Vestis Lawsuit Raises Questions Over Growth, Promises, and Management Trust

Date: July 21, 2025

Caption: Torres v. Vestis Corporation, et al.

Case No.: 1:25-cv-48444

Jurisdiction: U.S. District Court, Southern District of New York

Filed on: June 9, 2025

Class Period: May 2, 2024 – May 6, 2025

Introduction to Vestis Corporation (VSTS) Securities Lawsuit

Vestis Corporation (NYSE: VSTS) is facing a federal securities class action lawsuit. The lawsuit accuses the company and two former executives of misleading investors about operational health and financial projections. The complaint is brought by shareholder Cesar Torres on behalf of a proposed class. It focuses on the company’s public statements over a one-year period between May 2024 and May 2025.

Plaintiffs argue Vestis misrepresented its growth strategy, concealed service-related problems, and presented a steady outlook. Meanwhile, internal data showed rising customer. The issue came to a head on May 7, 2025 after Vestis posted dismal earnings and yanked its fiscal guidance. Those moves sent its stock price into freefall, causing a 37 percent loss in just a day. Investors lost millions and many now say they were blindsided.

This article walks through what’s alleged in the Vestis securities class action lawsuit, what the filings say, how the market reacted, and what it might mean for shareholders watching this case unfold.

Backdrop and Business Context

Vestis provides commercial uniform rentals, floor mats, restroom supplies, safety gear. These products are delivered on a set schedule to clients ranging from restaurants to industrial facilities. The model depends on customer retention. Most of the company’s revenue comes from long-term service contracts.

The company became a standalone public entity in 2023 after it spun off from Aramark. The pitch was that independence would allow Vestis to become more focused and efficient. Leadership emphasized new investments in sales and operations and projected modest but stable growth. They also pointed to pricing flexibility and better client support as ways to drive long-term gains.

Promises Made vs. Reality

Starting in mid-2024, Vestis delivered what appeared to be a confident message. On its May 2024 earnings call, then-CEO Kimberly T. Scott told analysts the company had taken “decisive actions” to improve growth and strengthen service. She described the sales team as more aligned and pointed to stronger customer engagement.

In November 2024, Vestis issued a press release announcing its fiscal 2025 growth guidance. The company projected between $2.8 billion and $2.83 billion in revenue, along with $345 million to $360 million in adjusted EBITDA. Scott described the numbers as realistic and grounded in improving client relationships and a “strong commercial pipeline.”

In early 2025, CFO Ricky T. Dillon announced he would step down. The company didn’t revise its projections. Scott said retention remained above 92 percent and noted that new customer onboarding had increased. She also said she expected EBITDA to rise by as much as 10 percent in the back half of the year.

But according to the complaint, the story playing out internally was very different. Vestis was losing clients at a higher-than-expected rate. Price increases had been introduced before service issues were resolved, which created dissatisfaction. Plaintiffs say the company had internal churn data and service metrics showing warning signs, but defendants failed to warn investors of that data. That data contradicted the rosy public story executives were spinning.

Timeline of Alleged Misconduct and Disclosures

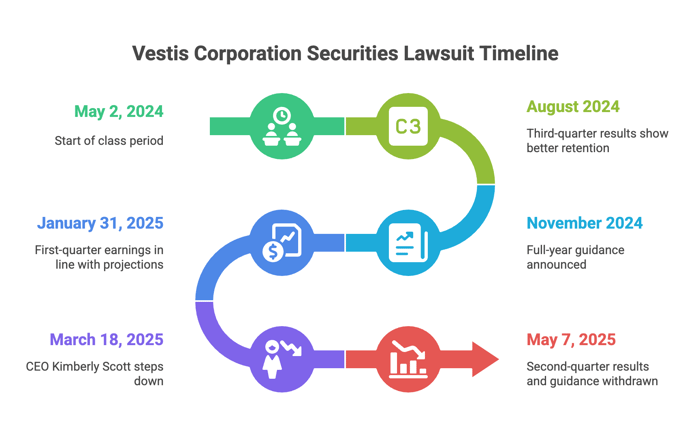

The lawsuit centers on a timeline beginning in May 2024. That month, Vestis released earnings and emphasized positive developments in operations. The stock price remained stable, and investor attention stayed light.

By August 2024, third-quarter results showed slightly better-than-expected customer retention. On the call, CFO Dillon suggested that churn was coming under control and projected fewer losses moving into the new fiscal year. This nudged the stock upward.

In November, full-year guidance was announced. The projections exceeded market expectations, and by January 2025, Vestis stock was trading near $11.87—its highest point in the class period.

On January 31, 2025, Vestis reported first-quarter earnings that were in line with projections. That same day, Dillon’s departure was confirmed. He would exit the company two weeks later. Scott reaffirmed the guidance during the earnings call, and the stock barely moved.

On March 18, 2025, Scott herself stepped down. She was replaced by interim CEO Phillip Holloman. The resignation raised some questions but again caused minimal impact on share price.

