Table of Contents

- Introduction

- The 10-K: The Year in Review

- The 10-Q: The Quarterly Check-In

- Why These Forms Matter to Investors

- What’s Inside a 10-K and 10-Q

- “SOX” Certifications and “Material Weaknesses”

- Why They Matter in Securities Fraud Cases

- When a Dodgy SOX Certification Isn’t Enough: In re Watchguard Securities Litigation

- When the 10-K Becomes the Smoking Gun: The AIG Example

- What to Look For as an Investor

- You Don’t Have to Be an Analyst to Notice

- Final Thought: Paper Trails Don’t Lie (Unless Someone Does)

Introduction

Four times a year, public companies pull back the curtain. They file quarterly reports (Form 10-Q) three times a year for the first three fiscal quarters and an annual report (Form 10-K) once a year. Not because they want to, but because they have to. They file official reports with the U.S. Securities and Exchange Commission (SEC): documents that, on paper, give you the state of the business.

Two of those reports have names that sound like they came from an IRS bingo game: Form 10-K and Form 10-Q.

They aren’t flashy. They aren’t fun. But they’re the backbone of public-company disclosure. If you’re an investor (or a securities law attorney!) they’re also the place where you can see the story before it hits the news. Or catch where the story doesn’t add up.

The 10-K: The Year in Review

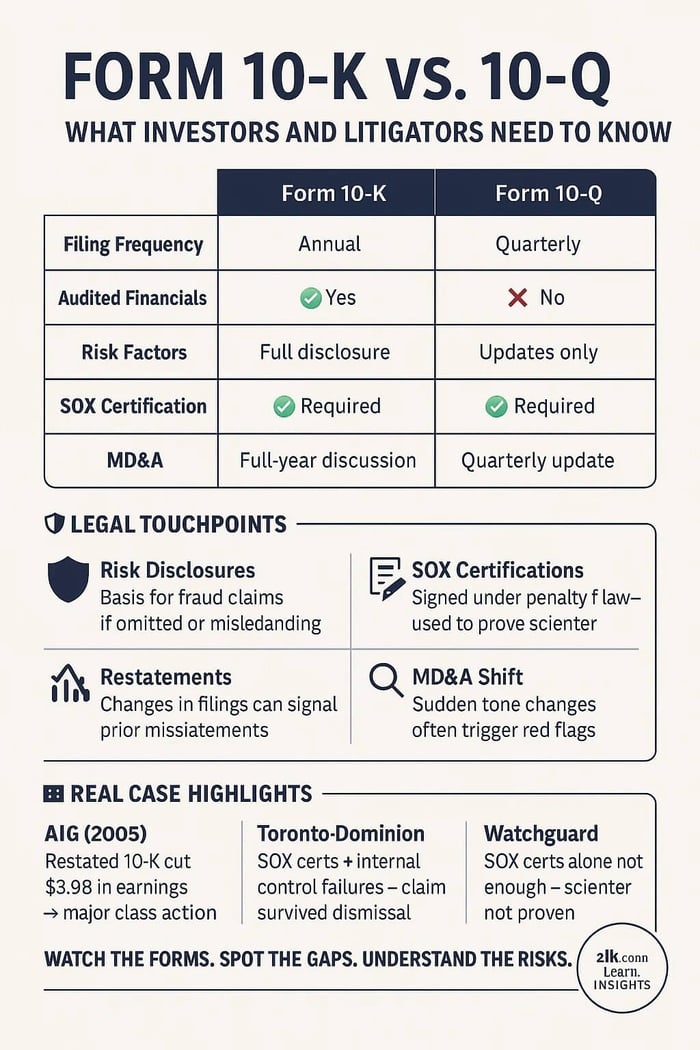

Think of the 10-K as the annual wrap-up. It’s long . . . often more than a hundred pages. The 10-K gets filed once a year.

- Audited financial statements

- A full rundown of the company’s business and strategy

- Risk factors—everything the company says could go wrong

- Management’s discussion of financial condition and results (the “MD&A” section)

That risk factor section? It matters. It’s where a company admits to all the things that might tank the business. Typical “risks” include the economy, supply chain problems, regulatory investigations, just to name a few. Think “any material risks that could realistically affect the business, operations, or financial condition.” The company has to put it on paper—so that later, if something does happen, they can say: we told you so.

But here’s the thing: risk factors only help if they’re real. If a company downplays a known risk, or leaves one out, that gap can turn into a securities fraud claim.

