![Semler Scientific, Inc. (SMLR) Securities Class Action Lawsuit Update [December 4, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/smlr-alert-plus-banner.webp)

Semler Scientific Lawsuit: Did Omitted DOJ Investigation Mislead Investors?

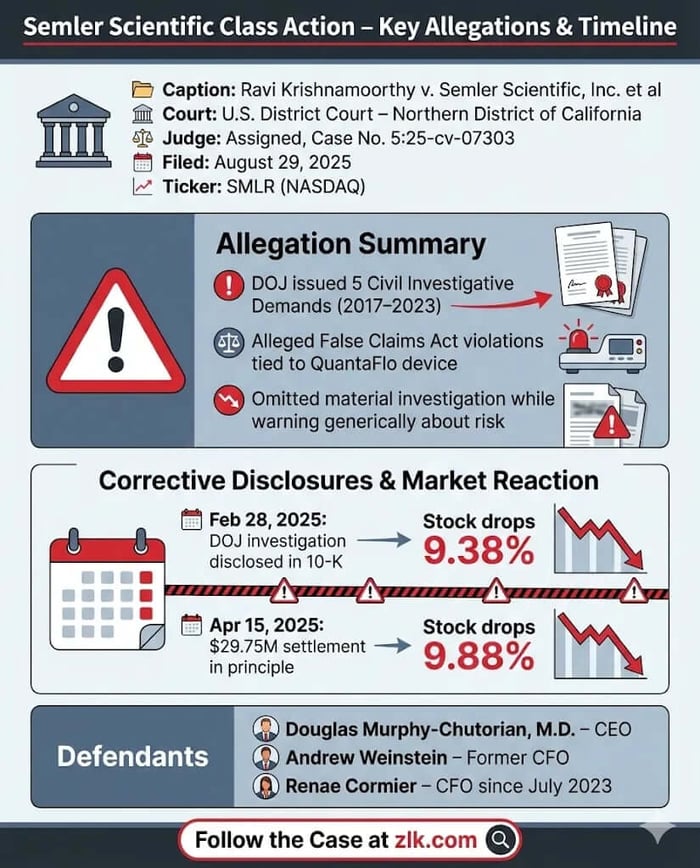

Caption: Ravi Krishnamoorthy v. Semler Scientific, Inc. et al.

Case No.: Case 5:25-cv-07303

Jurisdiction: U.S. District Court, Northern District of California

Filed on: August 29, 2025

Class Period: March 10, 2021–April 15, 2025

Introduction

Semler Scientific, Inc., a healthcare technology company that has notably branched into Bitcoin investing, is facing a securities class action lawsuit alleging that the company and its top executives knowingly concealed a material investigation by the U.S. Department of Justice (DOJ) into violations of the False Claims Act. The lawsuit, filed on behalf of investors who acquired Semler securities between March 10, 2021, and April 15, 2025 , claims that the omission of the DOJ Civil Investigative Demands (CIDs) rendered the Company's public risk disclosures about government scrutiny "materially false and misleading."

The legal action, brought in the United States District Court, Northern District of California (Case No: 5:25-cv-07303), centers on a fundamental question of corporate candor: How close must the government's hand be to the door before a company is required to disclose the knock? The resulting stock drops following the eventual disclosure and settlement announcement suggest investors believe the information was consequential.

Backdrop and Business Context

Semler Scientific (SMLR) describes itself as a company developing and marketing technology products and services to assist customers in evaluating and treating chronic diseases. Its flagship product, QuantaFlo , is an FDA-cleared device designed to measure arterial blood flow in the extremities to aid in the diagnosis of Peripheral Artery Disease (PAD).

An unusual dimension to this healthcare-focused business is the company’s adoption of Bitcoin as its "primary treasury reserve asset." The core healthcare technology solutions business is positioned as the predominant operational focus, generating the cash flows that enable the pursuit of its Bitcoin strategy. The company’s common stock trades on the NASDAQ Stock Market LLC under the ticker symbol SMLR

The operational setup that is central to the alleged misconduct involves the reimbursement practices for the use of QuantaFlo. The DOJ investigation specifically focused on whether the company violated the False Claims Act by marketing tests on devices using photoplethysmography technology as reimbursable by Medicare, allegedly in contravention of applicable laws and regulations. This is the fault line: a clinical device's profitability hinged on its regulatory compliance and reimbursement pathway.

