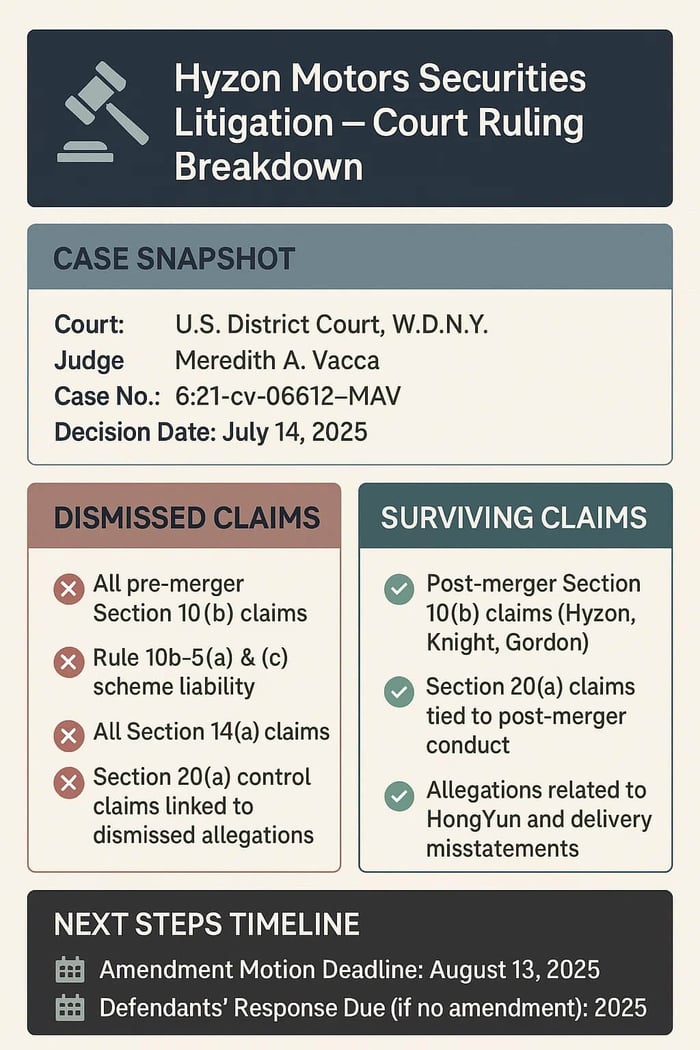

United States District Court, Western District of New York

Case No. 6:21-cv-06612-MAV

Judge Meredith A. Vacca**

Summary

On July 14, 2025, the U.S. District Court for the Western District of New York issued a mixed ruling on motions to dismiss in *In re Hyzon Motors Inc. Securities Litigation*. The Court dismissed the bulk of claims in the Third Amended Complaint (TAC), including all pre-merger Section 10(b) claims, all scheme liability claims under Rule 10b-5(a) and (c), all Section 14(a) claims, and the related Section 20(a) control person claims. These dismissals were based on findings of lack of standing, non-actionable statements, and insufficient pleading under the PSLRA and Rule 9(b). However, select post-merger claims under Section 10(b) and 20(a) were allowed to proceed against Hyzon, its former CEO Craig Knight, and former CFO Mark Gordon. The Court granted plaintiff leave to move to amend the complaint, citing developments in a related SEC action.

The Underlying Lawsuit

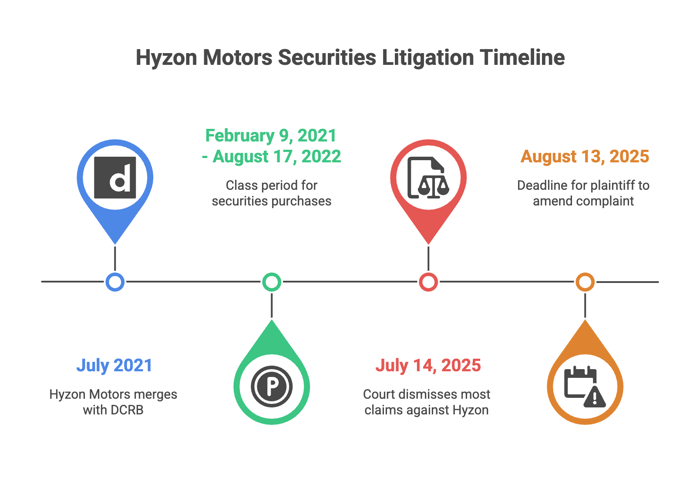

The litigation stems from alleged misstatements made by Hyzon and affiliated executives before and after the company's July 2021 merger with Decarbonization Plus Acquisition Corporation (DCRB). The TAC covers two proposed classes: (1) shareholders who purchased Hyzon securities between February 9, 2021, and August 17, 2022, and (2) DCRB shareholders as of June 1, 2021, in connection with proxy solicitation.