The 10-Q: The Quarterly Check-In

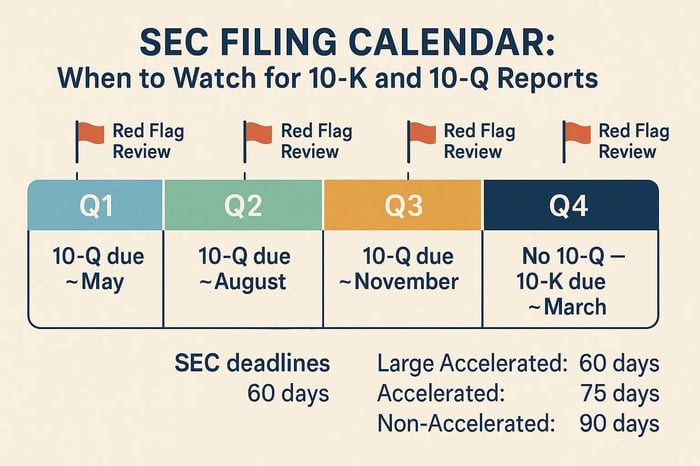

If the 10-K is the full yearbook, the 10-Q is the quarterly report card. Public companies file a 10-Q after each of the first three fiscal quarters—within 40 to 45 days of quarter-end, depending on filer status. No 10-Q is filed for the fourth quarter because the annual 10-K serves as the year-end report. It’s shorter. Less detail. No audited statements.

But it still matters, because it updates the story. It has:

- Unaudited financials for the quarter

- Management’s discussion of results

- Any material changes from the last 10-K, especially in risk factors

This is where patterns start to show. A revenue slide here. A sudden change in segment performance. A quiet update to the “what could go wrong” section. If you’re watching closely, those changes can be more revealing than the numbers themselves.

Why These Forms Matter to Investors

If you own stock—whether you check your portfolio daily or once a year—these filings are how you get the official version of the company’s story.

The 10-K and 10-Q aren’t just about data. They’re about consistency.

When leadership tells the market one thing on an earnings call but the 10-Q says something else, that inconsistency is a red flag. The same is true if risk factors suddenly expand after months of reassurance.

Investors who read these filings (or at least the summaries) aren’t looking for drama. They’re looking for alignment between what’s said, what’s written, and what’s happening in real time.

What’s Inside a 10-K and 10-Q

The 10-K is the full version. It’s where you’ll find audited financial statements, a detailed description of the company’s business, risk factors, management’s discussion and analysis (MD&A), and disclosures about legal proceedings. It’s big-picture and backward-looking, but also sets the stage for the year ahead.

The 10-Q is shorter. It updates the 10-K with unaudited financials, quarterly MD&A, and any material changes—especially in risk factors. It’s more about “what’s new” than “everything there is.”

Both filings carry legal weight. Every number, every risk disclosure, every note is made under the same anti-fraud rules. That’s why, for investors, knowing what’s in them isn’t trivia—it’s part of spotting whether the story’s shifting.

“SOX” Certifications and “Material Weaknesses”

Each report also includes Sarbanes–Oxley Act (SOX) certifications. These are affirmations, signed by the CEO and CFO, stating the financials are accurate, free from material misstatements, and that the company has effective internal controls over financial reporting. In plain terms, they’re affirming that the financial statements are fairly presented, that they have disclosed any known material weaknesses in internal controls, and that the company has systems designed to ensure accurate reporting. In securities fraud cases, these certifications can be powerful evidence: if internal records later show the executives knew about problems when they signed, that gap between what was certified and what was true becomes a direct path to proving scienter.

One example: in In re Toronto-Dominion Securities Litigation, investors claimed executives falsely certified that internal controls were effective while knowing about improper revenue recognition practices. Those SOX certifications, signed and filed alongside the 10-Qs, became a central hook for the court in finding the allegations of intent to defraud plausible enough to survive dismissal. When the paperwork says “everything’s fine” and the evidence shows the opposite, those signatures can be as important as the numbers themselves.

Why They Matter in Securities Fraud Cases

Under U.S. securities law, these filings aren’t optional. They’re mandatory disclosures. Which means they carry legal weight.

If a company knowingly files false or misleading information in a 10-K or 10-Q—and investors rely on that info to make decisions—it can form the basis of a securities fraud lawsuit.

Courts take these documents seriously. They’re often Exhibit A in a complaint. Plaintiffs will point to a statement in the 10-Q that painted a positive picture, then show how internal emails or later admissions proved the opposite. Or they’ll show that a risk wasn’t disclosed until after the fact—when the damage was already done.

