![Smart Digital Group Limited (SDM) Securities Class Action Lawsuit Update [January 19, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/sdm-alert-plus-banner.webp)

Inside the IPO, the Run-Up, and the Collapse

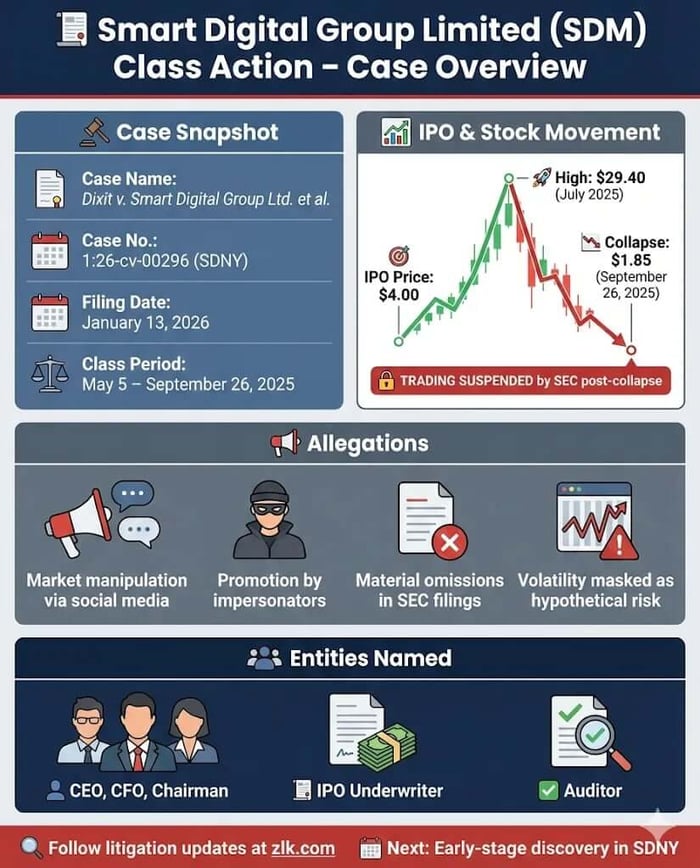

Case Name: Dixit v. Smart Digital Group Limited et al.

Case No.: 1:26-cv-00296

Jurisdiction: U.S. District Court, Southern District of New York

Filed on: January 13, 2026

Class Period: May 5, 2025 – September 26, 2025

Introduction

Smart Digital Group Limited did not stumble quietly. According to the complaint, it surged, spiked, and then imploded—taking retail investors with it. In January 2026, a federal securities class action was filed in the Southern District of New York alleging that Smart Digital Group Limited and its executives sold the market a company narrative while its stock traded inside a manipulated reality.

According to the complaint, the case centers on a low-float initial public offering (“IPO”) followed by an extraordinary post-offering price run-up that occurred despite the absence of any corresponding business announcements or fundamental developments disclosed by the Company. The complaint alleges that the stock ultimately collapsed on September 26, 2025, declining more than 86% from the prior trading day’s close during a single trading session. When regulators intervened, trading stopped. It has not resumed.

Now, investors are asking a narrower question than whether the stock was volatile. They are asking whether the risk was hidden in plain sight.

“Most SDM shareholders never file or join the class action, which means they miss out on potential recovery funds,” said Attorney Joe Levi.

Backdrop and Business Context

Smart Digital Group Limited is a Cayman Islands holding company whose operating entities are based in Singapore, Macau, and mainland China. Through those subsidiaries, the company reported providing event planning, internet media marketing, software customization, and business consulting services.

The company completed its initial public offering on May 5, 2025, selling 1.5 million ordinary shares at $4.00 per share and raising approximately $6 million in gross proceeds. The Company’s public float was limited. As alleged, this relatively small float meant that even modest trading activity could result in significant price volatility.

For months after the IPO, Smart Digital’s filings painted a picture of revenue growth, stable customer relationships, and strategic focus. What they did not disclose, plaintiffs allege, was that the company’s stock had become the target of a coordinated promotional campaign operating outside the company’s public disclosures.

Promises Made vs. Reality

In its IPO prospectus, Smart Digital emphasized growth, operational strength, and management experience. The company highlighted revenue growth of more than 120 percent year over year and described its ability to retain customers and execute strategy across Asian markets.

As alleged in the complaint, risk disclosures acknowledged the possibility of stock volatility, but only with generic boilerplate risk disclosures. The warnings described hypothetical price swings “seemingly unrelated” to fundamentals—language plaintiffs argue rang hollow once the volatility arrived not as a possibility, but as an unfolding event.

According to the complaint, while the company was assuring investors that no material subsequent events required disclosure, stock promoters were flooding messaging apps and social-media platforms with false claims. These included fabricated partnerships, exaggerated growth projections, and price targets reaching as high as $55 per share. Investors were allegedly urged to send screenshots confirming their purchases.

The contrast is central to the case: public filings spoke in generalities, while private channels drove urgency.