Plaintiff Alfred Miller alleged that Hyzon executives and DCRB affiliates made false or misleading statements about Legacy Hyzon’s hydrogen truck delivery capabilities, revenue projections, and customer pipeline—particularly concerning a deal with Shanghai Hydrogen HongYun. These statements, according to the complaint, misled investors and inflated stock prices until operational shortcomings were disclosed.

Defendants’ Motion to Dismiss

Defendants moved to dismiss the TAC under Rule 12(b)(6). Key arguments included:

- Standing: Plaintiff lacked standing to bring pre-merger Section 10(b) claims because he did not purchase Legacy Hyzon securities.

- Falsity: The challenged statements were vague, forward-looking, or immaterial puffery, especially those made prior to the merger.

- Scienter: The TAC failed to plead a strong inference of intent or recklessness.

- Loss causation: Alleged stock drops were not adequately tied to specific corrective disclosures.

- Scheme liability The complaint failed to allege deceptive conduct beyond the misstatements themselves.

- Section 14(a): Proxy-related statements were accompanied by extensive cautionary language and failed to meet the Rule 9(b) standard.

Plaintiffs’ Opposition

Plaintiff argued that Hyzon’s disclosures, short-seller reports, and an SEC enforcement action corroborated that key statements were materially false. The TAC alleged that Knight and Gordon were aware of operational gaps and exaggerated the company’s readiness. Post-merger representations, particularly concerning HongYun and vehicle functionality, were alleged to have misled investors.

Court’s Ruling

The Court granted the motions in part. All Section 10(b) claims concerning pre-merger statements by Legacy Hyzon, Knight, Gu, and Gordon were dismissed with prejudice, as were all claims under Rule 10b-5(a) and (c), Section 14(a), and related Section 20(a) control claims. However, the Court found that certain post-merger statements plausibly misrepresented Hyzon’s operational and financial status, and allowed those Section 10(b) and 20(a) claims to proceed against Hyzon, Knight, and Gordon.

The Court gave plaintiff until August 13, 2025, to file a motion to amend the complaint in light of the SEC’s findings in a parallel action. Defendants must respond to the surviving claims by the same date if no amendment is made.

Court’s Rationale

Falsity

The Court held that plaintiff lacked standing to assert pre-merger 10(b) claims, relying on *Frutarom* and its progeny. It also found that pre-merger statements by DCRB executives, including revenue projections, were either forward-looking or non-actionable puffery. However, post-merger statements about Hyzon’s customer pipeline and vehicle readiness, particularly regarding HongYun, were sufficiently specific to survive dismissal.

Scienter

The Court found scienter was not adequately pled as to Tichio, Anderson, or Haskopoulos. But allegations against Knight and Gordon—including their roles in public statements and internal awareness of Hyzon’s delivery issues—supported a strong inference of scienter that could be imputed to Hyzon.

Loss Causation

The Court found that loss causation was adequately pled for the surviving claims, noting that price drops following public disclosures, including a 28% decline after the Blue Orca report, were sufficiently alleged to be tied to revelations of operational deficiencies.

Scheme Liability

The Court dismissed all scheme liability claims, finding no actionable misconduct beyond the misstatements themselves. Allegations of a "sham media blitz" were not supported by specific deceptive acts distinct from the alleged misstatements.

Section 14(a)

The Court found that proxy statements were forward-looking and contained meaningful cautionary language. Plaintiff failed to plead any material omissions with the specificity required by Rule 9(b), and thus the Section 14(a) claims could not proceed.

Final Disposition

Most of the claims were dismissed with prejudice. What remains are narrow claims under Section 10(b) and 20(a) concerning certain post-merger statements. Plaintiff may move to amend the complaint by August 13, 2025. If no amendment is filed, the remaining claims will proceed and defendants must respond by that same date.