Table of Contents

- Where Did the Securities and Exchange Commission Come From?

- How is the SEC Organized?

- What are the SEC’s Tools Against Fraud?

- What are some Famous SEC Cases: When Enforcement Hits

- How Do SEC Fines and Settlements Help Investors?

- How Does the SEC Differ from FINRA?

- How Does the SEC Differ from State Regulators?

- Why Do These Differences Matter?

- A Modern Collision: SEC, FINRA, and States Together

- Final Reflection—The SEC Isn’t the Only Watchdog

- FAQs

The Securities and Exchange Commission (SEC) seems like another one of those agencies in the “alphabet soup” that is the federal bureaucracy. Many people have heard of it in passing or in the news. It pops up every now and then after a major corporate scandal or some CEO gets caught lying. Still, fewer people can actually describe the SEC’s unique role in that “alphabet soup” and what it does to protect investors.

What, then, is the SEC? How does it regulate securities fraud? How is it different from (or similar to) the other securities watchdogs, like FINRA and the state securities regulators? The lines overlap, sometimes confusingly. But they matter. Understanding who watches what tells you where enforcement comes from, and where gaps still exist.

Where Did the Securities and Exchange Commission Come From?

The SEC was born from crisis. Congress passed the Securities Act of 1933 and the Securities Exchange Act of 1934 to respond to financial destruction the country experienced during the 1929 market crash and the Great Depression. Congress established the SEC in 1934 to enforce those new rules and restore public confidence in the capital markets.

The SEC's goal core mission is “protecting investors, maintaining fair, orderly and efficient markets, and facilitating capital formation.” On a daily basis, those tasks mean the SEC monitors over trillions of dollars in stock market trading, oversees thousands of public companies, and protects millions of market participants. It does all this while also balancing the tension between market innovation and investor safety.

How is the SEC Organized?

The SEC is headed by five commissioners appointed by the President (with Senate "advice and consent"). The President appoints one commissioner as Chairman -- currently, that's Paul S. Atkins. SEC commissioners serve five year terms and they have staggered terms, meaning that there's always an "experienced" commissioner on the SEC as new ones come on board. No more than three commissioners can belong to the same political party. Forbidding the entire commission from being controlled by the same political party ensures it remains non-partisan.

The Commission has six divisions, each responsible for a different aspect of enforcing the SEC rules and regulations. The divisions are: Corporate Finance; Economic and Risk Analysis; Enforcement; Examinations; Investment Management; Trading and Markets.

The Commission maintains 10 regional offices located in major cities throughout the country.

What are the SEC’s Tools Against Fraud?

The SEC is the federal government’s primary securities law enforcer. The SEC's Enforcement Division investigates allegations ranging from insider trading to accounting fraud to market manipulation. It enforces SEC regulations and federal securities laws. The Division has subpoena power, can compel testimony, and can bring cases either in its own administrative proceedings or in federal court.

The SEC can:

- Freeze assets

- Seek injunctions to stop ongoing fraud

- Impose civil monetary penalties

- Bar individuals from serving as officers or directors of public companies

- Refer criminal cases to the U.S. Department of Justice

One of the SEC’s most important weapons is Rule 10b-5. That rule forbids fraud on the securities market. That means companies can’t mislead investors or make materially misleading statements in connection with the purchase or sale of securities. Most securities fraud class actions filed by private investors piggyback off this standard, but the SEC enforces it directly.

And unlike private litigants, the SEC doesn’t need to prove investors relied on the misstatement to bring an enforcement case. Its focus is on market integrity, not individual damages.

