Table of Contents

- Understanding Misleading Financial Statements

- Common Techniques of Misleading Financial Statements

- Identifying Red Flags in Financial Reporting

- Regulatory Frameworks and Compliance Requirements

- The Role of Auditors in Detecting Misleading Statements

- Consequences of Misleading Financial Reports

- Preventative Measures Against Financial Misrepresentation

- Leveraging Technology for Financial Statement Fraud Detection

- Best Practices for Reviewing Financial Statements

- The Need for Transparency in Financial Reporting

- FAQs

Understanding Misleading Financial Statements

In today’s interconnected business landscape, an accurate and transparent financial reporting process is the lifeblood of trust, credibility, and sustainable growth.

Yet, history is riddled with scandals and market tremors caused by misleading financial statements, fraudulent financial reporting, deliberate acts, or errors that distort a company’s accurate financial picture.

Misleading statements can have far-reaching effects, unsettling investors, destroying brands, and, in extreme cases, destabilizing markets.

Definition and Importance of Accurate Reporting

Misleading financial statements typically involve the manipulation or misrepresentation of a company’s financial information with the intent to deceive stakeholders.

Fraudulent financial statements involve the intentional misstatement or omission of financial information with the purpose of deceiving stakeholders and inducing reliance.

Integral to economic stability, honest financial statements are relied upon by investors, analysts, lenders, regulators, and employees for critical decision-making, ranging from investment and lending to hiring and policy-making.

Inaccuracies compromise trust and can trigger legal penalties or erode market confidence.

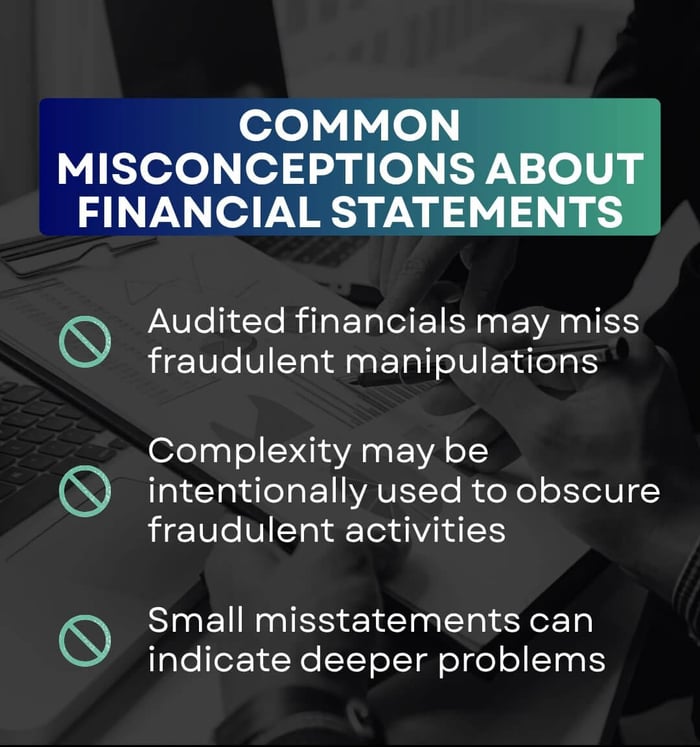

Common Misconceptions About Financial Statements

- All audited statements are trustworthy; however, even audited financials may miss fraudulent manipulations if sophisticated concealment tactics are employed.

- Complex jargon is often seen as a sign of authenticity: sometimes, complexity conceals irregularities or is intentionally used to obscure fraudulent activities.

- Minor errors are inconsequential: Small misstatements can indicate deeper problems with a significant cumulative impact.

Common Techniques of Misleading Financial Statements

Misleading statements take many forms, most commonly through the manipulation of revenues, expenses, and balance sheet entries.

Below are techniques used to distort the actual financial state of a business:

1. Creative Accounting and Its Implications

Creative accounting exploits permissible discretion within accounting standards to present more favorable results. While creative accounting may comply with formal rules, it can still violate the spirit of fair presentation under GAAP or IFRS. Creative accounting could potentially be masking poor performance or risk and paving the way for outright fraud.

Implications:

- Erodes investor trust.

- Can lead to regulatory scrutiny and sanctions.

- Often precedes larger fraudulent schemes.

2. Revenue Recognition Manipulation

Manipulating the timing or amount of revenue recognized is one of the most common types of financial statement fraud.

Tactics:

- Recording revenue before goods/services are delivered (premature recognition).

- Counting fictitious revenue (phantom sales, double-counted transactions).