Promises Made vs. Reality

Throughout the Class Period, Semler Scientific's annual reports on Form 10-K contained standard risk disclosures regarding healthcare regulations. In the 2020 Annual Report, for example, the company stated that its operations "may be subject to federal and state healthcare laws and regulations including fraud and abuse laws, such as anti-kickback and false claims laws." The filing further warned about the federal government's "increased its scrutiny of interactions between healthcare companies and healthcare providers" and the significant potential penalties for non-compliance, including "civil, criminal and administrative penalties, damages, fines, disgorgement, individual imprisonment, exclusion from participation as a supplier of product to beneficiaries covered by Medicare or Medicaid."

The reality, as revealed in the February 28, 2025, 2024 Annual Report, was that the risk was not hypothetical. The DOJ had already initiated a civil investigation demand (CID) in July 2017 , and subsequent CIDs had been received in February 2019, December 2021, April 2022, and April 2023.

The lawsuit alleges that by repeating the generic risk disclosures in the 2020, 2021, 2022, and 2023 Annual Reports—all while omitting the existence of the specific, ongoing DOJ investigation and multiple CIDs—the company was actively presenting a materially misleading picture to investors. The disclosure of a theoretical risk while an actual investigation was underway suggested a level of control and compliance that allegedly did not exist, a dissonance that struck at the heart of the company's operational integrity.

Timeline of Alleged Misconduct and Disclosures

July 2017: Semler Scientific receives an initial Civil Investigative Demand (CID) from the DOJ related to potential False Claims Act violations concerning the marketing of QuantaFlo tests as reimbursable by Medicare.

February 2019, December 2021, April 2022, April 2023: The company receives subsequent CIDs related to the same investigation, addressed to the Company or individual current or former employees.

March 10, 2021 – April 15, 2025 (Class Period): During this time, Semler Scientific files its annual reports (2020, 2021, 2022, and 2023 Annual Reports) containing general warnings about healthcare fraud and abuse laws, and DOJ scrutiny, but omits any mention of the specific, ongoing CID investigation.

February 28, 2025 (First Corrective Disclosure): After market hours, the company files its 2024 Annual Report on Form 10-K, finally disclosing the existence of the DOJ CID investigation dating back to 2017, the multiple subsequent CIDs, and the fact that the DOJ asked to engage in settlement discussions on February 6, 2025.

March 3, 2025 (Market Reaction): Following the initial disclosure, Semler Scientific stock fell $4.03, or 9.38%, closing at $38.89.

April 15, 2025 (Second Corrective Disclosure): After market close, the company files a Form 8-K disclosing that it had resumed settlement discussions with the DOJ and had reached an agreement in principle on a payment of $29.75 million to settle all claims.

April 16, 2025 (Market Reaction): Following the settlement news, Semler Scientific stock fell by $3.40 per share, or 9.88%, closing at $31.00.

August 29, 2025: The Class Action Complaint is filed.

Investor Harm and Market Reaction

The core of the investor harm centers on loss causation. Investors purchased Semler Scientific securities at prices that were allegedly artificially inflated because the Company's public statements on regulatory risk were incomplete and misleading. The stock price, it is argued, did not reflect the material contingency of an active, multi-year federal investigation with a substantial financial penalty looming.

The market’s reaction to the truth emerging was swift and punitive:

The initial disclosure of the investigation in the 2024 10-K triggered a drop of 9.38% on March 3, 2025, wiping out a significant portion of market capitalization as the risk moved from abstract to concrete.

The subsequent disclosure of the $29.75 million agreement in principle for settlement caused a further decline of 9.88% on April 16, 2025.

Collectively, these two disclosure events confirmed the gravity of the concealed operational risk and quantified the financial consequence, leading to significant compensable damages for the Plaintiff and other Class members.

Litigation and Procedural Posture

The lawsuit names Semler Scientific, Inc. and three key executives as defendants: Douglas Murphy-Chutorian, M.D. (CEO and Board Member); Andrew B. Weinstein (Senior Vice President, Finance and Accounting/Principal Financial Officer until July 2023); Renae Cormier (CFO since July 2023). The complaint asserts two primary legal claims:

Count I: Violation of Section 10(b) of The Exchange Act and Rule 10b-5 (Against All Defendants) : This count alleges that the defendants employed devices to defraud, made untrue statements of material facts, or omitted facts necessary to make the statements not misleading.

Count II: Violation of Section 20(a) of The Exchange Act (Against The Individual Defendants) : This count targets the Individual Defendants as "controlling persons" of Semler Scientific, alleging they were able to and did control the contents of the misleading public filings and thus share liability for the Company’s primary violations.

