Table of Contents

- Defining Insider Trading: Understanding the Basics

- The Legal Landscape of Insider Trading

- Recognizing Illegal Insider Trading Practices

- Role of Regulatory Bodies in Monitoring Insider Trading

- Consequences and Penalties for Engaging in Insider Trading

- Can You Be Held Liable for Sharing Insider Information?

- Accidental Insider Trading: Can It Happen?

- Legal Strategies and Defenses in Insider Trading Cases

- Preventative Measures: How to Stay Compliant

- Insider trading is not always illegal, but it is always closely scrutinized.

- FAQs

Insider trading is a term that evokes strong reactions, often associated with high-profile scandals, courtroom drama, and the image of unscrupulous executives exploiting confidential information for personal gain.

But is insider trading always illegal? Or is it a concept that is widely misunderstood, with nuances that often escape public discourse?

This blog delves into the complex realm of insider trading, examining its legal and illicit forms, the regulatory framework that governs it, and the broader implications for financial markets and investor confidence.

Defining Insider Trading: Understanding the Basics

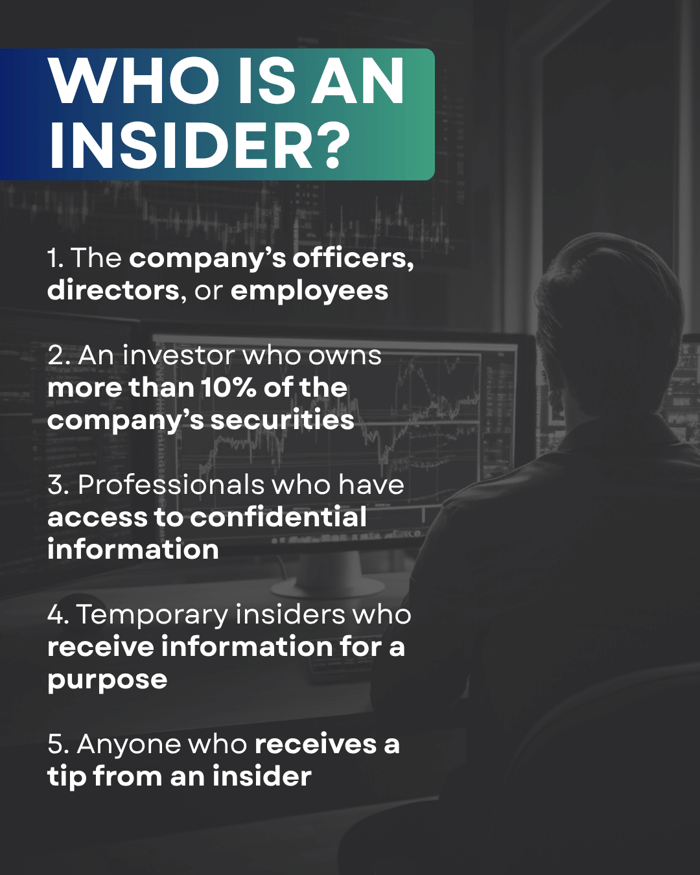

The Concept of an "Insider"

At its core, insider trading refers to buying or selling a security in breach of a fiduciary duty or other relationship of trust and confidence while in possession of material, nonpublic information about the security. But who exactly is an "insider"?

According to the U.S. Securities and Exchange Commission (SEC), an insider is typically:

A company’s officers, directors, or employees;

Anyone who owns more than 10% of a company’s securities (section 16, SEC Act, 1934);

Professionals such as lawyers, accountants, or consultants who have access to confidential information through their work;

“Temporary insiders” who receive confidential information for a specific purpose;

Anyone who receives a tip from an insider and trades on that information (so-called “tippees”).

Material Information: What Constitutes Value?

For information to be relevant in the context of insider trading, it must be material and significant. The Securities Act of 1933 defines material information as anything a reasonable investor would consider necessary in making an investment decision.

Examples include:

Earnings reports and financial results have not yet been released to the public.

News of mergers, acquisitions, or divestitures.

Changes in executive leadership.

Regulatory approvals or denials.

Significant product launches or recalls.