- Deferring revenue to future periods to smooth earnings.

Impact: Misleads investors regarding growth and performance, thereby inflating the company's valuation.

3. Expense Capitalization vs. Immediate Expense Recognition

Firms may inappropriately capitalize expenses (recording them as assets rather than costs) to inflate profits in the current period.

Example:

- Capitalizing routine maintenance costs rather than expensing them, thereby boosting net income.

Result: Overstates asset values and profitability, deceiving stakeholders about the company’s actual performance.

4. Off-Balance-Sheet Financing Tactics

Off-balance-sheet financing involves structuring financial obligations—such as debt, leases, or guarantees—in ways that exclude them from a company’s balance sheet. This can mislead investors about a company’s true financial condition.

Common methods include:

- Use of Special Purpose Vehicles (SPVs) or unconsolidated entities to house liabilities.

- Lease arrangements structured to qualify as operating leases (under pre-ASC 842 standards), which are excluded from liabilities.

- Synthetic financing or joint ventures that obscure economic exposure.

Risk: Conceals actual debt burden, misleading creditors, investors, and regulators.

Regulatory note: Standards like ASC 842 (effective 2019) now require many previously off-balance-sheet leases to be reported as liabilities, increasing transparency.

Identifying Red Flags in Financial Reporting

Investors, auditors, and regulators must remain vigilant for signals that indicate possible manipulation or misrepresentation.

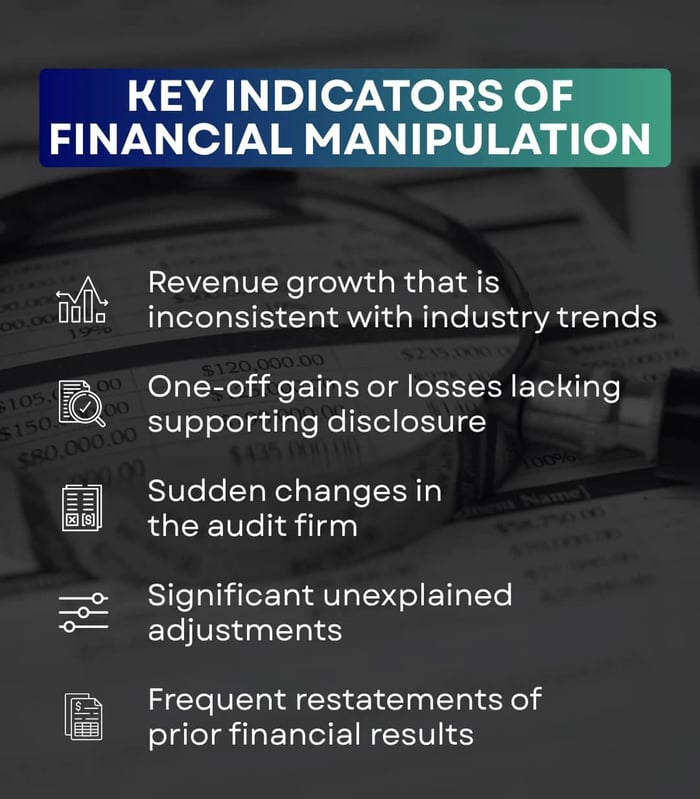

Key Indicators of Financial Manipulation

- Unexplained or sustained revenue growth inconsistent with industry trends.

- Significant, one-off gains or losses lacking supporting disclosure.

- Sudden changes in the audit firm or turnover of key accounting officers.

- Significant unexplained adjustments at period-end.

- Frequent restatements of prior financial results.

Analyzing Growth Trends and Outliers

Comparative analysis is vital:

- Vertical analysis: Examines each income statement item as a percentage of revenue to spot inconsistencies.

- Horizontal analysis: Compares performance over several periods to reveal unnatural trends.

Recognizing Related Party Transactions

Excessive or opaque transactions with related parties may serve as a channel for siphoning funds or masking liabilities.

Examples:

- Contracts with companies owned by insiders at non-market terms.

- Loans to or from executive-controlled entities.

Regulatory Frameworks and Compliance Requirements

Key Regulations Addressing Financial Statement Accuracy

- SEC regulations: Require public companies to file regular, accurate disclosures.

- Generally Accepted Accounting Principles (GAAP): Mandate consistency and accuracy in US financial reporting.

