Table of Contents

- The Word Nobody Knows, but Every Case Turns On

- Why It Matters

- Case One: Scienter Proven—Tellabs, Inc. v. Makor Issues & Rights, Ltd.

- Case Two: Scienter Rebutted—Macomb County Employee Retirement Sys. v. Align Technology, Inc.

- Case Three: What It Takes—Matrixx Initiatives, Inc. v. Siracusano

- Why It’s So Hard

- Final Reflection

The Word Nobody Knows, but Every Case Turns On

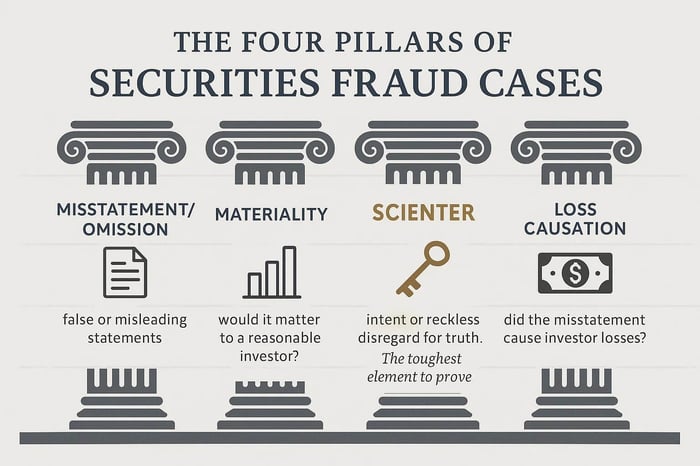

Anyone who’s ever read a securities law case knows there’s a few legal terms that just pop up every time. Things like “misstatement,” “materiality,” and “loss causation” appear in every case . . . and, for the most part, these words are somewhat self-explanatory (or, at least, they’re in English!). But then there’s one little Latin word that also pops up in every case: scienter.

In plain English, scienter is a legal term that refers to intent or knowledge of wrongdoing. It asks the question: “Did the company (and its execs) knowingly mislead investors or was it just sloppy?” That distinction means a lot and can decide whether the case survives or gets the axe.

In American law, scienter is about what a speaker knew when they said it. It’s all about a defendant's knowledge and mindset: When an exec says “things are great” or “margins are going to go way up,” did that exec know information which said things are awful or margins are falling? And that’s the challenging part about scienter, because proving someone’s state of mind – what they knew, what they believed, what they concealed -- is close to mind-reading sometimes.

So, let’s take a look at scienter, why it matters, and how courts have grappled with this issue.

Why It Matters

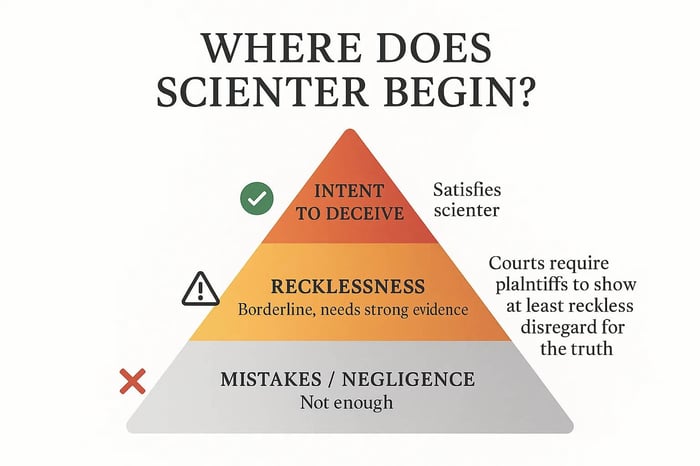

The Securities and Exchange Act of 1934 (the “Exchange Act”), Section 10(b), and SEC Rule 10b-5 set the rules for securities fraud cases. Among other things, those provisions require plaintiffs to show a significant stock drop or other lousy outcome that was more than just the result of poor business judgement or a business plan that didn’t pan out. Plaintiffs have got to show the company or its executives acted with "requisite scienter." That is, when those corporate executives were boasting about “things being great,” “massive margins,” or some other result, those executives had an intent to deceive investors, manipulate the market, or defraud. Or, lacking that explicit intent, plaintiffs have to show the executives acted with severe recklessness that borders on intent.

That’s a high bar to cross. Mistakes aren’t enough. Over-optimism isn’t enough. Even negligent misstatements aren’t enough. To win, plaintiffs must convince a judge (or jury) the company either knew the truth and said otherwise, or consciously disregarded red flags so obvious that not seeing them was effectively the same as lying.

Proving the scienter element can be a hiccup in a lot of cases. That’s why scienter is both the heart and the Achilles’ heel of securities law fraud litigation.

Let’s take a look, then, at how scienter played out in real-world litigation, as attorneys and judges grappled with proof of intent.

Case One: Scienter Proven—Tellabs, Inc. v. Makor Issues & Rights, Ltd.

For example, consider the Tellabs case as an instance when the courts grappled with evidence of intent versus corporate bluster. In the mid-2000s, communications company Tellabs was accused of painting an overly rosy picture about demand for its flagship product. Plaintiffs said Tellabs execs kept pushing a story about increased growth; meanwhile, internal reports showed demand was crumbling.