The U.S. Supreme Court, through its judgments in landmark cases like Basic Inc. v. Levinson, 485 U.S. 224 (1988), and TSC Industries v. Northway, has defined material information as information that “would be viewed by the reasonable investor as having significantly altered the ‘total mix’ of information made available.”

Public vs. Nonpublic Information: A Clear Distinction

The distinction between public and nonpublic information is fundamental.

Public information is widely disseminated and available to all investors, including through press releases, SEC filings, and news reports. Nonpublic information is confidential and not yet available to the investing public.

Trading on nonpublic, material information is where insider trading laws are most concerned.

The Legal Landscape of Insider Trading

Key US Regulations Governing Insider Trading

The U.S. has a robust legal framework to regulate insider trading, primarily anchored by:

Securities Exchange Act of 1934: The foundational law that prohibits manipulative and deceptive practices in securities trading.

SEC Rule 10b-5: The key anti-fraud provision that makes it unlawful to “employ any device, scheme, or artifice to defraud” in connection with the purchase or sale of securities.

Insider Trading Sanctions Act of 1984 and Insider Trading and Securities Fraud Enforcement Act of 1988: These acts increased the penalties for insider trading and expanded the SEC’s enforcement powers.

Legal vs. Illegal Insider Trading: The Fine Line

Legal insider trading occurs when corporate insiders—such as officers, directors, and employees—buy and sell stock in their own companies, provided they do so under SEC rules and report their trades to the SEC.

These transactions are disclosed to the public through SEC Form 4 filings.

Illegal insider trading happens when someone trades a security while in possession of material, nonpublic information, in violation of a duty of trust or confidence.

Rule 10(b)-5 of the Securities Exchange Act of 1934 asserts that illegal insider trading also includes “tipping” others who then trade on the information.

Recognizing Illegal Insider Trading Practices

Illegal insider trading can take many forms, including:

Executives trading ahead of earnings announcements.

Employees tipping friends or family about confidential company news.

Lawyers or consultants using privileged information to trade.

“Front-running” by brokers who use client information for personal gain.

Types of Insider Trading Violations

Violations can be divided into two main categories:

Classical Theory: When a corporate insider trades on material nonpublic information in breach of a fiduciary duty to shareholders.

Misappropriation Theory: When someone misappropriates confidential information for securities trading, in breach of a duty owed to the source of the information.

Examples of Legal Precedents in Insider Trading Cases

United States v. O’Hagan (1997): The Supreme Court upheld the misappropriation theory, holding that a lawyer who traded on confidential information from a client was guilty of insider trading.

United States v. Newman (2014): The Second Circuit ruled that tippees must know that the insider disclosed information in exchange for a personal benefit.

SEC v. Texas Gulf Sulphur Co. (1968): Early landmark case establishing that anyone in possession of material, nonpublic information must either disclose it or abstain from trading.

Role of Regulatory Bodies in Monitoring Insider Trading

The SEC’s Key Functions and Responsibilities

The Securities and Exchange Commission (SEC) is the primary federal agency responsible for enforcing laws against insider trading. Its functions include:

Investigating suspicious trading activity;

Bringing civil enforcement actions against violators;

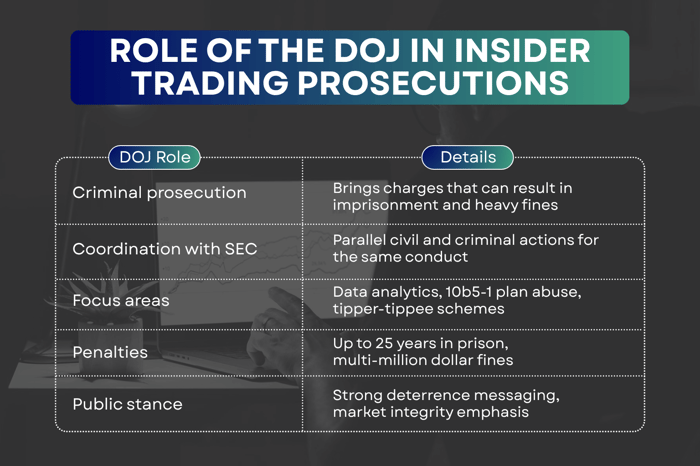

Working with the Department of Justice (DOJ) for criminal prosecutions;

Promoting market transparency and investor education.