The pivot came on May 7. That day, Vestis released second-quarter results and withdrew its 2025 guidance. The company reported just $48 million in EBITDA—far below the previously forecast range—and cited ongoing service issues and economic pressures. Investors reacted immediately. The stock fell from $8.71 to $5.44 in one day.

Investor Harm and Market Reaction

The stock suffered substantial losses, shedding more than a third of its value in less than 24 hours. For shareholders who bought in at or near the peak, the damage was severe. Lead plaintiff Cesar Torres had purchased shares on March 3, 2025, at $11.87. After the earnings miss, those shares were worth less than half their original value.

The investor reaction was swift. Barclays cut its price target in half, reiterating an underweight rating. Their analysts pointed to systemic service failures and said recovery would likely take time. Wolfe Research revised its outlook as well, dropping its target to a range of $6 to $8 and warning that brand damage and client losses could give competitors an opening.

More broadly, investors expressed frustration that the company’s tone had changed so abruptly. There had been no warning. Management had been reiterating guidance just months earlier, even as internal challenges appear to have deepened.

Litigation and Procedural Posture

The lawsuit names as defendants Vestis Corporation, former CEO Kimberly Scott, and former CFO Ricky Dillon. Plaintiffs claim that the company violated federal securities laws, such as Section 10(b) of the Securities Exchange Act and SEC Rule 10b-5, by making false or misleading statements. They also bring Section 20(a) claims, holding Scott and Dillon responsible for their role in shaping company disclosures.

The complaint filed alleges both executives had access to data showing client attrition and service-level failures. Their public statements during earnings calls and guidance updates allegedly failed to account for these internal realities. The plaintiffs argue that the resignations, which occurred shortly before the disclosure, suggest foreknowledge.

The case remains in early stages and a lead plaintiff has not yet been appointed. Class certification has not yet been granted, and defendants have not filed a formal motion to dismiss. If the case moves forward, discovery may bring internal communications and operational records into the spotlight.

Shareholder Sentiment

In the lead-up to May 2025, retail investors on platforms like Reddit, Stocktwits, and X were cautiously optimistic. Many pointed to the company’s stable customer base and believed the spin-off from Aramark would eventually pay off. Some were drawn by the low share price and the idea of a turnaround play.

In November 2024, one user wrote, “Not flashy, but the retention rate looks solid. Could be a sleeper.” Another comment from January 2025 read, “They’ve been consistent lately. Might be under the radar.”

After the May 7 drop, the mood shifted quickly. “We got blindsided,” one Reddit user wrote. “They were saying everything was fine. Then boom, $5 stock.” On Stocktwits, a user posted, “Can’t believe how fast this unraveled. Management totally lost my trust.”

The emotional response wasn’t just about money. It reflected a feeling that trust had been misplaced.

Analyst Commentary

Analyst sentiment toward Vestis securities before May 2025 was lukewarm but stable. Jefferies had maintained a neutral outlook through late 2024, noting that execution risk remained but commending the company for hitting EBITDA targets. Price targets at the time ranged from $12 to $14.

Barclays, too, had flagged service concerns in passing, but ultimately backed the company’s 2025 outlook. The tone began to change in early 2025, especially after Dillon’s resignation, but no major downgrades came until after the May disclosure.

Once the numbers were in, analysts moved quickly. Barclays described the guidance withdrawal as “deeply concerning” and warned that internal issues were likely underestimated. Wolfe Research echoed that sentiment, saying that Vestis had failed to rebuild investor trust and could face long-term brand harm in key markets.

SEC Filings & Risk Factors

From May 2024 through early 2025, Vestis issued a series of SEC filings that focused heavily on growth metrics, sales wins, and retention performance. Its November 2024 10-K reiterated the company’s full-year outlook and included generic caution around inflation, competition, and labor markets. There was no mention of specific service-level risks or customer churn outside normal expectations.

The company’s 10-Qs followed a similar pattern. Language around risks remained general. Terms like “operational challenges” and “market headwinds” were used but not expanded upon.

On May 7, 2025, Vestis filed an 8-K that told a different story. It disclosed declining revenue, higher-than-expected churn, and customer credits issued due to service lapses. The company also said that economic conditions had contributed to missed expectations, though it did not explain when management first became aware of the shortfall.

The lawsuit argues that earlier filings were incomplete in a way that mattered. The market’s sharp reaction supports the idea that investors were not expecting such a drop.

Conclusion: Investor Implications

For shareholders, the Vestis lawsuit serves as a clear warning. A company’s public tone may not always reflect what’s happening beneath the surface. Strong guidance and steady earnings can be comforting, but when customer satisfaction is core to the business model, operational gaps can quickly undo those gains.

Executive departures, particularly in close succession, deserve close scrutiny. And in service-heavy businesses like this, problems often start in places that don’t appear on financial statements—missed deliveries, long hold times, delayed credits. These details add up.

Vestis now faces a legal challenge that may open up its internal records. For investors still holding shares, the case may bring clarity about what went wrong and when. For others, it’s a broader lesson in watching for red flags that come not from numbers, but from silence. What’s not said can be as telling as what is.