![Fly-E Group, Inc. (FLYE) Securities Class Action Lawsuit Update [December 4, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/flye-alert-plus-banner.webp)

Fly-E Group Promised to Dominate the Urban Mobility Sector, Investors Were Left Stranded

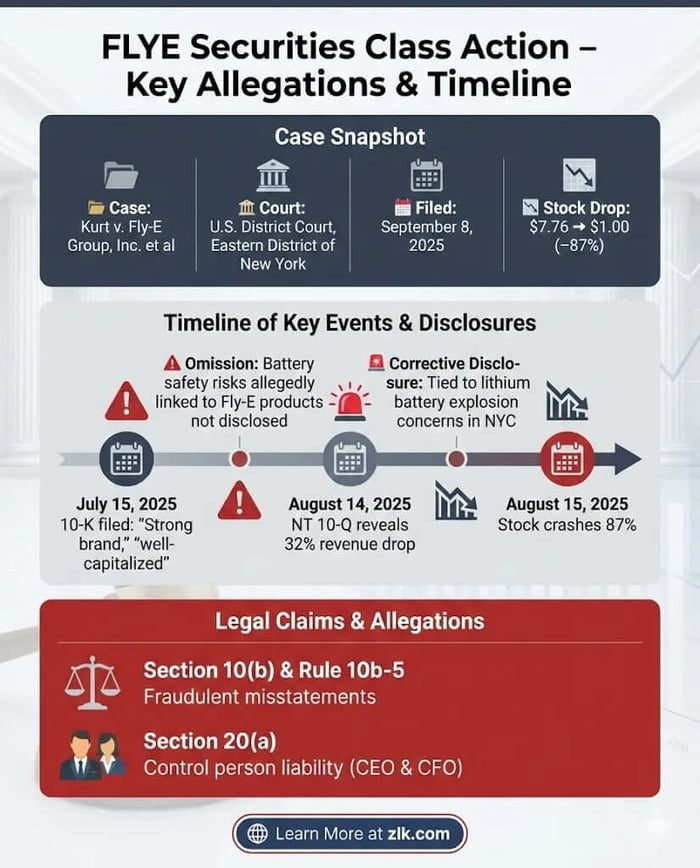

Caption: Kurt v. Fly-E Group, Inc. et al.

Case No.: 1:25-cv-05017

Jurisdiction: U.S. District Court, Eastern District of New York

Filed on: September 8, 2025

Class Period: July 15, 2025–August 14, 2025

Introduction

A federal securities class action has been filed against Fly-E Group, Inc. (FLYE) , a purveyor of electric bikes and scooters, alleging the Company and its top executives concealed material, adverse facts facts concerning the safety of Fly-E’s lithium battery. This lawsuit, filed on behalf of investors who purchased securities between July 15, 2025, and August 14, 2025 (the "Class Period") , posits a deceptive façade of robust growth that crumbled under the weight of undisclosed operational risks. The collapse was swift. When the truth emerged on August 14, 2025, the market delivered a verdict of its own, signaling devastating investor harm. This article explains the allegations, the business context, and the long-term implications for investors navigating the volatile electric vehicle (EV) industry.

Backdrop and Business Context

Fly-E Group is an electric vehicle company based in Flushing, New York, specializing in smart electric motorcycles, E-bikes, E-scooters, and related accessories under the Fly E-Bike brand across the United States, Mexico, and Canada. The Company carved out an early niche, primarily leveraging demand from the thriving E-commerce industry and, notably, serving food and package delivery workers in high-density urban areas like New York City.

The narrative of success was built on this "first mover advantage." Fly-E highlighted its strong brand reputation and innovative product pipeline, boasting over 67 new products launched since 2018. In June 2025, following a successful registered direct public offering , the Company felt "well-capitalized" to invest in inventory, vehicle production, and working capital. This perceived momentum set the stage for the alleged misstatements, painting a picture of market dominance just before the underlying reality was disclosed.

Promises Made vs. Reality

Throughout the Class Period, Fly-E management consistently presented a narrative of resilient growth, even while acknowledging sector-wide headwinds.

Promises Made (The Public Stance)

In its Form 10-K filed on July 15, 2025, the Company touted its "Our Strengths," which included its "Early Entry into the Market" and its "strong brand reputation for consistent delivery of high-quality EV products and excellent customer service."

Chief Executive Officer Zhou Ou reinforced this optimism in an accompanying press release: “We are positive about our growth prospects despite the dip in revenue caused by short-term external factors, as we have established solid reputation and continued to invest in marketing and product diversification." He further claimed the Company was "well-capitalized to invest in inventory, vehicle production, and working capital" , and that continued investment in safety, service, and innovation would prepare Fly-E for "sustained long-term growth." This was the explicit promise: a strong brand, ample capital, and a clear path to market leadership.

