![Bath & Body Works, Inc. (BBWI) Securities Class Action Lawsuit Update [January 19, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/bbwi-alert-plus-banner.webp)

Adjacencies, Promotions, and the Cost of Losing the Core

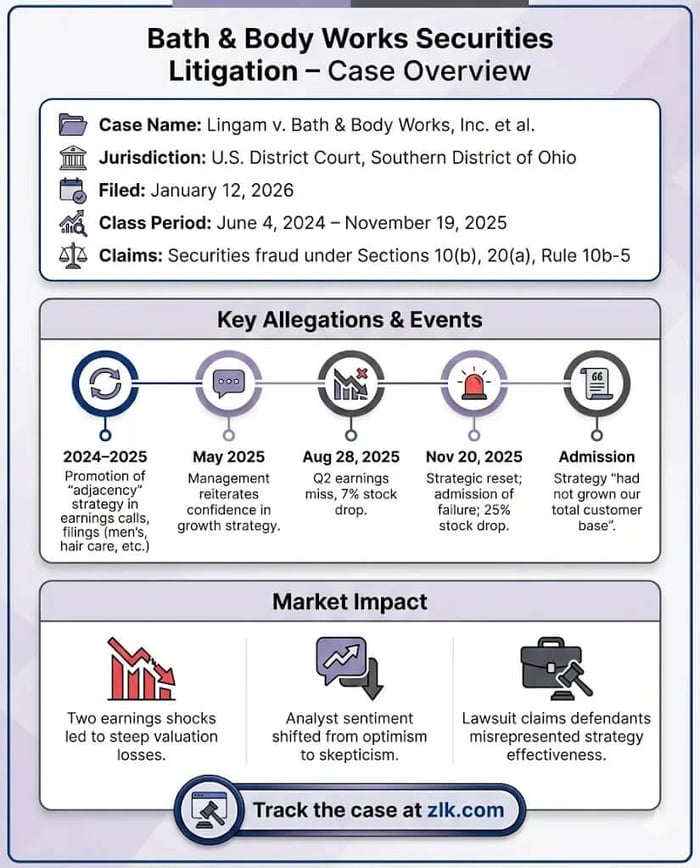

Case Name: Lingam v. Bath & Body Works, Inc. et al.

Case No.: 2:26-cv-00039-MHW-EPD

Jurisdiction: U.S. District Court, Southern District of Ohio

Filed on: January 12, 2026

Class Period: June 4, 2024-November 19, 2025

Introduction

Bath & Body Works, Inc. (NYSE: BBWI) told investors it was extending its reach. By late 2025, it admitted that reach had come at the expense of focus.

In January 2026, investors filed a federal securities class action alleging that Bath & Body Works misled the market about the effectiveness of its strategy built around product “adjacencies,” brand collaborations, and aggressive promotions. According to the complaint, management repeatedly framed these initiatives as engines of sustainable growth, even as they failed to expand the customer base and masked weakening fundamentals. The reckoning arrived through a pair of earnings shocks in August and November 2025—each followed by steep stock declines—and culminated in the company’s own admission that its strategy “had not grown our total customer base.”

Backdrop and Business Context

Bath & Body Works is a specialty retailer of home fragrance and body care products, long defined by a tight focus on a handful of high-margin core categories. Beginning in fiscal 2024, the company leaned into what it called “adjacencies”—new product lines including men’s grooming, hair, lip, and laundry—alongside collaborations and heavier promotional activity.

Management described these initiatives as a way to reach new customers, refresh the brand, and drive top-line growth. Investor presentations, earnings calls, and SEC filings repeatedly emphasized innovation, storytelling, and category expansion as proof that the strategy was working. Internally, according to the complaint, those same initiatives were failing to deliver durable growth while diverting attention from the core business.

Promises Made vs. Reality

Throughout the class period, Bath & Body Works publicly attributed its results to strong execution and innovation. In quarterly filings and presentations, the company said growth was supported by “continued focus on our new category adjacencies” and portrayed men’s, hair, lip, and laundry as fast-growing contributors.

The reality emerged only later. In November 2025, the company conceded that its adjacency strategy had not expanded the customer base, that collaborations had been used “to carry quarters,” and that the business had become “overly reliant on deeper and more frequent promotions.” Management acknowledged that these choices reduced investment in core categories and delivered diminishing returns—an admission that directly contradicted prior assurances that adjacencies were accelerating growth rather than masking weakness.

Timeline of Alleged Misconduct and Disclosures

The alleged misconduct spans more than a year of public messaging, stretching from mid-2024 through late-2025.

In June 2024, Bath & Body Works opened the class period by highlighting adjacencies as growth drivers in earnings releases, investor presentations, and its Form 10-Q. That narrative continued through 2024 and into early 2025, with management repeatedly affirming guidance and emphasizing innovation, collaborations, and category expansion.

The narrative carried into early 2025. On February 27, 2025, the company reported fourth-quarter and full-year 2024 results, stating that its “strategy is working” and reiterating that adjacencies and collaborations were driving topline growth, while issuing full-year 2025 guidance. That message was reinforced again in May 2025, when Bath & Body Works pre-announced first-quarter results on May 19, 2025 and formally reported them on May 29, 2025, maintaining full-year guidance and continuing to emphasize adjacent categories as a source of momentum.

The first major inflection point came on August 28, 2025, when the company reported second-quarter results showing a sharp year-over-year earnings decline and cut full-year guidance. Shares fell nearly 7% on unusually heavy volume.