The Sarbanes-Oxley Act: Implications for Corporations

The Sarbanes-Oxley Act of 2002 (SOX) and related SEC regulations require CEOs and CFOs of public companies to personally certify the accuracy and completeness of their financial statements under penalty of law. Passed in the wake of financial scandals, the Sarbanes-Oxley Act (SOX) overhauled financial reporting:

- Section 302: mandates the CEOs/CFOs must personally certify the “fair presentation” of quarterly and annual reports.

- Section 404: requires management and auditors to assess and report on the effectiveness of internal controls over financial reporting.

- Section 802: imposes criminal penalties for knowingly destroying, altering, or falsifying financial records with the intent to obstruct investigations

- Enhanced whistleblower protections and reporting of off-balance-sheet obligations.

Global Standards and Best Practices

International Financial Reporting Standards (IFRS) and various governmental requirements emphasize comparative transparency and accountability, supporting global investor confidence.

The Role of Auditors in Detecting Misleading Statements

Audit Processes and Ethical Responsibilities

Auditors review financial statements to ensure compliance with applicable accounting standards and identify potential fraud risk factors.

The profession is grounded in skepticism, the mindset that fraud could exist even in the face of honest prior dealings.

Key auditor objectives:

- Identify and assess risks of material misstatement due to fraud.

- Obtain sufficient evidence to address these risks.

- Respond appropriately to errors or fraud discovered.

Limitations of Traditional Auditing Techniques

Despite rigorous standards, external audits have inherent limitations:

- Reliance on management representations: Auditors often depend on company-provided information, which may be inaccurate or incomplete.

- Resource and scope constraints: Audit firms operate under time and budget pressures, which can limit the depth of review.

- Collusive or deceptive management: Fraudulent executives may actively conceal evidence, rendering traditional audit procedures ineffective.

- Expectation gap: The public often assumes that audits are designed to detect all fraud, but auditors are primarily responsible for assessing material misstatements—not guaranteeing fraud detection.

Consequences of Misleading Financial Reports

Legal Implications for Companies and Executives

Falsifying financial statements can lead to both civil and criminal liability under federal securities laws. Companies and individuals can face civil and criminal penalties, including hefty fines and imprisonment. The SEC, DOJ, and other regulators aggressively pursue those who violate the rules.

As previously mentioned, the Sarbanes-Oxley Act (SOX) and SEC rules require senior executives to personally certify the accuracy of their financial statements, holding them directly liable for any misstatements.

Impact on Stakeholders and Market Trust

- Loss of stock value and delisting.

- Erosion of investor, employee, and community trust.

- Loss of access to capital or loans.

- Employee terminations and leadership turnover.

Case Studies of Major Financial Scandals

- Enron: One of the most infamous accounting scandals in history, Enron used complex off-balance-sheet entities (Special Purpose Entities or SPEs) to hide billions in debt and inflate earnings. The deception led to the collapse of the company and the dissolution of its auditor, Arthur Andersen LLP.

- WorldCom:CEO Bernie Ebbers orchestrated a $3.8 billion fraud by capitalizing expenses that should have been expensed, misleading investors until the company's bankruptcy. Ebbers was sentenced to 25 years in prison.

- HealthSouth:CEO Richard Scrushy was accused of directing executives to inflate earnings by $1.8 billion. Although acquitted of criminal charges, the scandal exposed widespread internal control failures.

- AIG: The insurance giant faced charges of accounting fraud for using sham transactions to bolster reserves and misstate financial results. AIG ultimately paid over $1.5 billion in penalties and underwent leadership changes.

Preventative Measures Against Financial Misrepresentation

Strengthening Internal Controls and Governance

- Implementing structured accounting systems with clear audit trails and separation of duties.

- Regular internal and external audits.

- Establish clear policies for approving transactions with related parties.

Importance of Ethical Leadership in Financial Reporting

The tone at the top sets organization-wide expectations. Ethical leaders model transparency and discipline, deterring fraud through example and policy.

Training and Awareness Programs for Employees

- Ongoing education on ethics, accounting standards, and fraud red flags.

- Encouragement of whistleblowing with safe, anonymous hotlines.

Leveraging Technology for Financial Statement Fraud Detection

Artificial Intelligence and Machine Learning Applications

AI can analyze immense volumes of financial records, spotting anomalies that suggest fraud, for example, outlier detection in journal entries or comparative ratio analysis.

Data Analytics Tools for Financial Review

- Real-time dashboards and statistical analysis.

- Predictive analytics to anticipate areas of risk.

Emerging Technologies in Fraud Detection

Among the most effective:

- Machine learning classifiers (e.g., support vector machines) for fraud detection.

- Data mining for identifying irregular patterns.

