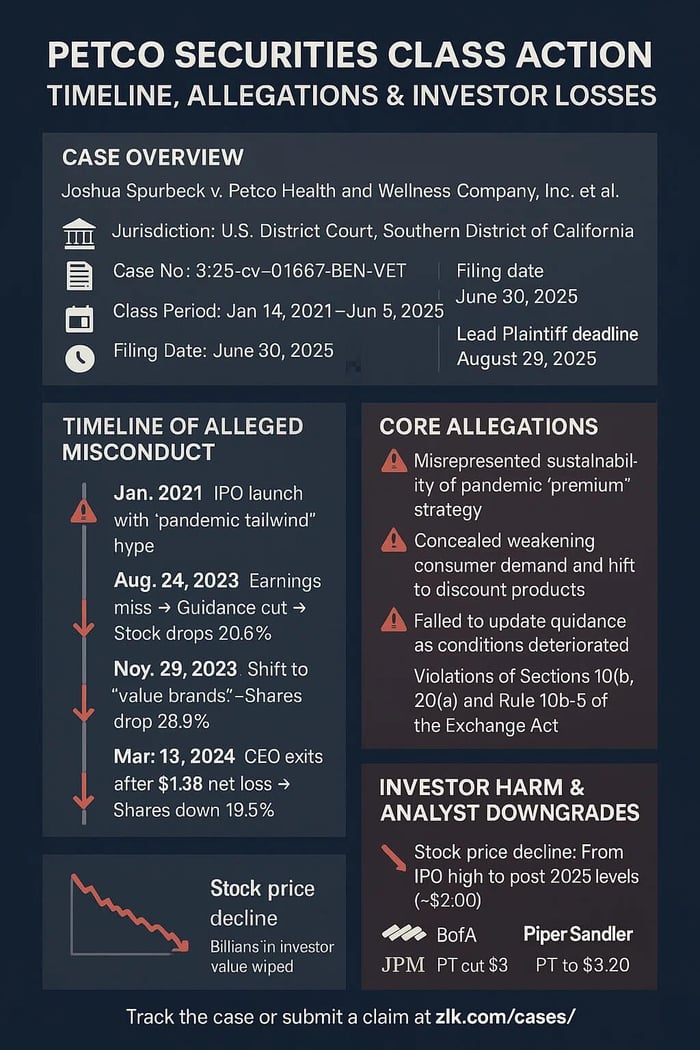

Caption: Spurbeck v. Petco Health and Wellness Company, Inc., et al.

