![Savara Inc. (SVRA) Securities Class Action Lawsuit Update [January 5, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/svra-alert-plus-banner.webp)

Inside the Molbreevi FDA Refusal-to-File Shock

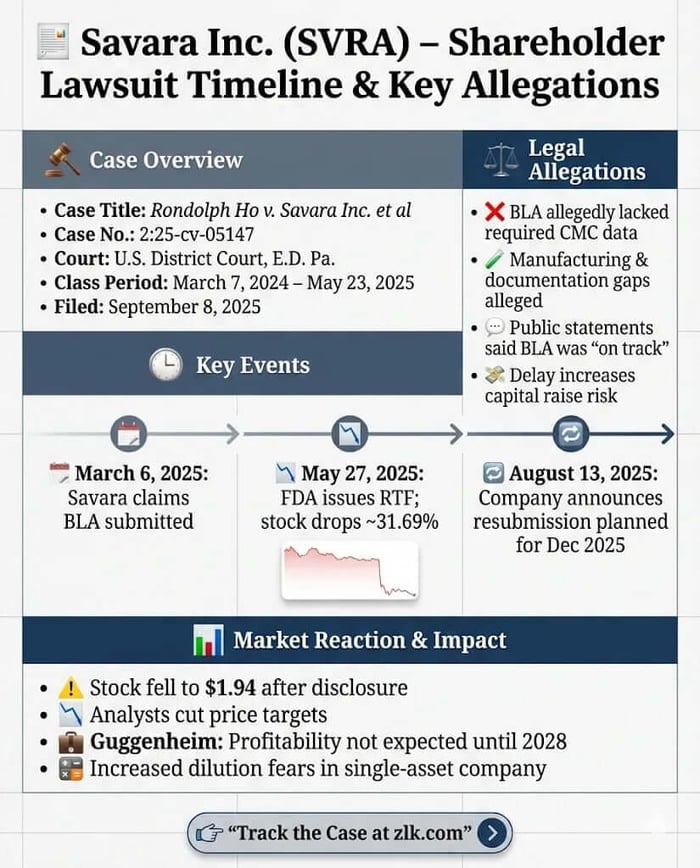

Caption: Ho v. Savara Inc. et al.

Case No.: 2:25-cv-05147

Jurisdiction: U.S. District Court, Eastern District of Pennsylvania

Filed on: September 8, 2025

Class Period: March 7, 2024–May 23, 2025

Introduction

Savara said it was on track. The FDA said the application was not ready.

A federal securities class action filed in the Eastern District of Pennsylvania accuses Savara Inc. (NASDAQ: SVRA) and two senior executives of misleading investors about the readiness of the company’s Biologics License Application for MOLBREEVI (molgramostim) and the downstream capital consequences of a regulatory delay.

The case is Ho v. Savara Inc., Matthew Pauls, and David Lowrance, filed as Case No. 2:25-cv-05147 in the U.S. District Court for the Eastern District of Pennsylvania. Plaintiff Rondolph Ho seeks to represent investors who purchased Savara securities from March 7, 2024 through May 23, 2025 (the “Class Period”).

The alleged core failure is not a clinical miss. It is paperwork, manufacturing detail, and regulatory sequencing—specifically whether Savara’s MOLBREEVI BLA included enough chemistry, manufacturing, and controls (CMC) information to be accepted for review. Investors allege it did not, and that the gap was disguised behind confident timelines and runway talk.

The trigger event was blunt. On May 27, 2025, Savara disclosed the FDA issued a Refusal-to-File (RTF) letter because the BLA was “not sufficiently complete” and the agency requested additional CMC data. The stock dropped about 31.69% that day, closing at $1.94.

For investors, this is the familiar biotech risk in a different costume: not “does the drug work,” but “can the company clear the gate that lets the FDA even start reading.”

“Most SVRA shareholders never file or join the class action, which means they miss out on potential recovery funds,” said Attorney Joe Levi.

Backdrop and Business Context

Savara is a clinical-stage biopharmaceutical company focused on rare respiratory diseases, with its investment thesis concentrated in one lead asset: MOLBREEVI (molgramostim), an inhaled GM-CSF therapy being developed for autoimmune pulmonary alveolar proteinosis (aPAP).

The company’s story, as framed in public communications cited in the complaint, leaned heavily on momentum: Phase 3 execution, disease-awareness efforts, and a market opportunity narrative. One quoted company statement pointed to an analysis identifying “~3,600 currently diagnosed aPAP patients” in the U.S., coupled with a promise that the program could “fundamentally change the way aPAP is treated.”

But in biologics, the story is never only clinical. It is also industrial. A BLA lives or dies on whether manufacturing is reproducible, validated, and documented—down to stability testing and analytical method validation. The complaint underscores that the CMC section must provide a detailed account of manufacturing process validation, stability testing, analytical method validation, and quality controls.