The SEC maintains a dedicated Market Abuse Unit and leverages advanced analytics to detect unusual trading patterns.

How Regulatory Frameworks Evolve Over Time

Regulatory frameworks have evolved in response to new trading technologies, globalization, and increasingly sophisticated schemes.

The SEC regularly updates its rules and guidance, and Congress has passed new laws to strengthen enforcement and increase penalties.

Technological Advances in Detecting Insider Trading

The SEC and other regulators now use cutting-edge technology, including:

Algorithmic surveillance: Automated systems flag suspicious trades for further review.

Big data analytics: Cross-referencing trading data with news events and social media.

Whistleblower programs: Incentivizing insiders to report wrongdoing.

Consequences and Penalties for Engaging in Insider Trading

Civil vs. Criminal Penalties: Understanding the Differences

Penalties for insider trading are severe and can be both civil and criminal:

Civil penalties: Disgorgement of profits, fines up to three times the profit gained or loss avoided, and bans from serving as officers or directors (Insider Trading and Securities Fraud Enforcement Act of 1988).

Criminal penalties: Fines up to $5 million for individuals ($25 million for entities) and up to 20 years in prison (Section 10(b) of the Securities Exchange Act of 1934 and SEC Rule 10b-5).

The SEC also has the authority to freeze assets, seek injunctions, and bar individuals from the securities industry.

Broader Implications for Financial Markets and Investor Trust

Insider trading undermines the integrity of financial markets.

If investors believe the market is rigged in favor of insiders, they may lose confidence and withdraw their capital, reducing liquidity and increasing the cost of capital for companies.

Can You Be Held Liable for Sharing Insider Information?

Secondary Liability: Understanding the Implications

You don’t have to trade yourself to be liable for insider trading.

Tipping—passing material, nonpublic information to someone else who then trades—can also lead to insider trading liability for both the tipper and tippee if the tipper receives a personal benefit.

How Scope of Knowledge Affects Legal Accountability

For liability, the tippee must know or should have known that the information was obtained in breach of a duty. (Dirks v. SEC)

Courts have debated what constitutes a “personal benefit”, with recent rulings narrowing the definition.

Accidental Insider Trading: Can It Happen?

Unintended Consequences: The Gray Areas of Insider Trading

Sometimes, individuals may inadvertently engage in insider trading (Section 10(b) of the Securities Exchange Act of 1934 and SEC Rule 10b-5).

For example, if an employee overhears confidential information in an elevator and trades on it, they could be liable, even if they didn’t realize the info was nonpublic.

Examples of Unintentional Violations and Their Outcomes

Here are several real-world examples that illustrate how accidental insider trading can occur:

1. In 2013, Tyrone Hawk overheard his wife discussing her company’s upcoming acquisition during a work call. Despite being told not to trade, Hawk bought shares in the target company before the deal was announced and profited $150,000.

The SEC charged him with insider trading, and he ultimately paid over $300,000 to settle the case. This example shows how even indirect exposure to confidential information—combined with a decision to trade—can lead to serious consequences, regardless of whether the information was intentionally sought out.

2. During the COVID-19 pandemic, Steven Teixeira accessed nonpublic information from his girlfriend’s laptop while she worked remotely at an investment bank.

Teixeira used this information to trade call options and tipped off friends, resulting in illicit profits for himself and others.

The SEC charged both Teixeira and his friend, Jordan Meadow, with insider trading. This case illustrates how remote work environments can inadvertently expose sensitive information to household members, resulting in unintentional breaches.

3. Daniel Moscatiello was charged by the SEC after trading on material nonpublic information he received from his mother.

Although Daniel was an inexperienced trader and had not traded in years, he acted on the tip immediately after speaking with her, purchasing a large number of call options and making significant profits.

The SEC used the timing and nature of the trades to demonstrate that the action was prompted by the tip, not by coincidence. Moscatiello was required to disgorge his profits and pay penalties.

4. Employees are often restricted from trading during specific periods (blackout windows) to prevent misuse of insider information.

In some cases, employees have traded during these periods, not realizing that the restriction was in place due to pending material events.

Even if the employee did not intend to break the rules, the SEC may still bring enforcement actions if the trades coincide with undisclosed material developments.

