![Firefly Aerospace, Inc. (FLY) Securities Class Action Lawsuit Update [November 21, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/fly-alert-plus-banner-image-j88uj.webp)

Investors Allege IPO Masked Operational and Financial Collapse

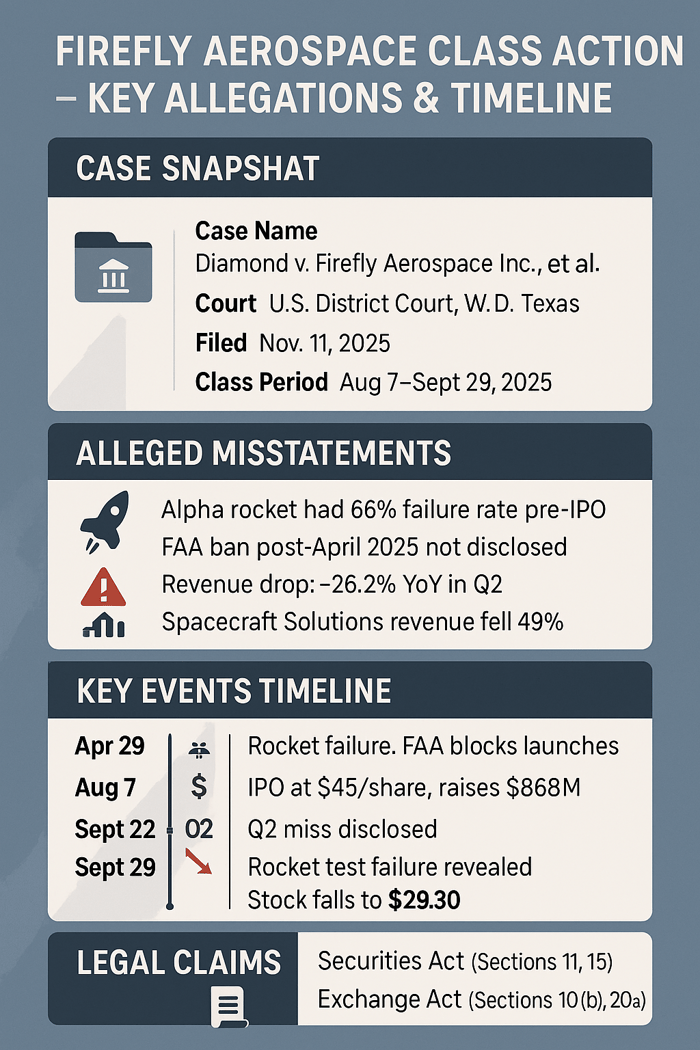

Case Name: Diamond v. Firefly Aerospace Inc., et al.

Case No.: 1:25-cv-01812

Jurisdiction: U.S. District Court, Western District of Texas

Filed on: November 11, 2025

Class Period: August 7, 2025 - September 29, 2025

Introduction

The promise of space exploration is often written in prose, but its reality is tallied in balance sheets and failure rates. For investors in Firefly Aerospace Inc. (FLY), the journey from its highly-anticipated Initial Public Offering (IPO) in August 2025 to a plummeting stock price just weeks later has become a harsh lesson in gravity. This isn’t a closing argument. It’s a reckoning.

Filed in the U.S. District Court for the Western District of Texas, the securities class action lawsuit, Diamond v. Firefly Aerospace Inc. et al. (Case No. 1:25-cv-01812), alleges that the Company and its senior leadership misled investors through materially false and misleading statements contained in the IPO Offering Documents and throughout the Class Period—August 7, 2025, through September 29, 2025. The core allegation is stark: Firefly, a space and defense technology firm, had systematically overstated the commercial viability of its Alpha rocket program and inflated the growth prospects of its Spacecraft Solutions segment.

The truth emerged not in a single catastrophic disclosure, but in two rapid, successive blows: a September 22, 2025, earnings report that missed analyst expectations and revealed a significant revenue decline, followed less than a week later by the announcement of an Alpha Flight 7 rocket failure during a pre-flight test. The stock price, initially priced at $45.00 per share in the IPO, crashed, resulting in significant investor harm and initiating this legal pursuit.