Reality (The Alleged Truth)

The complaint alleges that these positive representations were disseminated while concealing material adverse facts concerning the safety of Fly-E's own lithium battery. The core of the accusation is that Fly-E’s forecasting processes were inadequate, failing to account for the impact that specific, ongoing safety concerns were having on sales.

The misalignment came into stark relief on August 14, 2025, when the Company filed an NT 10-Q, stating that net revenue had decreased by a significant 32%. The crucial, and previously omitted, truth: the decline was "primarily driven by a decrease in total units sold" because customers were less inclined to purchase E-Bikes due to an "increasing number of lithium-battery explosion incidents in New York."

The reality, therefore, was not one of minor "short-term external factors" , but one where product safety issues—specific to the Fly-E experience, according to the lawsuit—were actively eroding customer demand and derailing revenue forecasts.

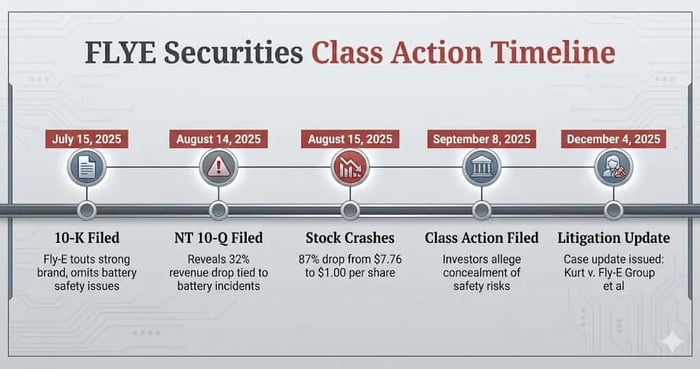

Timeline of Alleged Misconduct and Disclosures

The alleged misconduct is framed as a short, sharp period of optimistic reporting immediately followed by a catastrophic disclosure.

July 15, 2025: Fly-E files its Form 10-K, announcing financial results for the year ended March 31, 2025.

Alleged Misstatement: Management touts its "strong brand reputation" and plans to "Enhance our position as a leader in urban mobility." CEO Ou highlights an "improvement in gross margin" and expresses a "positive" outlook for "sustained long-term growth."

Omission: While mentioning a sector-wide revenue decrease due to "recent lithium battery accidents involving E-Bikes and E-Scooters," the filing allegedly failed to identify that the batteries involved in the incidents were Fly-E lithium batteries, thus minimizing the true, product-specific risk.

August 14, 2025: Fly-E files a form NT 10-Q (Notification of inability to timely file Form 10-Q) with the SEC.

Corrective Disclosure: The Company reveals a substantial 32% decrease in net revenue and attributes the decline to a decrease in units sold.

Truth Revealed: The decrease is tied to customers being "less inclined to purchase E-Bikes due to an increasing number of lithium-battery explosion incidents in New York."

August 15, 2025: The stock market reacts to the news.

Stock Price Reaction: FLYE stock plummets from a closing price of $7.76 on August 14, 2025, to $1.00 per share.

Investor Harm and Market Reaction

The disclosure on August 14, 2025, acted as the loss causation event, directly translating alleged misstatements into quantifiable investor harm.

The market’s reaction was immediate and brutal: Fly-E’s common stock declined by approximately 87% in a single day, falling from $7.76 to $1.00 per share. This dramatic price drop—a consequence of the market processing the truth that Fly-E's sales were being directly impaired by lithium battery safety incidents—quantifies the economic loss suffered by investors who had purchased shares at artificially inflated prices during the Class Period.

Litigation and Procedural Posture

The lawsuit, Kurt v. Fly-E Group, Inc. et al., is a federal securities class action filed in the United States District Court for the Eastern District of New York.

The Asserted Claims

The Plaintiff asserts claims under two main provisions of the Securities Exchange Act of 1934:

Section 10(b) and Rule 10b-5: This is the primary anti-fraud provision, alleging that the Defendants engaged in a scheme to deceive the market by making materially false and misleading statements and omissions.

Section 20(a): This claim asserts control person liability against the Individual Defendants—CEO Zhou Ou and CFO Shiwen Feng. Because of their senior positions, they allegedly "possessed the power and authority to control the contents of Fly-E’s reports" and thus exercised control over the Company’s alleged unlawful conduct.

The case hinges on the element of scienter (a state of mind signifying intent or knowledge of wrongdoing). The complaint alleges the Individual Defendants acted either knowingly or with reckless disregard for the truth. As officers with access to material non-public information, they allegedly "knew that the adverse facts [...] were being concealed from, the public" and that their positive representations were "materially false and/or misleading." The theory of "group-published" information liability is also invoked, stating the misstatements were the result of the collective actions of the Individual Defendants.

