![Lantheus Holdings, Inc. (LNTH) Securities Class Action Lawsuit Update [December 24, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/lnth-alert-plus-banner.webp)

LNTH: When Pricing Power Proved Fragile

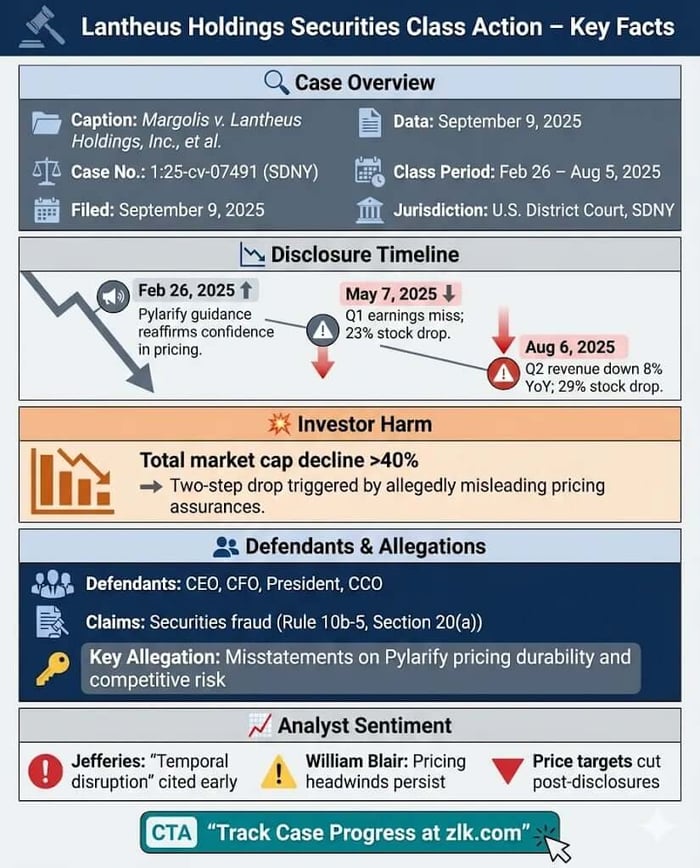

Case Name: Margolis v. Lantheus Holdings, Inc., et al.

Case No.: 1:25-cv-07491

Jurisdiction: U.S. District Court, Southern District of New York

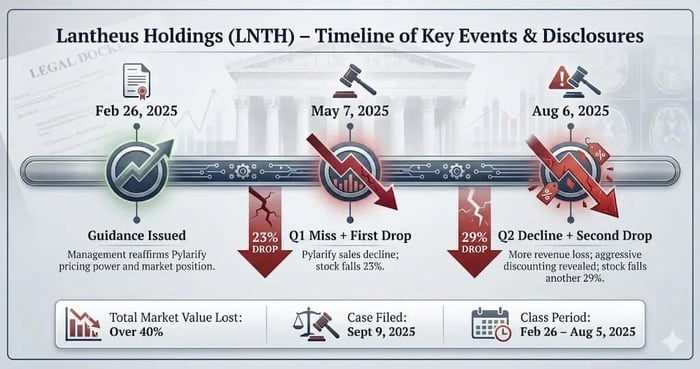

Filed on: September 9, 2025

Class Period: February 26, 2025–August 5, 2025

Introduction

Lantheus Holdings, Inc. told investors its flagship prostate cancer imaging agent, Pylarify, was insulated from competition. The market believed it—until it didn’t. In September 2025, a federal securities class action was filed in the Southern District of New York alleging that Lantheus Holdings, Inc. and senior executives misled investors about pricing power, competitive dynamics, and revenue visibility tied to Pylarify. When those assumptions cracked, the stock collapsed in two violent steps. Now, investors are fighting back.

“Most LNTH shareholders never file or join the class action, which means they miss out on potential recovery funds,” said Attorney Joe Levi.

Backdrop and Business Context

Lantheus is a radiopharmaceutical diagnostics company whose growth story has been dominated by Pylarify, a PSMA PET imaging agent used in prostate cancer diagnosis and treatment. By early 2025, Pylarify had crossed the $1 billion annual revenue mark and was framed internally as both category leader and premium-priced standard of care.