That distinction matters because an RTF is not the FDA saying “no.” It is the FDA saying “we are not even opening the file.” Fierce Pharma captured the practical impact: an RTF means the FDA “has declined to evaluate” the application as submitted, even if safety and efficacy are not the issue.

Promises Made vs. Reality

The Promises:

Across the Class Period, Savara repeatedly described a tight regulatory schedule—rolling submission initiated, completion targeted, and an implied near-term approval path. The complaint cites multiple company statements projecting that Savara would complete the rolling BLA by the end of 1Q 2025. It also quotes language around the BLA as a milestone, with management describing it as “on track” and tied to launch preparations.

Separately, Savara’s SEC filings framed the regulatory process in a way that, in hindsight, reads like a quiet warning label: the company explained that a BLA must include “detailed information” about “chemistry, manufacturing, [and] controls,” and that the FDA “may refuse to file” an application it deems incomplete—requiring resubmission.

The Reality:

Investors allege that, throughout this period, the MOLBREEVI BLA lacked sufficient CMC information, making FDA acceptance and timely completion unlikely. The alleged consequence chain is simple and grim: incomplete CMC → RTF → delayed review and launch → increased need for capital.

The May 27 disclosure supplied the missing piece in plain English. Savara said the FDA determined the BLA was not complete enough for substantive review and requested additional CMC data. And the market treated that as what it was: a major schedule break.

Timeline of Alleged Misconduct and Disclosures

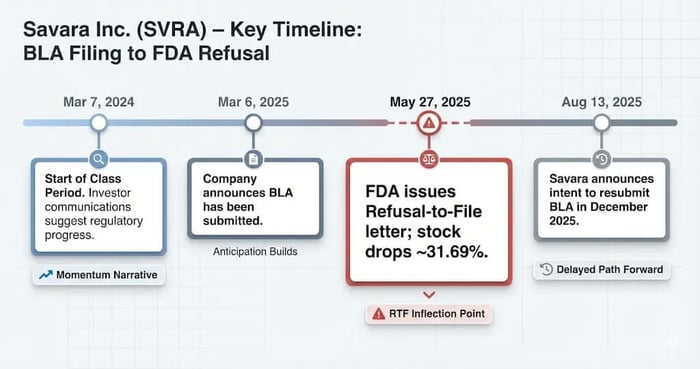

March 7, 2024 (start of Class Period): The complaint anchors the start date to Savara’s annual reporting cycle and public communications that positioned the program as advancing toward pivotal milestones.

Late 2024 into early 2025: Savara publicly discussed initiating and completing a rolling BLA submission on a near-term schedule, repeatedly pointing investors toward end of 1Q 2025 for completion.

March 6, 2025: Savara represented the BLA had been submitted, with messaging tied to “priority review” hopes and launch planning (as summarized in the complaint).

May 27, 2025 (corrective disclosure): Savara announced the FDA issued an RTF letter, stating the BLA was “not sufficiently complete” and requesting additional CMC data. Fierce Pharma reported the FDA did not flag safety concerns or request new efficacy studies, reinforcing that manufacturing documentation—not clinical outcomes—was the blocker. Savara’s stock fell $0.90, or 31.69%, to close at $1.94.

August 13, 2025 (post-class development): Savara later disclosed it planned to resubmit the BLA in December 2025, a timeline shift that, in investor framing, confirmed the delay was not a quick fix.

Investor Harm and Market Reaction

Loss causation in biotech cases often turns on whether the disclosure is truly “new” or merely a risk finally materializing. Here, the complaint’s harm theory ties investor losses to a discrete event: the RTF announcement and the immediate price collapse.

The market reaction was violent because the disclosure re-priced multiple assumptions at once:

Regulatory timing: an RTF resets the clock before a review clock even starts.

Manufacturing readiness: “additional CMC data” signals work still needed to make the filing reviewable.

Financing risk: delays in a single-asset company tend to surface dilution fears.

Analysts explicitly connected those dots in contemporaneous commentary cited in the complaint: Guggenheim reportedly reduced its price target and stated it did not expect Savara to be profitable “until 2028” and expected the company “may raise additional capital,” potentially through a secondary offering.

That framing matters because it translates regulatory delay into shareholder math.

Litigation and Procedural Posture

The complaint asserts claims under Section 10(b) and Rule 10b-5, and seeks control-person liability under Section 20(a) against the individual defendants.

The named executives are Matthew Pauls (CEO/Chairman) and David Lowrance (CFO/CAO/Secretary).

The alleged misstatements and omissions focus on five linked assertions: that the BLA lacked sufficient CMC information, that approval was unlikely “in its current form,” that Savara’s projected submission timeline was not achievable, that the delay increased the likelihood of a capital raise, and that public statements were therefore misleading.

On scienter, the complaint pleads motive-and-opportunity and knowledge/control arguments typical in Exchange Act cases, arguing senior officers controlled and certified filings while allegedly possessing information about the true state of readiness.