Shareholder Sentiment

The abrupt 87% stock drop sent a shockwave through the retail investor community, shifting sentiment from cautious optimism to outrage over alleged concealment.

Before Disclosure: Sentiment was largely focused on the potential for growth. Discussions across platforms like Stocktwits and Reddit (r/ebikes) centered on the "last-mile delivery story" and the perceived safety advantage Fly-E’s certified models had gained via the NYC trade-in program.

After Disclosure: The filing of the NT 10-Q sparked a furious reaction. The narrative changed from growth story to betrayal. Shareholders immediately demanded accountability, focusing their frustration on the CEO and CFO for their prior optimistic messaging.

The dominant trend in post-disclosure sentiment was a collective search for information, transitioning quickly to discussions about joining the securities class action and pursuing legal redress.

Analyst Commentary

Professional analyst opinion on Fly-E Group (FLYE) had been largely favorable or neutral prior to the NT 10-Q filing, emphasizing the company's competitive advantages in the last-mile delivery ecosystem and its participation in New York City's e-bike trade-in program as indicators of a "solidifying position" in urban mobility. Following the August 14, 2025 disclosure of the 32% revenue decline tied to lithium battery safety incidents, the consensus shifted dramatically toward caution and bearishness.

A report from AInvest highlighted the "perfect storm of operational and market challenges," noting that lithium-battery safety incidents and potential recalls could "erode consumer trust and trigger costly legal liabilities," positioning Fly-E as a high-risk bet in the EV retail sector with limited upside from pivots like rental services. Similarly, TradingView's analysis described the NT 10-Q as exposing a "safety cover-up" that undermined prior growth hype, with the 87% stock plunge reflecting investor realization of "existential product viability" risks beyond mere competition. TipRanks echoed this pivot, pointing to the company's failure to disclose ongoing battery investigations as a key factor in the year-to-date 84% stock loss, suggesting profound lapses in internal controls and forecasting.

Overall, post-disclosure commentary underscores a transition from optimism about Fly-E's niche in delivery-focused e-mobility to warnings of regulatory scrutiny and diminished market share due to unresolved safety flaws.

SEC Filings & Risk Factors

The allegations fundamentally stem from the contrast between the optimistic business outlook presented in SEC filings and the failure to adequately disclose product-specific risks.

The Company’s Form 10-K, filed on July 15, 2025, discussed the "Regulatory Landscape," noting the industry is "subject to extensive environmental, safety and other laws and regulations, which include products safety and testing, as well as battery safety and disposal." It even highlighted that its Fly-11 PRO model was chosen for a New York City Department of Transportation trade-in program to replace "unsafe e-bikes."

The core allegation is not that Fly-E failed to mention the industry risk, but that it failed to disclose the realized risk. The 10-K stated that net revenues had decreased by 21% for the prior year due to "recent lithium battery accidents involving E-Bikes and E-Scooters." Critically, the complaint alleges this disclosure obscured the material fact that the incidents were associated with Fly-E's own lithium batteries, creating a false sense that the risk was merely sector-wide, rather than company-specific.

The August 14, 2025 NT 10-Q, by explicitly linking the 32% revenue decrease to customer reaction against the "increasing number of lithium-battery explosion incidents in New York" , implicitly revealed that the prior risk disclosures were, at best, critically misleading and, at worst, an omission of a material fact.

Conclusion: Implications for Investors

The Fly-E Group securities class action offers a crucial, reflective takeaway for investors, particularly those engaged in emerging technology sectors like electric mobility and battery technology.

The primary lesson here is the chilling effect of realized risk, specifically regarding product safety. Investors must look past "lofty long-term projections" and scrutinize the nuance within risk factor disclosures. When a company attributes operational setbacks to vague "sector-wide" issues while promoting its own differentiated product quality, the dissonance should trigger deeper inquiry. The dramatic revenue decline and subsequent litigation show that an 87% loss in market capitalization is the cost of concealing an inherent, unmitigated flaw in the core technology.

This case has broader relevance for the entire EV and E-mobility sector. In a market where lithium battery safety is heavily regulated and often makes headlines, any company failing to adequately address, forecast, or disclose product-specific battery risks invites extreme market penalty and securities litigation. For investors, the FLYE securities class action is a stark reminder that a strong "Brand Reputation" means nothing if the underlying product is failing on its most critical promise: safety.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![CoreWeave, Inc. (CRWV) Securities Class Action Lawsuit Update [January 19, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/crwv-alert-plus-banner.webp)

![Bath & Body Works, Inc. (BBWI) Securities Class Action Lawsuit Update [January 19, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/bbwi-alert-plus-banner.webp)

![Vistagen Therapeutics, Inc. (VTGN) Securities Class Action Lawsuit Update [January 19, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/vtgn-alert-plus-banner.webp)