This case made it all the way to the Supreme Court because the parties disputed what counts as proof of scienter. The Court clarified what courts need to look for when weighing whether if scienter has been properly alleged.

The Supreme Court held that a securities fraud complaint must plead facts giving rise to a strong inference of scienter—an inference that is cogent and at least as compelling as any opposing inference of nonfraudulent intent

When the Seventh Circuit got the case back, the Circuit Court applied this standard. The Seventh Circuit found that the executives’ statements weren’t mere mistakes. The execs had access to detailed internal reports showing the gap between public messaging and private reality. Thus, the inference of intent to mislead, or deliberate ignorance, was stronger than the inference of mere carelessness, allowing plaintiffs to prevail on the motion to dismiss.

Takeaway: Scienter can be proven when plaintiffs show contemporaneous internal evidence contradicting executives’ public statements and conduct. It’s not enough to say “they should have known.” Plaintiffs need to show “they did know—or chose not to see.” (Tellabs, Inc. v. Makor Issues & Rights, Ltd., 551 U.S. 308 (2007).)

Case Two: Scienter Rebutted—Macomb County Employee Retirement Sys. v. Align Technology, Inc.

Not every case clears that bar: Align Technology is an example of when courts don't find requisite scienter. In 2020, Align Technology (the Invisalign company) faced a securities lawsuit. Plaintiffs argued Align misled investors about its growth prospects in China. The plaintiffs said Align’s executives must have had knowledge about slumping Chinese sales when they made those optimistic statements.

But the Ninth Circuit wasn’t convinced. The court found the statements were either non-actionable “puffery” (vague optimism) or did not create a false impression of growth. At most, the evidence showed optimism that turned out wrong. That might be bad corporate judgment, but bad decisions aren’t enough. Plaintiffs need to show specific intent to deceive or extreme recklessness with the truth.

The court stressed a point worth remembering: it’s not enough to allege that executives could have known, or should have known, or were in a position to know. Without specific facts showing deliberate fraud or reckless disregard, a securities case can’t move forward (though here, the court dismissed without reaching scienter).

Takeaway: Courts won’t infer scienter just because predictions didn’t pan out. Proving a securities fraud claim requires more than 20/20 hindsight and proof that results turned out badly. Winning a case requires proof of intent or recklessness at the moment the statements were made. (Macomb County Employees' Retirement System v. Align Technology, Inc., 39 F.4th 1092 (9th Cir. 2022).)

Case Three: What It Takes—Matrixx Initiatives, Inc. v. Siracusano

Then there’s the landmark case that shows what it really takes to plead scienter adequately. Matrixx Initiatives made a popular cold remedy called Zicam. Reports surfaced that some users lost their sense of smell after using it. Instead of being public about those reports, Matrixx executives kept touting the product and reassuring investors about growth.

Investors sued. Plaintiffs said that by ignoring and downplaying the adverse event reports, defendants had acted with scienter. The company countered that the reports weren’t statistically significant and thus not “material" nor indicative of wrongdoing.

This case also made it up to the Supreme Court. The Court took the investors’ side and held that the absence of statistically significant evidence does not preclude a finding of materiality, and scienter can be shown where executives were aware of potentially serious problems but concealed them (though the ruling centered on materiality, it allowed scienter allegations to proceed based on circumstantial evidence).

Takeaway: Scienter doesn’t require a smoking gun email admitting “we lied” (though that would definitely help!). Scienter can be shown through circumstantial evidence—patterns of concealment, knowledge of adverse facts, and deliberate decisions to keep investors in the dark. (Matrixx Initiatives, Inc. v. Siracusano, 563 U.S. 27 (2011).)

Why It’s So Hard

Here’s the hard truth: lawyers, judges, and juries can’t climb into executives’ heads. So we have to rely on circumstantial evidence: things like the timing of statements, access to contradictory information, insider stock sales, and deliberate avoidance of bad news. Those factors might help show defendants' knowledge of wrongdoing.

But those same facts often cut both ways. A stock sale might suggest intent, or it might just be routine. An optimistic projection might suggest fraud, or it might just be corporate culture. That ambiguity is why scienter is the gatekeeper: if plaintiffs can’t raise a strong inference of intent at the very beginning, the claim doesn’t even reach discovery.

Final Reflection

Scienter cases are, in a way, about trust broken at the deepest level. Many times, investors don’t sue just because numbers went bad – they sue because corporate executives said one thing so confidently and then the exact opposite thing happened. But the question becomes: was that just bad luck or was it an instance of corporate deceit?

And that’s why courts scrutinize scienter so closely. Securities law doesn’t punish bad luck. It punishes bad faith. Proving scienter is proving that gap: between what was known and what was said, between what was real and what was presented.

If securities law is built to keep markets honest, then scienter is its litmus test. Did the company play straight—or did it hide the ball?

Disclaimer: This article is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for advice on specific securities fraud matters.

You Can Also Read... |

![Alto Neuroscience, Inc. (ANRO) Securities Class Action Lawsuit [September 02, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/altoneuroscience-securities-lawsuit-blog-banner.webp)

![RxSight, Inc. (RXST) Securities Class Action Lawsuit Update [September 03, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/rxsight-securities-lawsuit-blog-banner.webp)