What are some Famous SEC Cases: When Enforcement Hits

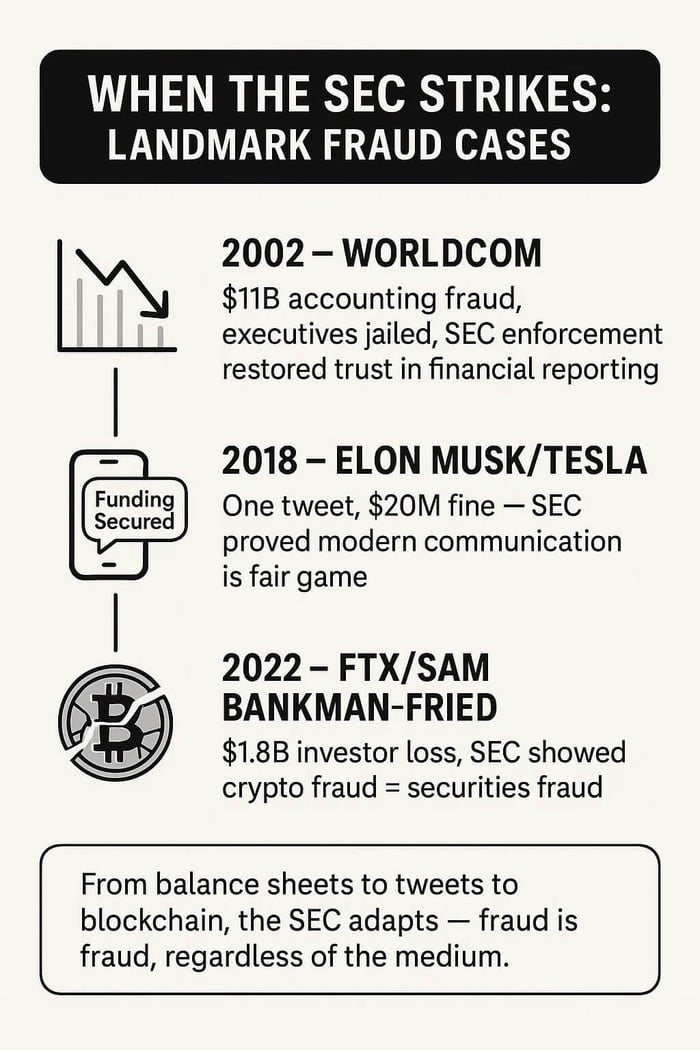

1. SEC v. WorldCom, Inc. (2002)

WorldCom was one of the largest accounting frauds in U.S. history. At its peak, WorldCom was a telecom giant valued at over $100 billion. But by 2002, the façade crumbled when the company admitted it had overstated assets by more than $11 billion through improper accounting entries.

The SEC moved quickly, charging WorldCom with securities fraud in SEC v. WorldCom, Inc., 273 F. Supp 2d. 431 (S.D.N.Y. 2003). The case illustrated how accounting manipulations—things buried in the balance sheets—could ripple out into systemic harm for millions of investors. WorldCom stock, once a mainstay in retirement portfolios, became worthless.

What mattered legally was the scale and intentionality. Executives directed accounting staff to reclassify ordinary expenses as capital investments, inflating profits and hiding losses. It wasn’t a mistake. It was deliberate misrepresentation, signed off in SEC filings and echoed in earnings calls.

The SEC’s enforcement action ran alongside bankruptcy proceedings and criminal indictments. CEO Bernard Ebbers was eventually convicted of fraud and conspiracy. For the SEC, the case was proof of concept: that it could expose not just market manipulation at the margins, but systemic accounting fraud at the core of a Fortune 500 company.

Takeaway: WorldCom reinforced the SEC’s role as a market stabilizer. When investors can’t trust a company’s financial statements, the entire system falters. The SEC’s enforcement gave at least some measure of accountability—and a roadmap for future corporate fraud cases.

2. SEC v. Elon Musk and Tesla, Inc. (2018)

On August 7, 2018, Elon Musk tweeted: “Am considering taking Tesla private at $420. Funding secured.” Those two words—“funding secured”—set off a firestorm. Tesla’s stock price surged more than 10 percent. Analysts scrambled. Investors speculated about a buyout.

But there was a problem. According to the SEC, the funding wasn’t secured at all. Musk had chatted with Saudi Arabia’s sovereign wealth fund. But there weren’t binding agreements, there wasn’t board approval, and there wasn’t set-in-stone financing. The SEC said Musk’s tweet was false and misleading, and thus breached Rule 10b-5. The case was heard in a New York federal court, SEC v. Elon Musk, Case No. 18-cv-8865 (S.D.N.Y. 2018).