5. In the SEC v. Panuwat case, an employee used confidential information about his own company’s pending merger to trade in the securities of another company likely to be affected by the news.

While the employee may not have realized this was a violation, the SEC successfully argued that using any material nonpublic information—regardless of whether it directly relates to the company whose securities are traded—can constitute insider trading if it breaches a duty of trust.

Legal Strategies and Defenses in Insider Trading Cases

Key Defense Arguments Used in Insider Trading Cases

Common defenses include:

The information was neither material nor non public.

The trade was pre-planned under a Rule 10b5-1 trading plan.

The trader did not owe a duty of trust or confidence;

Lack of scienter (intent to defraud) (example: Ernst & Ernst v. Hochfelder (1976)).

What to Do If You’re Accused of Insider Trading

If accused, it’s crucial to:

Retain experienced legal counsel immediately.

Preserve all communications and trading records.

Cooperate with authorities while protecting your rights.

The Role of Legal Counsel: Importance of Experienced Representation

Insider trading cases are complex and require specialized legal expertise. The SEC and DOJ have vast resources, and penalties can be life-altering.

At Levi & Korsinsky, LLP, we specialise in legal counsel for investor class action lawsuits, representing shareholders who have suffered financial losses due to securities fraud, corporate misconduct, and deceptive investment practices.

With over 80 collective years of experience, our experienced attorneys are on hand to provide you with the support and legal expertise you need to maximise your recovery.

Preventative Measures: How to Stay Compliant

Best Practices for Corporate Insiders and Employees

Adopt clear insider trading policies and regularly train employees on what constitutes material, non-public information.

Implement blackout periods: Restrict trading around earnings announcements and significant events.

Require pre-clearance of trades: Have compliance officers review trades by insiders.

Understanding Safe Harbor Rules and Trading Plans

Rule 10b5-1 trading plans enable insiders to pre-schedule trades, providing a defense against accusations of trading on inside information, provided the plan is established in good faith before the insider possesses material non-public information.

Investor Education: Recognizing Red Flags of Insider Trading

Investors should be wary of:

Unusual spikes in trading volume before major announcements;

Sudden price movements without public news;

Patterns of successful trades by company insiders.

Insider trading is not always illegal, but it is always closely scrutinized.

Legal insider trading, when done transparently and in compliance with regulations, is a regular part of corporate life.

Illegal insider trading, however, undermines the integrity of financial markets and carries severe penalties.

As markets evolve and technology advances, so too do the methods for detecting and prosecuting insider trading. For investors, companies, and employees alike, understanding the rules and staying vigilant is essential for maintaining trust in the financial system.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal advice. Readers should not act or refrain from acting on any of the information contained in this blog without consulting a qualified legal professional. Levi & Korsinsky LLP is not responsible for any actions taken or not taken based on the information provided in this blog.

You Can Also Read |

FAQs

What Is Insider Trading? What qualifies for insider trading?

Trading a security while in possession of material, nonpublic information, in breach of a duty of trust or confidence.

When is Insider Trading Illegal?

When it involves trading on material, nonpublic information in violation of a duty owed to the company or its shareholders.

Can insider trading ever be legal?

Yes, when insiders trade and adequately disclose their trades to the SEC, or when trades are made under pre-established Rule 10b5-1 plans.

What is an example of illegal insider trading?

A CEO selling company stock before announcing negative earnings results, based on knowledge not yet public.

How Does Insider Trading Impact the Broader Market?

It erodes investor confidence, increases the cost of capital, and undermines the perceived fairness of financial markets.

Are There Exceptions to Insider Trading Rules?

No, but legal defenses exist if trades are made without material, nonpublic information or under pre-established plans.

Who Can Report Suspicious Insider Trading Activities?

Anyone can report to the SEC’s Office of the Whistleblower, which offers financial rewards for tips that lead to enforcement actions.

How Does the SEC Detect and Investigate Illegal Insider Trading?

Through advanced data analytics, market surveillance, whistleblower tips, and cooperation with other agencies.

What are the penalties for illegal insider trading?

Civil fines up to three times the profit gained or loss avoided, criminal fines up to $5 million, and up to 20 years in prison.

How is insider information defined in the context of insider trading?

Material, nonpublic information that would influence an investor’s decision to buy or sell securities.