- Automated compliance monitoring.

Best Practices for Reviewing Financial Statements

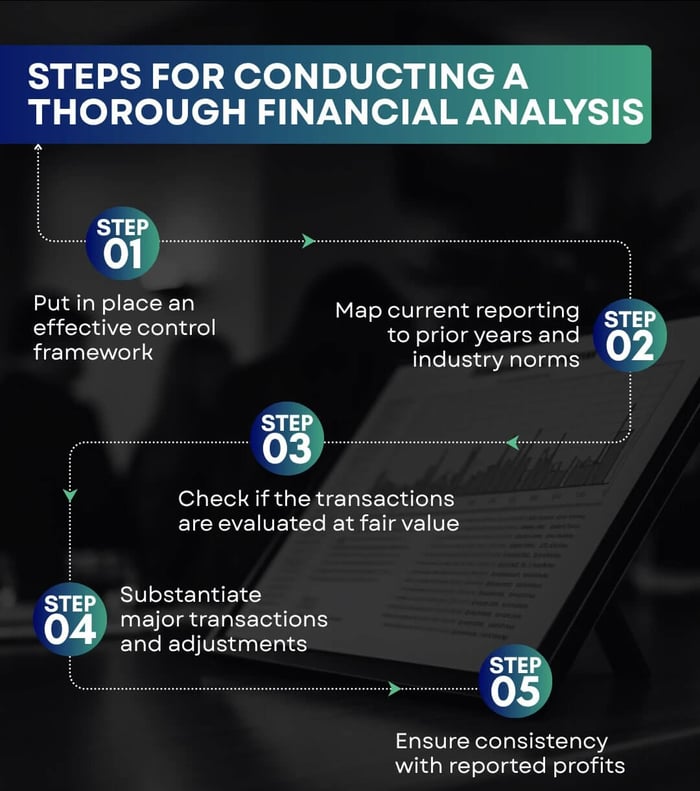

Steps for Conducting a Thorough Financial Analysis

- Verify internal controls: Is there a practical control framework in place?

- Assess consistency by comparing current reporting to prior years, industry norms, and segment data.

- Probe related-party transactions: Are they explained and at fair value?

- Seek supporting evidence: Substantiate foremost transactions and adjustments.

- Analyze cash flows: Ensure consistency with reported profits.

Engaging Third-Party Consultants for Review

In complex situations, it’s beneficial to engage external consultants or forensic accountants with no vested interest in the company’s performance, ensuring objectivity and methodological rigor.

The Need for Transparency in Financial Reporting

Transparent and accurate financial reporting underpins market integrity and investor confidence. Transparency helps safeguard investments and enable sound policy-making.

Strong regulation, effective governance, technological innovation, and a culture of ethical leadership are crucial in preventing and detecting misleading financial statements.

The cost of complacency, both monetary and reputational, can devastate even the most seemingly robust of enterprises.

This guide is a comprehensive resource for detecting, understanding, and preventing misleading financial statements.

Vigilance, continual learning, and a commitment to transparency are vital for maintaining integrity in financial reporting.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal advice. Readers should not act or refrain from acting based on any of the information contained in this blog without consulting a qualified legal professional. Levi & Korsinsky LLP is not responsible for any actions taken or not taken based on the information provided in this blog.

You Can Also Read... |

FAQs

What is financial statement fraud?

It is the intentional manipulation or misrepresentation of a company’s financial data to deceive stakeholders, often for personal gain or to mask poor performance.

How are financial statements manipulated or misrepresented?

Through techniques like inflating revenue, capitalizing expenses improperly, hiding liabilities, using off-balance-sheet transactions, or creating fictitious entries.

What is an example of a false or misleading financial statement?

Enron’s use of off-balance-sheet entities to conceal billions in debt, resulting in significant investor losses and ultimately leading to bankruptcy, is a classic example.

What are the causes of inaccurate financial reporting?

- Pressure to meet market expectations.

- Weak internal controls.

- Poor ethical culture and tone at the top.

What are the consequences of falsifying or inaccurately reporting financial statements?

Legal penalties, financial loss, leadership changes, and lasting reputational damage for both companies and individuals involved.

How can investors protect themselves from misleading financial information?

- Review multiple years’ statements and footnotes.

- Assess consistency between reported profits and cash flows.

- Look for large or unusual transactions, auditor changes, or restated results.

What should you do if you suspect a company is issuing false financial statements?

Report your suspicions to regulatory authorities, such as the SEC, or use whistleblower hotlines protected under SOX.