The case was as much about tone as substance. Musk argued the tweet was aspirational, not literal. The SEC countered that markets can’t function if CEOs can toss out half-baked statements on social media that move billions in market capitalization. The court didn’t need to reach trial—the case settled quickly. Musk and Tesla each paid $20 million in fines. Musk stepped down as Tesla’s chairman for three years, though he remained CEO.

What made the case striking was its modernity. A single tweet—not a press release, not an SEC filing—triggered securities fraud charges. It showed that the SEC wasn’t confined to old channels of disclosure. Anywhere material information moves markets, the SEC can intervene.

Takeaway: The Musk case signaled to every executive: your communications matter. Whether it’s a conference call, a filing, or 280 characters on Twitter, misleading statements can invite SEC enforcement. The medium doesn’t excuse the message.

3. SEC v. Samuel Bankman-Fried (FTX) (2022)

When the FTX crypto collapsed in November 2022, the world felt the impact. The cryptocurrency exchange (once valued at $32 billion) imploded just days after shocking revelations showed the firm misused customers’ assets.

The SEC slammed FTX founder Sam Bankman-Fried, charging him with securities fraud (SEC v. Samuel Bankman-Fried, No. 1:22-cv-10501, S.D.N.Y. 2022). The SEC said Bankman-Fried raised over $1.8 billion from investors. He boasted FTX was a safe, innovative platform. Meanwhile, he secretly siphoned off customers’ funds into his hedge fund, leaving investors to foot the bill for his fraud. Billions were stolen for risky bets, political donations, and personal purchases – all while FTX said investors’ accounts were safe.

This was classic securities fraud in a new wrapper: false statements, omissions, misuse of funds, concealed risk, and a crypto focus. The fact that it happened in a market often seen as unregulated didn’t shield it from SEC jurisdiction. The agency applied the same basic principle it had used since the 1930s: if you raise money from investors with promises of returns, and you lie about it, the SEC has authority to act.

The FTX collapse underscores the coordination that frequently happens between regulators. The SEC worked alongside the DOJ and the Commodity Futures Trading Commission (CFTC). State regulators weighed in, too, pursuing actions against local promoters of FTX products under their Blue Sky laws. The case showed how, when the fraud is massive enough, every level of enforcement comes into play.

Takeaway: FTX reinforced that securities law is technology neutral. Fraud is fraud. Whether the product is a telecom bond, a share of stock, or a digital token, the law is looking. The SEC’s willingness to charge Bankman-Fried sent a message: crypto isn’t beyond the reach of federal securities law.

How Do SEC Fines and Settlements Help Investors?

When the SEC fines a company, does the money go to investors?

Not always. Civil penalties often go to the U.S. Treasury. But when investors have been directly harmed, the SEC can create “Fair Funds” under the Sarbanes-Oxley Act of 2002. A Fair Fund allows penalties and disgorged profits to be pooled and distributed to eligible investors.

What’s the legal basis for Fair Funds?

SOX Section 308(a) (codified at 15 U.S.C. § 7246(a)) allows civil penalties to be added to disgorgement funds “for the benefit of victims.” This is an exception to the usual rule that penalties go to the Treasury.

What is disgorgement?

Disgorgement is the repayment of ill-gotten gains. If a company or executive profited from fraud, the SEC can force them to return those profits. Disgorged funds can then be returned to investors through court-approved distribution plans.

What about settlements?

Most SEC cases resolve through settlements. In those cases, the defendant may agree to pay a mix of penalties, disgorgement, and prejudgment interest. If a Fair Fund is created, those dollars go back to harmed investors instead of just disappearing into the Treasury.

How do investors actually get paid?

The SEC appoints a distribution agent to identify harmed investors, calculate eligible losses, and send payments. Investors usually don’t need to file suit themselves. Sometimes claim forms are required, other times payments are automatic if records are available.