The company did not come public through a speculative SPAC structure; it was already established, profitable, and analyst-covered. That context matters. Investors were not buying an untested science project. They were buying predictability—recurring demand, durable pricing, and management’s claimed command of reimbursement and competitive forces.

That narrative, according to the complaint, depended on one fragile premise: that Lantheus truly understood the pricing elasticity of Pylarify in a market undergoing reimbursement shifts and competitive reawakening.

Promises Made vs. Reality

Throughout late 2024 and early 2025, executives repeatedly emphasized Pylarify’s “clear market leadership” and ability to maintain a “pricing premium,” even as competitors repositioned and Medicare reimbursement mechanics shifted. On earnings calls, management described competitive noise as manageable and temporary, assuring investors that pricing normalization would follow brief disruptions.

Those assurances were categorical. Management spoke as if they possessed granular visibility into customer behavior, contract durability, and competitor intent. Analysts pressed. Executives doubled down.

The complaint alleges that, internally, the picture was less controlled. Pricing pressure had already begun to surface in late 2024. A price increase implemented in early 2025, despite earlier erosion, allegedly created an opening for aggressive discounting by competitors—particularly among smaller, non-contracted imaging centers. Investors were not told that Pylarify’s premium position was increasingly optional rather than essential.

The result, plaintiffs say, was a market misled into believing growth headwinds were theoretical when they were already operational.

Timeline of Alleged Misconduct and Disclosures

The class period runs from February 26, 2025 through August 5, 2025.

On February 26, 2025, Lantheus issued full-year guidance projecting Pylarify growth in the low-to-mid single digits, stressing confidence in pricing and competitive positioning.

The first crack appeared on May 7, 2025, when Lantheus reported first-quarter results below expectations. Pylarify sales declined year-over-year, and management attributed the shortfall to a “temporal competitive disruption.” Full-year growth guidance was cut. The stock fell more than 23% in a single session, erasing months of gains.

Management framed the disruption as contained. Investors were told pricing pressure would normalize. The market hesitated, but many stayed in.

On August 6, 2025, the second disclosure landed harder. Pylarify sales fell again—down over 8% year-over-year—and guidance was slashed for a second time. Executives acknowledged aggressive discounting by competitors, renegotiated contracts, and deliberate walk-aways from unprofitable volume. The stock dropped another nearly 29% in one day.

By then, the narrative of control had collapsed.

Investor Harm and Market Reaction

Across the two disclosure events, Lantheus lost well over 40% of its market value. For investors who purchased during the class period, losses were not abstract—they were immediate and severe.

Analysts reacted quickly. Price targets were cut. Notes emphasized that Pylarify’s volume growth masked deeper price/mix deterioration. Several firms highlighted that competitors were growing faster, even as Lantheus surrendered pricing to defend share.

The alleged loss causation is direct: optimistic guidance and assurances inflated the stock; corrective disclosures revealed the truth; the price fell. Twice.

Litigation and Procedural Posture

The action is captioned Margolis v. Lantheus Holdings, Inc., et al., Case No. 1:25-cv-07491, pending in the U.S. District Court for the Southern District of New York.

The complaint asserts claims under Section 10(b) of the Securities Exchange Act and Rule 10b-5, as well as Section 20(a) control-person liability against senior executives, including the CEO, CFO, President, and Chief Commercial Officer.

Scienter is alleged through repeated, confident statements about pricing dynamics and competitive understanding, juxtaposed against later admissions that management underestimated the durability and intensity of competitive discounting. The case is in its early stages, with motions to dismiss expected.

Shareholder Sentiment

Investor sentiment toward Lantheus Holdings ($LNTH) shifted markedly in 2025, starting with optimism around Pylarify's blockbuster status and pipeline potential, then turning to frustration amid pricing pressures, competitive headwinds, and guidance cuts following Q1 and Q2 earnings misses. Stock drops of ~20-29% in May and August triggered a securities class action lawsuit.

Early 2025, there was optimism and strong confidence in Pylarify's durability and growth. X posts contained bullish calls on undervaluation and 2026 catalysts.

May-August disclosures produced shock and anger. The Q1 miss and first guidance cut (May), followed by Q2 decline in Pylarify sales (~8% YoY) and further cuts (August), led to sharp reactions from X/Reddit. There was limited direct outrage visible, but discussions noted "headwinds" and reimbursement shifts chipping at share.

