than three decades. MIT scientists founded the company back in 1990, but the company initially worked on defense contracts. In 2002, the company pivoted from national defense to dust defense, hitting mass-market success with the Roomba vacuum. For years, Roomba dominated the home robotics category and became synonymous with automated cleaning.

By the mid-2010s, iRobot’s market share was unmatched. It controlled almost two-thirds of the U.S. robot vacuum market. That dominance didn’t last. By 2020, cheaper rivals from China (like Ecovacs, Roborock, and others) had eaten into share, and dragged iRobot’s slice down to less than 50%. Competitors like SharkNinja and Samsung further chipped away even more market share. The Roomba manufacturer still held the “premium” mantle, but volumes and margins were slipping.

But then COVID provided a temporary reprieve. With people stuck at home during lockdowns, sales surged. But that bump proved unsustainable. By 2022, iRobot faced mounting debt, shrinking share, and pricing pressure from rivals: a tough triple-whammy to overcome. So, Amazon’s $1.7 billion deal in August 2022 looked like a lifeline. Investors cheered the deal and iRobot stock briefly stabilized.

The Amazon deal went belly-up, killed by regulatory ire. In January 2024, EU regulators raised antitrust concerns; meanwhile, the FTC also pushed back. The deal collapsed. Colin Angle, iRobot’s longtime CEO, stepped down. Roughly 31% of staff were cut. The company rolled out “Elevate,” a restructuring plan meant to focus on premium models, streamline operations, and reassure investors.

Elevate was billed as a turning point. But debt obligations loomed, tariffs shifted cost structures, and fresh competition didn’t let up. By mid-2025, the program was unraveling.

Promises Made vs. Reality

From day one of the Amazon deal collapse, management tried to instill confidence. On January 29, 2024, executives told investors that iRobot was “confident as a standalone” and that Elevate would create “sustainable value.”

Glen Weinstein, then interim CEO, told analysts the plan positioned iRobot for stabilization and renewed profitability. Cohen and Zeiler echoed that message in filings, pointing to efforts to capture mid-tier and premium customers. Press releases described Elevate as a disciplined reset, designed to navigate tariffs and margin pressure.

The lawsuit paints a very different picture. According to plaintiffs, internal data showed sales slipping, inventory swelling, and cash burn accelerating. The alleged reality: management knew Elevate couldn’t solve long-term viability, but continued to claim otherwise. Plaintiffs argue the program was never more than a stopgap—meant to buy time while avoiding disclosure of existential risks.

By early 2025, those risks had become impossible to hide. When the March 12 earnings hit, iRobot not only posted steep losses but admitted “substantial doubt” about its ability to continue as a going concern. The guidance for 2025? Withdrawn entirely.

Timeline of Alleged Misconduct and Disclosures

Class Period: January 29, 2024 – March 11, 2025

- Jan 29, 2024: Amazon deal terminated. Colin Angle resigns. Roughly 350 jobs cut. Elevate plan rolled out with promises of “confidence.” Shares dip.

- Throughout 2024: Quarterly calls and filings highlight Elevate progress, insist stabilization is underway.

- Mar 12, 2025: Q4/FY2024 results: loss of $2.06 per share, revenue of $172 million (down 44% year-over-year), going concern warning issued. Investor call canceled. Shares collapse 51.6% to $3.055 over two days.

- May 2025: A temporary stock pop follows tariff relief news, driven by short squeeze dynamics. But fundamentals remain unchanged

Investor Harm and Market Reaction

For investors, the fallout was brutal. Plaintiffs say they purchased shares at inflated levels, duped by management’s misstatements. By mid-March 2025, half of that value was gone. Billions in market capitalization were erased.

The pain was compounded by history. Pre-merger, shares once traded above $100. After the deal collapsed, they halved, but the March 2025 was the final nail in the coffin. Funds liquidated positions; retail investors vented online, complaining that the whole thing felt like a “betrayal.”

Analyst reactions were swift. Seeking Alpha downgraded to “sell,” citing a “bleak outlook” and “substantial doubts.” Similarly, Motley Fool ran a piece titled Why iRobot Stock Is Crashing Today, noting that the company’s restructuring costs (including a workforce cut of roughly 50%) hadn’t delivered stability; instead, matters just got worse for iRobot. Market volume spiked as investors fled.

Litigation and Procedural Posture

The lawsuit accuses iRobot and some of its top brass of violating Sections 10(b) and 20(a) of the Exchange Act, as well as SEC. Plaintiffs say executives acted with scienter—that they knew Elevate was inadequate and concealed that truth.

The suit wants a jury trial and seeks damages for the plaintiffs. Lead plaintiff motions are due soon, followed by briefing on dismissal. With a large shareholder base, discovery could be drawn out and contentious.

Shareholder Sentiment

Before March 2025, many retail investors still clung to hope. On Stocktwits in January 2024, one wrote: “$IRBT standalone—Elevate looks strong.” Reddit’s r/stocks in mid-2024 echoed optimism: “Restructuring rebound—Roomba is still king.” On X, users pointed to tariff relief and said value was ahead.

After the March disclosure, the mood turned. Stocktwits posts accused management of “lying about stability.” Reddit threads described Elevate as a flop: “They knew it was unviable.” On X, users called the company “a house of cards” and admitted dumping shares at $3. Others recounted buying at $20 and holding through the collapse.

Some traders briefly speculated on tariff-driven pops in May 2025. But for most, trust was gone. The company went from a possible turnaround to what posters called a “ponzi” in disguise.

Analyst Commentary

Analyst coverage wasn’t kind. Pre-disclosure, some framed Elevate as a plausible turnaround. But after March 12, analyst’s ire was evident:

- Seeking Alpha (Mar 12, 2025): Downgraded to sell. Warned of “disastrous Q4,” worsening margins, and doubts about viability over 12 months.

- The Motley Fool (Mar 12, 2025): Explained the collapse, pointing to costly restructuring and competition from low-cost Chinese rivals.

- By mid-2025, consensus was clear: Elevate had failed, and iRobot’s independence was in doubt.

SEC Filings & Risk Factors

The company’s filings reflected optimism but, plaintiffs say, left out key risks.

- FY2022 10-K (year ended Jan 28, 2023): Praised premium positioning and pet humanization, listed broad consumer spending risks.

- FY2020 10-K: Noted shifting preferences, competition.

- Prospectus materials: Emphasized premium focus.

- Jan 29, 2024 8-K: Detailed $12–$13M restructuring charges after merger termination

- Mar 12, 2025 8-K: Reported steep losses and issued “going concern” warning.

Plaintiffs argue omissions concealed iRobot’s fragility, particularly its dependence on debt financing and inability to fend off competition.

Conclusion: Investor Implications

The iRobot case shows how fragile merger-driven stories can be. A regulatory block, a rushed restructuring, and assurances that proved empty. But, behind the scenes, things were falling apart at iRBT and fast. Sometimes, a merger hides rot just beneath the surface.

For shareholders, the lessons echo others in securities litigation: be wary of confident language unsupported by fundamentals, watch for repeated guidance without detail, and treat going-concern warnings as more than footnotes. In industries facing heavy competition, one failed plan can erase decades of brand equity. Plaintiffs now press their case in court. For investors, the warning is clear: hype fades, but losses linger.

![Alto Neuroscience, Inc. (ANRO) Securities Class Action Lawsuit Update [September 10, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/anro-shareholder-alert-blog-banner.webp)