Backdrop and Business Context

Firefly Aerospace purports to provide "mission solutions for national security, government, and commercial customers". It operates through two primary segments: Launch (centered on the Alpha rocket) and Spacecraft Solutions. The company’s investment narrative was built on a bold promise: converting prestigious NASA contracts and a purported $1.1 billion backlog into consistent, rapid revenue growth.

The Company’s journey to the public market culminated in its August 7, 2025, IPO, selling approximately 19.3 million shares at $45.00 per share. This was no quiet launch. It raised $868 million and was one of the largest U.S. space IPOs of the year. For a moment, the stock performed a kind of zero-G float, climbing as much as 56% during its first day of trading. The excitement was palpable, framed by the executive team—including CEO Jason Kim and CFO Darren Ma—who publicly affirmed the company’s strong operational posture and readiness for a high-growth trajectory. The whole point of the IPO was to capitalize on this perception of momentum.

But underneath the glossy prospectus and CEO soundbites, the operational setup was allegedly more fragile. The Alpha rocket, described publicly as "flight proven and commercially available," had a troubling, undisclosed history. The operational reality was one of persistent, severe failures; by the time of the IPO, four of its six attempted flights had ended in failure. This operational deficiency, and its subsequent financial impact on the Spacecraft Solutions revenue, formed the unstable ground upon which the public company was built.

Promises Made vs. Reality

The narrative constructed by Firefly management painted a picture of inexorable growth, driven by a reliable launch schedule and robust Spacecraft Solutions demand. This narrative was cemented in the Offering Documents that facilitated the IPO.

The Public Promise: In the days surrounding the August 2025 IPO, the Company and its leadership emphasized their readiness. CEO Jason Kim, for instance, spoke confidently about the market and operational readiness of Firefly’s vehicles. The IPO filings highlighted the rapid acceleration of the business, stating that Firefly’s revenue had surged to $71M in the first half of 2025, backed by that formidable $1.1 billion backlog.

The Alleged Reality: The foundational promises began to erode just weeks after the IPO.

The Launch Lie: The complaint alleges that the Alpha rocket program was far from operationally ready. The six launch attempts leading up to the IPO had a 66% failure rate, which included explosions and failures to reach orbit. Critically, after the sixth failure in April 2025, the Federal Aviation Administration (FAA) had prohibited further launches until Firefly completed a root-cause investigation and secured approval. This material regulatory and operational block was allegedly suppressed while the Company was aggressively soliciting IPO investment.

The Financial Misstatement: Firefly’s first public earnings report on September 22, 2025, revealed the extent of the financial divergence. Far from a surge, Firefly reported a 26.2% decline in revenue year-over-year. The Spacecraft Solutions segment, a key part of the growth story, generated only $9.2 million in revenue, a precipitous 49% year-over-year decrease. CEO Jason Kim's characterization of the quarter as "steady progress" may be scrutinized in light of these figures. The data exposed the alleged truth: the demand and growth prospects were grossly overstated.

Timeline of Alleged Misconduct and Disclosures

The alleged fraud follows a sharp, tight timeline—a causal chain narrative that accelerated the crisis.

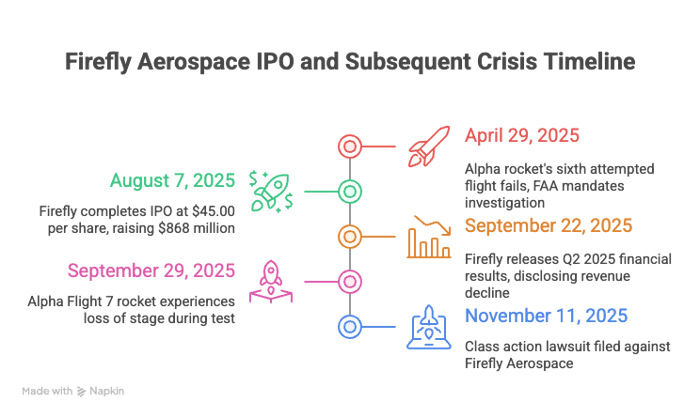

- April 29, 2025: Alpha rocket’s sixth attempted flight fails. The FAA mandates an investigation and prohibits further launch attempts until clearance. This material setback is allegedly suppressed in subsequent public-facing documents.