This is still early-stage litigation. The next inflection point, as in most securities class actions, will be a motion to dismiss fight over falsity, scienter, and loss causation—especially the defense argument that risks around FDA filing completeness were disclosed, versus the plaintiff argument that the market was sold certainty while the company allegedly knew the application was not “sufficiently complete.”

Shareholder Sentiment

Retail sentiment around biotech catalysts is rarely nuanced. It tends to split into two camps: “this is a fatal sign” versus “this is a fixable delay.”

After the RTF news, that split showed up in the way investors discussed the distinction between a refusal-to-file and a clinical rejection. Media coverage emphasized that the FDA did not cite safety concerns or request additional efficacy studies, which naturally fed the bull thesis that the drug’s clinical profile was intact and the issue was operational. Bears read the same fact differently: if the company could not clear the procedural threshold, what else was being oversold?

Meanwhile, broader social feeds often revert to chart talk once the headline passes. One StockTwits-adjacent dashboard captured the familiar “dip and bounce” posture in an SVRA post: “The 10 at $6.17 looks good after a dip looks to bounce soon.” It is not a legal argument. It is a coping mechanism.

The practical takeaway for fund managers is that sentiment volatility can outpace fundamentals in single-asset names. When the story is one molecule, the crowd treats every regulatory document like a verdict.

Analyst Commentary

Analyst reactions, as summarized in market reporting, clustered around two themes: (1) the issue appears CMC-focused, not clinical, and (2) timing and dilution risk rise immediately.

A TipRanks recap described a mixed response: Oppenheimer maintained an Outperform, emphasizing Phase 3 strength and the absence of safety or efficacy concerns, while H.C. Wainwright downgraded to Neutral amid uncertainty in the approval path. The same recap noted Evercore ISI and Guggenheim lowered price targets, with Evercore pointing to CMC issues and a potential launch pushed to 2027, and Wells Fargo also reducing its target while still stressing the RTF was not safety-related.

The complaint itself highlights Guggenheim’s posture as explicitly capital-focused, pointing to expectations of continued losses and the prospect of a secondary offering that could dilute existing holders.

In plain terms: Wall Street did what it usually does after a regulatory schedule break. It priced time, then priced cash.

SEC Filings & Risk Factors

One uncomfortable feature of many securities class actions is that the “truth” can often be found—quietly—in risk-factor language long before it detonates in a headline.

Savara’s SEC filings describe, with clinical precision, what a BLA must contain: “detailed information” relating to a product’s “chemistry, manufacturing, [and] controls.” The filing also states the FDA reviews a BLA shortly after submission to determine if it is “substantially complete,” and that the agency “may refuse to file” an application it deems incomplete—requiring resubmission with additional information.

That disclosure is the defense’s natural oxygen: investors were warned about the procedural risk. But plaintiffs will argue the lawsuit is not about whether a refusal-to-file is theoretically possible. It is about whether the company, while projecting confidence and timelines, allegedly failed to disclose that the application in fact “lacked sufficient” CMC information—turning a generic risk into a known problem.

Savara’s later quarterly reporting also indicates meaningful spend tied to CMC workstreams (including efforts to establish additional manufacturing), underscoring how operationally central manufacturing readiness is to the program’s value.

In a case like this, the SEC filing record is not just background. It is the battleground: risk disclosure versus alleged omission, cautionary language versus alleged certainty.

Conclusion: Implications for Investors

The Savara (SVRA) securities class action is a reminder that biotech risk is not only science. It is process. Validation runs. Documentation. The unglamorous machinery behind a molecule.

For investors, the red flags are structural and widely portable across development-stage biopharma: a single-asset valuation, tightly choreographed regulatory timelines, and repeated runway assurances that assume the clock will behave. When the FDA refuses to file, the clock does not merely slow down. It restarts.

Two broader lessons tend to surface in cases like this.

First, “risk factor” is not the same as “known issue.” Courts often ask whether the market was warned in the abstract, or whether management allegedly knew the problem had already arrived. Second, manufacturing readiness is material in biologics in a way retail investors routinely underestimate—until an RTF forces everyone to learn the acronym.

This isn’t a closing argument. It’s a snapshot of what investors say happened, what the public record shows, and what the next phase of litigation will likely test. Now, investors are fighting back.

How to Join the Savara Inc. (SVRA) Class Action

Confirm you purchased SVRA shares during the relevant period

Review eligibility details

Click here to check eligibility: https://zlk.com/learn/savara-inc-svra-securities-class-action-lawsuit?wire=54

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Smart Digital Group Limited (SDM) Securities Class Action Lawsuit Update [January 19, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/sdm-alert-plus-banner.webp)

![Dow Inc. (DOW) Securities Class Action Lawsuit Update [December 26, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/dow-alert-plus-banner.webp)

![Vistagen Therapeutics, Inc. (VTGN) Securities Class Action Lawsuit Update [January 19, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/vtgn-alert-plus-banner.webp)