When a Dodgy SOX Certification Isn’t Enough: In re Watchguard Securities Litigation

In Watchguard, plaintiffs challenged the company’s 10-Q reports over the course of three quarters. In late 2005, Watchguard had to admit material weaknesses in its internal controls for the first three quarters of 2004. That meant those financial reports were flawed because something was rotten with the way it was compiling its numbers.

The problem was the company’s execs signed off on the SOX certifications on those very reports which the company said were no good. Specifically, the Court said those “certifications contained assurances that the stated financials results were adequate, and the certifying officers had designed adequate financial controls, evaluated those controls, and disclosed any material weaknesses.”

But, that wasn’t enough to prove scienter. The Court reminded attorneys and investors that just signing off on the SOX certification isn’t necessarily proof of fraudulent intent. There’s got to be some evidence of recklessness or knowledge, and that was missing in this case. Courts have held that signing a SOX certification, without more, is not sufficient to plead scienter. Plaintiffs must allege facts showing that the officer knew, or was reckless in not knowing, that the certification was false when signed.

When the 10-K Becomes the Smoking Gun: The AIG Example

In 2005, American International Group filed its annual 10-K with a twist—one that wiped out billions. The company restated prior years’ earnings, cutting $3.9 billion from reported profits and erasing $2.26 billion in shareholder equity. Buried in the fine print was the confirmation: earlier filings had overstated financial strength.

That restated 10-K didn’t just correct the record. It lit the fuse for one of the largest securities fraud cases in history. The restatement also prompted regulatory enforcement actions, including SEC charges and DOJ investigations, underscoring the gravity of such corrections. Plaintiffs pointed to the difference between the original numbers and the restatement as proof that AIG’s earlier disclosures were materially false. In litigation, the “before” and “after” filings became side-by-side evidence—showing how investors were misled, and how the truth only emerged once the company had no choice but to put it in black and white.

For investors, it was a reminder: a 10-K isn’t just a year-end recap. It’s sworn testimony. And when the numbers change this dramatically, it’s not an adjustment—it’s a confession.

What to Look For as an Investor

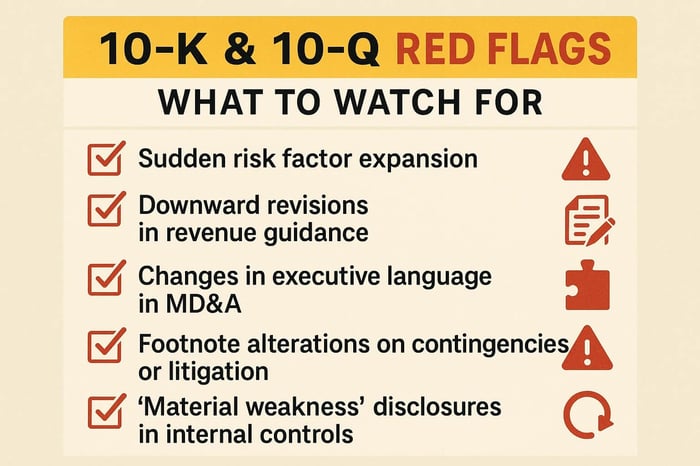

You don’t have to read every page. But skimming the right sections can tell you a lot:

- Risk Factors: Are they new, or did they suddenly get longer?

- Management Discussion (MD&A): Does the tone shift from past filings?

- Financial Trends: Do quarterly numbers match the story told elsewhere?

Changes between one quarter and the next can be especially telling. Sometimes the real signal isn’t in the headline—it’s buried in a footnote or a one-sentence update to a risk disclosure.

You Don’t Have to Be an Analyst to Notice

Most investors will never print out a 10-K and highlight it like a law school casebook. But even casual investors can benefit from paying attention to what changes—and what doesn’t—between filings.

Because for all the corporate polish, these are still sworn statements. And in the courtroom, they matter just as much as anything said in an interview or on an earnings call.

Final Thought: Paper Trails Don’t Lie (Unless Someone Does)

The 10-K and 10-Q aren’t bedtime reading. But they’re where the official story lives. They’re what courts look at first when things go wrong.

So even if you never download one yourself, remember: every number, every line in those forms, was signed off under penalty of law. And if the story in them isn’t true, it won’t just be a bad quarter—it could be the start of a lawsuit.

![iRobot Corporation (IRBT) Securities Class Action Lawsuit Update [August 15, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/irobot-securities-lawsuit-blog-banner.webp)