- July/August 2025: Firefly files its Offering Documents for the IPO. The complaint alleges these documents omit the severity of the Alpha failures and misrepresent the operational readiness and financial trajectory.

- August 7, 2025 (IPO): Firefly completes its IPO at $45.00 per share, raising $868 million. Stock trades up to $70.00 on its first day, fueled by the optimistic narrative. The Class Period begins.

- September 22, 2025 (First Corrective Disclosure):After market close, Firefly releases its Q2 2025 financial results. The report discloses a wider loss of $80.3 million and total revenue of $15.55 million, missing analyst estimates ($17.25 million) and declining 26.2% year-over-year. Crucially, the Spacecraft Solutions revenue had dropped 49%.

- Market Reaction: The next day, September 23, 2025, the stock fell 15.3% ($7.58 per share), closing at $41.94.

- September 29, 2025 (Second Corrective Disclosure): Firefly announces that the Alpha Flight 7 rocket experienced an event resulting in a loss of the stage during a test. This disclosure, coming just days after the CEO had expected the launch "in the coming weeks," highlighted the persistent operational risks. The Class Period ends.

- Market Reaction: The stock plummeted further, falling 20.73% ($7.66 per share) to close at $29.30 on September 30, 2025.

- November 11, 2025: The class action lawsuit is filed.

Investor Harm and Market Reaction

The two disclosures served as dual accelerants, quantifying investor losses and extinguishing the post-IPO buoyancy. The combined drop represented a catastrophic loss of capital and faith for those who bought into the public offering.

Investors who purchased shares at the $45.00 IPO price saw the value of their holdings shrink by nearly 35% in just over two weeks following the first disclosure, with the stock closing at $29.30 after the second. The September 23, 2025, decline alone erased approximately $146 million in market capitalization.

This rapid devaluation was notable because it occurred while broader market indices were reportedly hitting record highs, indicating the loss was specific to Firefly’s disclosed performance and operational crises. The market’s reaction tied the price drops directly to the revelation of previously concealed information—a classic case of loss causation in securities litigation.

The incident reframed the company’s immediate risk profile, shifting the focus from hitting projected revenue goals to confronting fundamental reliability concerns.

Litigation and Procedural Posture

The lawsuit, led by Plaintiff Jana K. Diamond, is brought on behalf of all investors who purchased Firefly securities during the Class Period, particularly those who acquired common stock traceable to the August 2025 IPO.

Asserted Legal Claims: The complaint alleges violations of the federal securities laws, specifically:

- The Securities Act of 1933 (Sections 11 and 15): Pertaining to the alleged untrue statements and material omissions in the Registration Statement and Prospectus used in the IPO.

- The Securities Exchange Act of 1934 (Sections 10(b) and 20(a)): Pertaining to the use of manipulative and deceptive devices in connection with the purchase or sale of securities, and for control person liability.

Defendants and Scienter: The defendants include Firefly Aerospace itself, along with key executives like CEO Jason Kim and CFO Darren Ma, and other directors. The suit summarizes scienter allegations—the required element of fraudulent intent or severe recklessness—by arguing that the executives, through their roles, must have known or were severely reckless in not knowing the true state of the Alpha program and the Spacecraft Solutions revenue decline prior to the IPO, yet they continued to promote the company’s misleading narrative. The CEO’s confident statements about the vehicle's readiness, made while the FAA investigation was ongoing, will be a central point of scrutiny.

Lead Plaintiff Deadline set for January 12, 2026, allowing investors with the largest financial interest to seek appointment to steer the litigation.