Case No.: 3:25-cv-01667-BEN-VET

Jurisdiction: U.S. District Court, Southern District of California

Filed on: June 30, 2025

Class Period: January 14, 2021, to June 5, 2025

Introduction

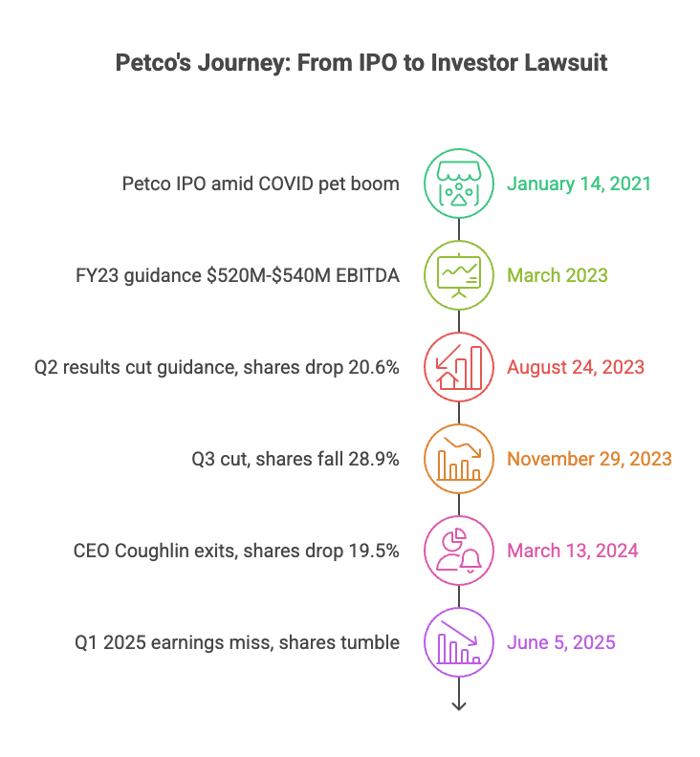

Petco Health and Wellness Company, Inc.—once riding high on pandemic pet adoptions—now stares down a securities lawsuit. Plaintiffs say Petco and some of its execs (Joel D. Anderson, R. Michael Mohan, Ronald V. Coughlin, Jr., Sabrina Simmons, Brian Larose, and Michael Nuzzo) misled buyers from January 14, 2021, to June 5, 2025 (the “Class Period”). Petco’s top dogs touted sustainable tailwinds from COVID pet surges and a premium "humanization" strategy, even as sales tanked. Reality hit with guidance cuts, executive exits, and stock plunges—like 20.6% on August 24, 2023, to $5.19. This unravels the claims, Petco's ops, investor pain, and signals for retail chasers.

Backdrop and Business Context

Petco peddles pet gear—food bowls gleaming, leashes taut, premium kibble stacked high. It runs stores, vets, groomers, online hubs. Born in 1965, it went public January 2021 amid COVID pet frenzy, adoption rates spiking, folks treating furballs like family. The "yield" was premium focus: no-artificial-ingredient chow, betting on "humanization" where millennials splurge on organic treats. Comparable sales—same-store growth—became the pulse. But post-lockdown, tailwinds faded. Cheaper rivals bit in. By mid-2023, metrics soured, yet execs swore the premium pivot held. (It didn't.) Financing stayed steady, but consumer shift to bargains exposed the fragility.

Promises Made vs. Reality

Execs sold endurance. January 2021 IPO: Pandemic "tailwinds" sustainable, premium strategy "uniquely positioned." Coughlin on calls: "Pet humanization" drives "healthy, premium" sales. FY23 guidance March 2023: Adjusted EBITDA $520M-$540M, EPS $0.40-$0.48. Reaffirmed May: "Strength" intact. Filings echoed: Growth from "no artificial" foods.

Lawsuit flips it. Tailwinds crashed; premium push faltered as shoppers pinched pennies. Insiders knew—adoptions dropped, "value" brands needed—but hid. "Reset" was delay. Reality: Cheaper goods flooded shelves by November 2023.

Timeline of Alleged Misconduct and Disclosures

Deception spanned January 14, 2021, to June 5, 2025—the Class Period.

- January 2021: IPO hypes pandemic surge, premium edge. Shares debut strong. Through 2022: Calls tout "sustainable tailwinds," comp sales up.

- March 2023: FY23 guidance $520M-$540M EBITDA.

- May 2023: Reaffirmed.

- August 24, 2023: Q2 results slash guidance to $460M-$480M EBITDA, $0.24-$0.30 EPS. "Consumer shift" cited. Shares drop 20.6% to $5.19.

- November 29, 2023: Q3 cuts to $400M EBITDA, $0.08 EPS. "Value" brands added. Shares fall 28.9% to $2.73.

- March 13, 2024: Coughlin out as CEO. Q4: Comp sales down 0.9%, $1.3B net loss. Premium model "not sustainable." Shares drop 19.5% to $2.06 over two days.

- April 9, 2024: Chief Customer Officer fired. Shares slip 2.1% to $1.85.

- June 5, 2025: Q1 2025 earnings miss, more cuts. Shares tumble further.

Investor Harm and Market Reaction

The unraveling gutted holders. Spurbeck, class voice, bought high, watched evaporate. August 2023: 20.6% wipeout. November: 28.9% bloodletting. March 2024: 19.5% over Coughlin exit, earnings bomb. Total: Billions in cap vaporized. Pension pots, retail dreams—shattered by broken "premium" vows. Analysts piled on: Morgan Stanley to $12, "damage deep." Barclays underweight, "yield gone." Volume spiked, funds fled. Market spat on excuses. Ran. Buried risks multiplied the sting.

Litigation and Procedural Posture

Southern California filing nails Petco, Anderson, Mohan, Coughlin, Simmons, Larose, Nuzzo for 10(b), Rule 10b-5, 20(a) control breaches. Scienter: Knew tailwinds fleeting, premium failing, but concealed. No insider sales cited, but omissions fuel. Seeks class, jury, damages. Early: Lead plaintiff deadline August 29, 2025, dismiss fights loom. Vast shareholder pool hints ugly discovery.