Timeline of Alleged Misconduct and Disclosures

The alleged scheme unfolded quickly. After the May 2025 IPO, Smart Digital’s stock began rising sharply in June, accompanied by sudden and unexplained spikes in trading volume. By late July, the shares reached an intraday high of $29.40—more than seven times the offering price—despite no corresponding business announcements.

In August, the stock fell back toward $10, again without disclosure explaining either the rise or the decline. Then, in September, the company issued a series of filings and press releases, including financial updates and announcements about establishing a “diversified cryptocurrency asset pool.” Each disclosure coincided with renewed upward pressure on the stock.

On September 26, 2025, minutes after the market opened, trading was halted for volatility. When it resumed, the stock collapsed, closing at $1.85 per share on record volume. Within days, the SEC suspended trading entirely, citing potential market manipulation carried out through social-media recommendations by unknown persons. NASDAQ later extended the suspension pending further information. Trading has remained halted.

Investor Harm and Market Reaction

The losses were immediate and severe. On the September 26 collapse alone, Smart Digital shares lost approximately eighty-eight percent of their value from the prior close. Investors who purchased during the promotional run-up were effectively trapped once trading was suspended.

Unlike gradual declines tied to earnings or guidance revisions, the harm here was compressed into a single morning. Liquidity vanished. Exit options disappeared. What remained was a frozen position and an unresolved regulatory process.

The complaint frames this not as ordinary market risk, but as loss causation tied directly to the revelation that the trading environment itself had been distorted.

Litigation and Procedural Posture

The action, filed under Sections 10(b) and 20(a) of the Securities Exchange Act and Rule 10b-5, names the company, its CEO, CFO, and chairman, along with its auditor and IPO underwriter. Plaintiffs allege material misstatements and omissions, control-person liability, and a failure to disclose known risks tied to manipulation and trading halts.

Scienter allegations focus on the timing of filings, the nature of the stock’s price movements, the small public float, and the defendants’ alleged access to information about abnormal trading activity. The case is in its early stages, with discovery likely to focus on communications, account relationships, and coordination between promoters and insiders.

Shareholder Sentiment

Retail investor sentiment on Smart Digital Group shifted rapidly from speculative enthusiasm to frustration following the sudden trading halt. Prior to the collapse, online discussion boards and social media platforms were active with bullish sentiment.

However, following the September 26 halt and subsequent SEC suspension order, confusion dominated retail channels. Investors on platforms like Investing.com and Public.com reported being trapped in positions with no ability to liquidate, as the stock remained "frozen" at $1.85. The lack of communication from the company was a primary grievance, with users comparing the situation to other recent halts in the sector.

Analyst Commentary

Institutional coverage of Smart Digital Group was virtually nonexistent, a common trait for micro-cap foreign issuers that often leaves retail investors relying on unregulated information sources. In the absence of traditional sell-side research, financial news outlets like Benzinga filled the void by reporting on the regulatory actions rather than fundamental valuation.

Following the collapse, market commentators quickly linked SDM’s trajectory to a broader pattern of "pump-and-dump" schemes involving Cayman-incorporated entities. Financial media highlighted the parallel suspension of QMMM Holdings and the indictment of executives at Ostin Technology Group, noting that these companies shared similar "low float" structures and aggressive social media promotion.

Analysts have since cited the SDM case as a primary example of why NASDAQ has begun implementing stricter scrutiny on initial listings for companies with limited operating history in restricted markets.

SEC Filings & Risk Factors

Smart Digital’s SEC filings acknowledged volatility risk, but plaintiffs argue those disclosures were generic and failed to address risks that had already materialized. The prospectus warned that stocks with similar floats had experienced extreme swings, yet did not disclose that Smart Digital’s own stock was allegedly being promoted through impersonation and misinformation.

Later filings stated that no subsequent events required disclosure, even as trading volumes surged. When the SEC finally suspended trading, the company disclosed the halt only after the fact, while denying involvement in manipulation. The lawsuit contends that this sequence illustrates a gap between disclosure obligations and disclosure practice.

Conclusion: Implications for Investors

The Smart Digital case is not about hindsight. It is about timing. Investors are not alleging that volatility alone was wrongful, but that the conditions producing that volatility were concealed while the market was still buying.

For investors, the lesson is structural as much as substantive. Low-float IPOs, thin coverage, and cross-border operations amplify risk when disclosure lags reality. For regulators and counsel, the case underscores how quickly promotional ecosystems can outpace formal filings.

This is not a closing argument. It is a warning signal.

How to Join the Smart Digital Group Limited (SDM) Class Action

Confirm you purchased SDM shares during the relevant period

Review eligibility details

Click here to check eligibility: https://zlk.com/pslra-1/smart-digital-group-limited-lawsuit-submission-form?wire=54

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Savara Inc. (SVRA) Securities Class Action Lawsuit Update [January 5, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/svra-alert-plus-banner.webp)

![Dow Inc. (DOW) Securities Class Action Lawsuit Update [December 26, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/dow-alert-plus-banner.webp)

![Vistagen Therapeutics, Inc. (VTGN) Securities Class Action Lawsuit Update [January 19, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/vtgn-alert-plus-banner.webp)