The second—and more severe—disclosure followed on November 20, 2025. Bath & Body Works reported declining revenue, slashed guidance again, and unveiled a strategic reset. In an accompanying presentation and earnings call, management admitted that adjacencies and promotions had failed to deliver growth and would be exited in favor of refocusing on the core. The stock fell roughly 25% in a single session.

Investor Harm and Market Reaction

According to the complaint, investors suffered significant losses as the market recalibrated its expectations. The August 2025 disclosure erased hundreds of millions of dollars in market capitalization. The November 2025 announcement was more devastating, wiping out nearly a quarter of the company’s value in one day.

Plaintiffs tie these losses directly to the corrective disclosures, arguing that earlier statements artificially inflated the stock by portraying a strategy that was already faltering as a durable growth engine.

Litigation and Procedural Posture

The action is pending in the U.S. District Court for the Southern District of Ohio. The complaint asserts claims under Sections 10(b) and 20(a) of the Securities Exchange Act of 1934 and Rule 10b-5. Defendants include Bath & Body Works and senior executives Gina Boswell (former CEO), Daniel Heaf (CEO), and Eva Boratto (CFO).

Plaintiffs allege that defendants knew or recklessly disregarded that the adjacency-driven strategy was not growing the customer base, that collaborations were being used to smooth results, and that guidance lacked a reasonable basis. Scienter is pled through defendants’ access to internal performance data and their own later admissions about the strategy’s failure.

Shareholder Sentiment

Investor sentiment around Bath & Body Works shifted sharply as the company’s narrative around “adjacencies” unraveled in late 2025.

In the weeks following the November earnings release and strategic reset, discussion across Stocktwits and X (formerly Twitter) turned from cautious optimism to outright frustration. Retail investors fixated on management’s admission that adjacencies “had not grown our total customer base,” a reversal that many users framed as an implicit acknowledgment that prior messaging overstated the strategy’s effectiveness. On Stocktwits, bearish commentary surged as traders debated whether the damage reflected a temporary reset or a deeper brand erosion problem.

On X, investors circulated clips and quotes from the earnings call, particularly CEO Daniel Heaf’s explanation that adjacencies “reduced focus in investing in our core categories,” questioning why that tradeoff was not disclosed sooner. Several widely shared posts framed the disclosure not as a single bad quarter, but as a credibility break—less about macro pressure, more about strategy drift.

Reddit discussions in investing and retail-focused forums echoed that theme. Commenters described the November reset as a “walk-back” of a growth story that had been promoted for more than a year, with some users arguing that promotions and collaborations had been masking stagnation rather than creating demand.

The throughline was not panic, but disappointment. Investors appeared less surprised by slowing sales than by how abruptly management reframed what had previously been sold as a durable growth engine.

Analyst Commentary

Professional analysts were more restrained, but no less direct. Coverage following Bath & Body Works’ August and November 2025 disclosures focused on execution risk, margin sustainability, and the credibility of the company’s prior growth narrative.

After the August earnings miss and guidance cut, several analysts highlighted pressure from promotions and questioned whether adjacencies were contributing incremental demand or simply shifting mix. As Reuters noted at the time, the company was already facing skepticism about whether product expansion could offset a cautious consumer backdrop.

The tone hardened after November’s strategic reset. Analysts seized on management’s acknowledgment that adjacencies failed to expand the customer base, reframing earlier results as less a macro story and more a strategic miscalculation. Barron’s coverage emphasized the scale of the reset and the challenge of rebuilding momentum while simultaneously exiting categories that had been heavily promoted.

Equity research commentary summarized by Seeking Alpha pointed to declining confidence in near-term earnings visibility, with contributors noting that reliance on promotions can temporarily support revenue but often compress margins and dilute brand equity.

Meanwhile, outlets like CNBC framed the selloff as a repricing event—investors reassessing not just near-term earnings, but the longer-term story around whether Bath & Body Works could grow beyond its core without undermining it.

Taken together, analyst reaction reflected a market no longer underwriting the adjacency thesis on faith. The question shifted from “when does growth reaccelerate?” to something more basic: whether the company’s core can now carry the weight it was once asked to share.

SEC Filings & Risk Factors

Bath & Body Works’ SEC filings throughout the class period acknowledged macroeconomic pressure and consumer caution but continued to frame adjacencies and collaborations as strategic strengths. Risk disclosures discussed competition and changing consumer preferences, yet did not, according to plaintiffs, reveal that the company’s own strategy was undermining focus on the core business or relying on promotions to obscure weakness.

Only in late 2025 did filings and presentations align with the company’s operational reality, conceding that prior assumptions about category expansion were flawed.

Conclusion: Implications for Investors

The Bath & Body Works lawsuit underscores a familiar lesson in retail-sector securities litigation: strategy narratives matter, but execution truth eventually surfaces.

For investors, the case is a reminder to scrutinize growth stories built on expansion beyond a company’s core—especially when those stories rely heavily on promotions, collaborations, or frequent reinvention. When management later admits that the strategy itself was the problem, the market response can be swift and unforgiving. Now, shareholders are asking whether that reckoning should have come sooner—and whether the law provides a remedy.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Fly-E Group, Inc. (FLYE) Securities Class Action Lawsuit Update [December 4, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/flye-alert-plus-banner.webp)

![Vistagen Therapeutics, Inc. (VTGN) Securities Class Action Lawsuit Update [January 19, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/vtgn-alert-plus-banner.webp)

![CoreWeave, Inc. (CRWV) Securities Class Action Lawsuit Update [January 19, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/crwv-alert-plus-banner.webp)