Shareholder Sentiment

Pre-2023, retail buzzed warm. Stocktwits 2021: "$WOOF riding pet boom—premium's gold." Reddit r/stocks early 2022: "Humanization trend? All in." X mid-2022: "$WOOF tailwinds forever—adoptions up." Saw fortress in fur frenzy.

Post-drops? Venom. Stocktwits August 2023: "Guidance slash? Lied on premium." Reddit r/investing November: "Value pivot? Knew premium dead." X March 2024: "$WOOF Coughlin out—house cards." Another: "Held $20, now $2. Betrayed." Some eyed rebound via vets. Most? Dumped. From boom darling to bust tale—trust torched, "scam" whispers loud.

Analyst Commentary

Before major misses, analysts leaned positive. Guggenheim held $8 target early 2023, citing "growth potential." Wolfe initiated Peer Perform Sept 2023. BMO Hold mid-2023, around $6.

After the August 2023 cut, Wedbush to $4.50 Outperform. After Nov, Baird to $3.50 Neutral, Morgan Stanley to $4.50 Equal-weight. BofA to $1.5 Apr 2024. Consensus bearish, flagging "demand weakness."

Analyst responses to Petco’s Q1 2025 earnings report (June 5, 2025) were mixed but leaned bearish due to revenue declines and ongoing challenges, despite an earnings beat. Below is a summary based on available information:

- Bank of America: Slashed price target from $5 to $3, maintaining an Underperform rating, citing “trust killer” impact from the Novo Nordisk split and revenue headwinds from lost Wegovy access. They noted weakened brand credibility and potential regulatory scrutiny.

- J.P. Morgan: Reduced target from $6 to $3.50, keeping a Neutral rating, highlighting “deceptive marketing” concerns and predicting challenges in rebuilding consumer trust amid a resolved semaglutide shortage squeezing Petco’s compounded drug niche.

- Piper Sandler: Cut target from $7 to $3.20, downgrading to Neutral, pointing to credibility loss from the Novo fallout and questioning Petco’s ability to pivot to other revenue streams effectively.

- General Sentiment: Analysts acknowledged Petco’s adjusted EBITDA beat ($89.45M vs. $80.68M expected) and EPS beat (-$0.04 vs. -$0.05), but the 2.3% year-over-year revenue decline to $1.49B and softer Q2 guidance ($1.49B vs. $1.50B expected) fueled downgrades. Concerns centered on persistent traffic softness, tariff impacts, and the shift to value-oriented products, signaling doubts about Petco’s premium strategy sustainability.

The consensus shifted from cautious optimism to skepticism, with analysts flagging long-term growth hurdles and competitive pressures in the pet retail sector.

SEC Filings & Risk Factors

Petco’s filings touted premium strategy and tailwinds while downplaying risks. The FY2022 10-K (ended Jan 28, 2023) highlighted "pet humanization" driving premium sales but warned broadly of consumer spending shifts and competition in risk factors. Earlier FY2020 10-K summarized risks including preferences changes. Prospectus emphasized integrated premium offerings.

August 24, 2023 8-K: Q2 results, guidance cut to $460M-$480M EBITDA due to discretionary pressures. November 29, 2023 8-K: Q3 cut to $400M, value brands added. March 13, 2024 8-K: Q4 net loss $1.3B, Coughlin exit; acknowledged premium unsustainability. April 9, 2024 8-K: Chief Customer Officer termination. June 5, 2025 8-K: Q1 2025 results miss, guidance assumes tariffs.

Suit alleges omissions hid tailwind fade and premium weakness, leaving investors exposed to consumer bargain shifts.

Conclusion: Investor Implications

Petco's tumble exposes retail fragility. Pandemic highs, premium bets—probe beneath. Flags: Tailwind hype, guidance clings, exec exits. In pet space, consumer whims kill; one shift, yields evaporate. Suit watchers wait. Lesson bites: In furry boom gloss, hunt cracks—or watch dividends flee like scared cats.

![Alto Neuroscience, Inc. (ANRO) Securities Class Action Lawsuit Update [September 10, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/anro-shareholder-alert-blog-banner.webp)