Does every SEC action result in investor payments?

No. If the misconduct didn’t directly harm investors — or if the amount collected is too small to distribute — the money may not flow back. But in major cases, like Enron, WorldCom, or more recently FTX-related proceedings, Fair Funds have been used to return billions.

How long does it take?

Distribution is not fast. Large Fair Funds can take years to administer because investigators have to reconstruct trades, verify losses, and weed out duplicate or fraudulent claims.

What if investors also file class actions?

It can happen in parallel. Investors might recover through a private securities class action settlement and also through an SEC Fair Fund. The two systems are separate, but both are designed to push restitution back to those who were misled.

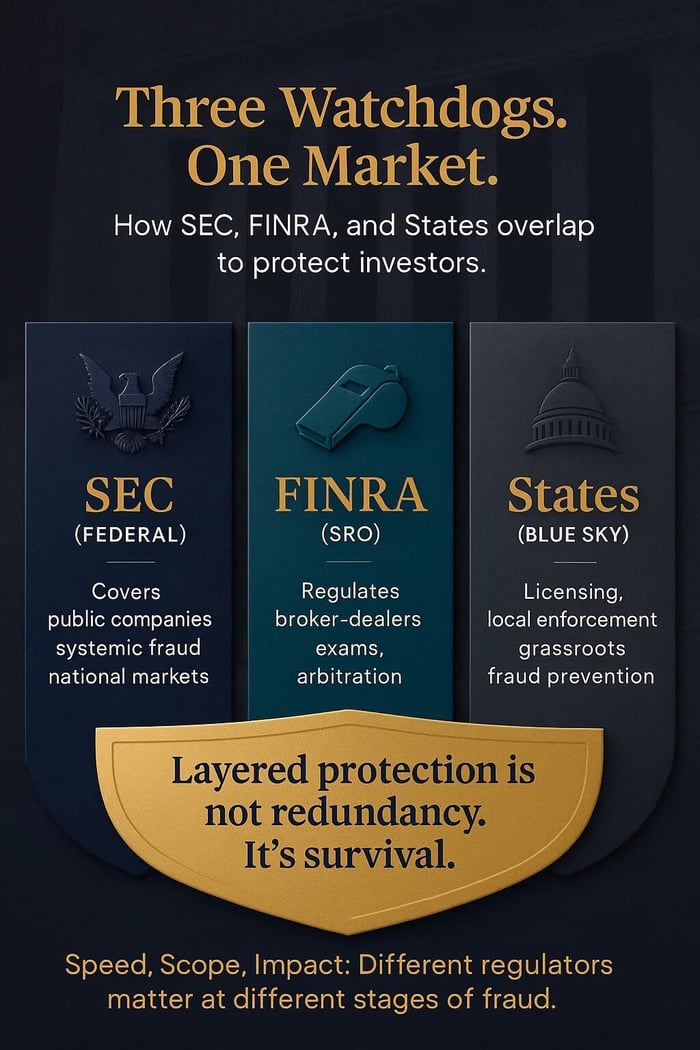

How Does the SEC Differ from FINRA?

It’s easy to lump the SEC and FINRA together—they both regulate parts of the securities industry. But they’re not the same.

- SEC: A federal government agency. It enforces federal securities laws. Its jurisdiction covers public companies, securities markets, and investment advisers. It has the power to make rules, bring enforcement actions, and coordinate with the DOJ.

- FINRA: The Financial Industry Regulatory Authority is self-regulatory organization (SRO). That is, it is the financial industry doing some self-policing. FINRA oversees broker-dealers and their registered representatives. It does things like drafting rules for brokers, running broker exams, conducting audits of financial institutions, and administering arbitration forums for customer disputes.

In practice, the SEC supervises FINRA. FINRA enforces day-to-day conduct for brokers. But the SEC can (and sometimes does) overrule it. The SEC also handles matters FINRA doesn’t touch, like public company disclosure, insider trading, and systemic fraud.