Shareholder Sentiment

The retail investor sentiment surrounding Firefly shifted with brutal speed. Following the IPO, the mood across platforms like Stocktwits and Reddit was one of explosive, almost euphoric excitement. Firefly was the next great space play, riding the wave of commercialization.

The tone began to cool immediately after the September 22 earnings miss. The revenue decline wasn't just a miss; it was a repudiation of the growth narrative. The Alpha rocket failure a week later was the final, sharp blow. Investor sentiment shifted from aspirational high-growth to genuine panic and rising risk perception.

The conversations quickly moved from boasting about first-day gains to raw, tactical fear. The focus turned to the financial consequences—the immediate need for management to detail next steps and addresses these technical and reputational challenges. The initial bravado evaporated, replaced by a sense of betrayal; the feeling of walking into a public offering based on a fundamentally flawed foundation.

Analyst Commentary

Professional analyst commentary highlighted the immense, arguably unsustainable, expectations baked into Firefly’s IPO valuation from the start.

The Company's Price-to-Sales (P/S) ratio was a significant red flag for analysts, even amidst the space sector’s hype. At 38.2x, Firefly was trading at a sharp premium, vastly exceeding the U.S. Aerospace & Defense industry average of 3.4x. This steep multiple was essentially pricing in hyper-aggressive future revenue growth, placing a premium on potential rather than proven execution.

Following the twin disclosures, analysts had to confront the reality that the promised growth was not materializing. Despite the stock trading at a "sharp discount to analyst targets" (Webull) after the fall, the fundamental question remained: Was the market now overlooking long-term potential, or was all the risk finally priced in?

The divergence in valuation was palpable. Even post-crash, the Simply Wall St Community showed wildly different "fair value estimates," ranging from a low of US $9.40 to a high of US $70 per share. This lack of consensus is telling; it suggests that even professional investors are deeply divided on whether Firefly’s underlying technology justifies its initial valuation, or if the technical and legal failures have rendered the original investment thesis obsolete.

SEC Filings & Risk Factors

The lawsuit's claims under the Securities Act are centered on the Offering Documents—the S-1 Registration Statement and Prospectus—filed with the SEC in connection with the August 2025 IPO.

In any major offering, risk factors are a dense, required section meant to insulate the company from litigation by warning investors of possible pitfalls. However, the allegation here is not that the Company failed to warn of potential risk, but that it failed to disclose materialized problems.

The primary omission relates to the Alpha rocket’s reliability. The complaint alleges that the Offering Documents failed to disclose the full extent of the operational failures, specifically that four out of six launch attempts had already failed. Even more critically, the filings allegedly failed to disclose the FAA’s decision to bar the company from conducting further launches until an investigation was completed.

A reasonable risk factor would warn: “If the Alpha rocket program encounters technical setbacks or failures, our launch schedule and revenue may be adversely affected.” The alleged omission is that the risk had already been triggered: “The Alpha rocket program has encountered technical failures requiring an FAA-mandated operational halt.” The difference between a warning and an omission of a material existing fact is the line between valid risk disclosure and alleged fraud.

Conclusion: Implications for Investors

The Firefly Aerospace securities class action serves as a potent reminder for investors in high-growth, technically complex sectors like space and defense. When the narrative is about a "historic" IPO and a "billion-dollar backlog," the investor’s due diligence must pivot to the granular: operational execution and segment-specific revenue validation.

This litigation is a battle over the fundamental truth of the Company's business at the moment it went public. It reinforces the causal chain: misstatement leads to inflated price, truth emerges, price corrects violently. The only question now is the scale of the resulting liability, and how much of that original $45.00 share price was based on a lie.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Inspire Medical Systems Inc. (INSP) Lawsuit Update [November 26, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/insp-alert-plus-banner-image.webp)

![Telix Pharmaceuticals Ltd. (TLX) Securities Class Action Update [November 21, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/tlx-alert-plus-banner-image.png)

![Primo Brands Corporation (PRMB) Securities Class Action Update [November 25, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/prmb-alert-plus-banner-image.webp)