Post-August, many holders express skepticism on near-term recovery but see value in diversification (acquisitions, pipeline). Tone: "Undervalued but wait for proof of stabilization." Overall, trust in management's prior certainty eroded, with sentiment now cautiously opportunistic ahead of 2026 events. Many view the episode as a lesson in healthcare reimbursement sensitivity.

Analyst Commentary

Professional analyst coverage of Lantheus shifted markedly over the course of 2025 as Pylarify’s performance disappointed and strategic risk surfaced.

In the immediate aftermath of the May 7, 2025 first-quarter earnings, analysts reacted to weaker-than-expected results and the company’s acknowledgment of “temporal competitive disruption” among smaller non-contracted sites—a phrase that offered comfort but not clarity on pricing resilience. Several well-known analysts lowered price targets or adopted more cautious language, reflecting diminished confidence in Pylarify’s near-term growth trajectory and the reliability of management’s outlook. According to the complaint, Jefferies noted that while “LNTH continues to maintain that strategic partnerships have been secured with the vast majority of its key customers,” the call also highlighted “temporal competitive disruption” as a meaningful headwind affecting pricing and volume dynamics, echoing broader market skepticism.

After the August 6, 2025 second quarter disclosure, the tone hardened further. Data in the lawsuit shows that William Blair, while maintaining a Market Perform rating, pointed to “weaker-than-expected Pylarify revenue” and reiterated concerns about share loss amid aggressive competitor pricing—factors now baked into earnings guidance. Analysts at Jones Research similarly warned that “sustained competitive pressure is creating headwinds for the company’s lead asset, PYLARIFY,” noting that even though volume might stay positive through fiscal 2025, growth would lag broader PSMA-PET market trends. Jefferies also slashed its price target, explicitly linking competitive discounting and renegotiated deals to price/mix deterioration.

Beyond the class period, subsequent commentary has remained guarded. Broader equity analysts have trimmed fair value estimates modestly, with consensus price targets declining as the company navigates both pricing pressure and acquisition-related execution risks. Coverage notes that earnings guidance was narrowed following the third quarter results, with some analysts questioning whether new franchise growth or licensing arrangements (like the exclusive agreement with GE HealthCare in Japan) will be enough to offset Pylarify headwinds.

Across the coverage, the common thread is clear: what began as a managed competitive disruption evolved into a structural challenge for Pylarify’s pricing model, prompting revisions to growth expectations and a recalibration of valuation assumptions among sell-side analysts.

SEC Filings & Risk Factors

Lantheus’ SEC filings contained standard risk disclosures about competition, reimbursement changes, and pricing pressure. The lawsuit does not allege the absence of risk factors; it alleges their inadequacy.

According to plaintiffs, generic warnings about competition did not meaningfully disclose that Pylarify’s pricing model was already under strain, or that internal forecasting processes failed to capture the real-time impact of aggressive discounting. Forward-looking statements, they argue, were presented without sufficient caution or internal support.

That gap—between disclosure formality and operational reality—sits at the center of the case.

Conclusion: Implications for Investors

The Lantheus case is not about a failed drug or an unexpected regulatory shock. It is about confidence. About what happens when management speaks with certainty in markets defined by elasticity, incentives, and human behavior.

For investors, the lesson is familiar but still costly: pricing power is never permanent, and confidence is not a substitute for evidence. Especially in healthcare markets shaped by reimbursement and competition, narratives age quickly.

This isn’t a closing argument. It’s a reckoning.

How to Join the Lantheus Holdings, Inc. (LNTH) Class Action

Confirm you purchased LNTH shares during the relevant period

Review eligibility details

Click here to check eligibility: https://zlk.com/pslra-1/lantheus-holdings-inc-lawsuit-submission-form-2?wire=54

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![BellRing Brands, Inc. (BRBR) Securities Class Action Lawsuit Update [January 27, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/brbr-alert-plus-banner.webp)

![Savara Inc. (SVRA) Securities Class Action Lawsuit Update [January 5, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/svra-alert-plus-banner.webp)

![Smart Digital Group Limited (SDM) Securities Class Action Lawsuit Update [January 19, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/sdm-alert-plus-banner.webp)