Think of FINRA as the referee for brokers on the ground, while the SEC acts as the federal court of appeals—and the cop.

How Does the SEC Differ from State Regulators?

State securities regulators enforce Blue Sky laws. Those state laws are often older than SEC but still form the backbone of day-to-day securities laws enforcement in the U.S. State regulators do a number of important things. They license brokers and investment advisers locally, review certain offerings, and police fraud at the state level.

So, the SEC might pursue billion-dollar accounting fraud at a public company. A state regulator may shut down a fraudulent promissory-note scheme in that state. The SEC is more big picture, targeting national markets. States (naturally) focus on their own residents.

Crucially, the laws overlap. A fraudster can face both SEC action and state enforcement. And sometimes states move first, catching misconduct before it scales.

Why Do These Differences Matter?

To investors, the differences can feel academic. Fraud is fraud. But the enforcement landscape matters because it affects speed, scope, and impact.

- Speed: States often move faster—they can issue cease-and-desist orders quickly. The SEC, with more process, takes longer.

- Scope: The SEC focuses on public markets and systemic risk. States often handle localized fraud. FINRA, meanwhile, lives in the middle—regulating broker conduct.

- Impact: SEC actions carry nationwide weight, with penalties that ripple through markets. State actions protect smaller pools of investors but can be life-changing locally. FINRA keeps brokers in line but rarely makes national news.

Together, they form a layered defense. No single regulator covers everything, but their combined authority gives investors multiple lines of protection.

A Modern Collision: SEC, FINRA, and States Together

The crypto sector offers a modern example of how these regulators overlap.

- The SEC sues major platforms for offering unregistered securities.

- State regulators bring their own claims under Blue Sky statutes, sometimes even when federal courts dismiss parts of the SEC’s cases.

- FINRA issues guidance on how broker-dealers can handle digital asset securities.

The result is a patchwork—but an intentional one. Fraud in new markets doesn’t fall neatly into one regulator’s lap. It gets tackled on multiple fronts.

Final Reflection—The SEC Isn’t the Only Watchdog

The SEC is the centerpiece of U.S. securities regulation. It enforces federal law, investigates fraud, and brings landmark cases that ripple across markets. But it doesn’t work alone. FINRA patrols the broker-dealer world. State regulators operate closer to the ground.

The lines blur, sometimes uncomfortably. But that’s the design. When one regulator misses something—or chooses not to act—another can step in.

For investors, the takeaway is simple: there isn’t just one watchdog. There are layers. And in a system where fraud still finds its way in, those overlapping roles aren’t redundancy. They’re survival.

You Can Also Read |

FAQs

Who funds the SEC?

The SEC is funded by Congress, but much of its budget is offset by transaction and registration fees paid by public companies and market participants.

Can the SEC bring criminal charges?

No. The SEC's authority only lets it bring civil and administrative proceedings via the SEC's Division of Enforcement. For criminal charges, it refers matters to the Department of Justice.

What role does the SEC play in IPOs?

The SEC reviews registration statements for initial public offerings (IPOs) under the Securities Act of 1933. It ensures disclosures are complete and accurate, but does not endorse the investment.

Does the SEC regulate investment advisers?

Yes. Under the Investment Advisers Act of 1940, the SEC regulates advisers with more than $110 million in assets under management.

How does the SEC protect whistleblowers?

The SEC’s whistleblower program offers confidentiality, anti-retaliation protections, and potential financial awards of 10–30% of monetary sanctions collected.

How do investors report fraud to the SEC?

Investors can submit tips and complaints through the SEC’s online portal, accessible at sec.gov.

![RxSight, Inc. (RXST) Securities Class Action Lawsuit Update [September 03, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/rxsight-securities-lawsuit-blog-banner.webp)

![Replimune Group, Inc. (REPL) Securities Class Action Lawsuit [September 8, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/replimune-securities-lawsuit-blog-banner-v2.webp)

![Alto Neuroscience, Inc. (ANRO) Securities Class Action Lawsuit [September 02, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/altoneuroscience-securities-lawsuit-blog-banner.webp)