The lawsuit advances a strong scienter (intent to deceive) argument. The Individual Defendants are alleged to have had "actual knowledge of the material omissions and/or the falsity of the material statements" or to have acted with reckless disregard for the truth. The basis for this knowledge is their senior positions, direct participation in management, involvement in drafting and reviewing public statements, oversight of internal controls, and the signing of Sarbanes-Oxley (SOX) certifications. Specifically, the complaint notes that both the CEO and the then-Principal Financial Officer (Weinstein) signed SOX certifications for the 2020, 2021, and 2022 Annual Reports, attesting to the accuracy of financial reporting and disclosure of all fraud. The core of the scienter claim is that a multi-year DOJ investigation with multiple CIDs is a fact that cannot be ignored or simply forgotten when drafting risk disclosures.

Shareholder Sentiment

Prior to the corrective disclosures, shareholder sentiment on platforms like X/Twitter and Reddit focused on two distinct narratives: the promise of the QuantaFlo technology in chronic disease management and the speculative upside of the company's novel Bitcoin treasury strategy. The dual focus provided a unique investment profile, potentially drawing in both healthcare and cryptocurrency-focused funds and investors. Representative pre-disclosure commentary centered on the cash flow from the stable healthcare business being used to fuel Bitcoin accumulation, a perceived low-risk path to high-growth exposure.

The sentiment shift following the February and April 2025 disclosures was dramatic. The 9.38% and 9.88% stock drops turned investor commentary from speculative enthusiasm to anger and concern over corporate governance. Quotes and trends shifted rapidly to dismay that a risk of this magnitude was allowed to fester for years, suggesting that management had prioritized the 'Bitcoin story' over the underlying operational risks of the core healthcare business. Likewise, the $29.75 million settlement agreement was a tangible, non-recurring cost that directly impacted the balance sheet and future cash flows, leading to a "tax" on prior shareholder enthusiasm.

The prevailing post-disclosure sentiment was a loss of faith in management's transparency, leading to the rapid and decisive sell-off reflected in the stock price movements.

Analyst Commentary

Analyst coverage of Semler Scientific was complex due to the company's unique hybrid business model: a traditional healthcare revenue stream combined with an atypical treasury reserve in Bitcoin. Before the 2025 disclosures, analyst reports focused on the recurring revenue potential of QuantaFlo's fee structure and the company’s capital allocation strategy regarding its Bitcoin investment. Price targets were influenced by a valuation model balancing predictable medical device earnings with highly volatile cryptocurrency holdings.

The February and April 2025 disclosures forced a fundamental re-rating. Analyst reports included immediate downgrades/target price adjustments, especially related to the undisclosed DOJ investigation and the subsequent $29.75 million settlement, which introduced a massive, previously unmodeled liability. This non-operational, non-recurring cost directly reduced earnings projections and required a higher risk premium to be applied to the company's valuation.

The consensus pivoted from viewing Semler as an innovative Bitcoin proxy to a company with significant, undisclosed regulatory risk, a shift that justified the subsequent price declines.

SEC Filings & Risk Factors

Semler Scientific’s annual reports on Form 10-K during the Class Period—specifically the 2020, 2021, 2022, and 2023 filings—contained a section on healthcare law and regulation compliance, which is now central to the litigation. These filings detailed the inherent risks of operating in the healthcare sector:

Fraud and Abuse Laws: The company specifically warned about federal and state fraud and abuse laws, including anti-kickback and false claims laws.

False Claims Act: The risk factor section described the gravity of the civil False Claims Act, noting the prohibition against presenting a false or fraudulent claim for payment to the U.S. government and mentioning that the government is using it extensively to investigate healthcare providers.

Off-Label Promotion: The filings even warned that "off-label promotion has been pursued as a violation of the federal False Claims Act" and confirmed that the company is "prohibited from promoting products for such off-label uses."

The critical omission alleged by the lawsuit is that this highly detailed and accurate description of the theoretical risks was presented concurrently with the actual fact of an ongoing DOJ investigation into those very risks. The lawsuit argues the risk factor language was itself rendered misleading because it discussed the DOJ's scrutiny in the abstract, while omitting that the DOJ was already scrutinizing Semler. This created a disparity between the disclosed risk environment and the undisclosed operational reality, violating the essential purpose of risk factor disclosure.

Conclusion: Implications for Investors

The Semler Scientific case offers a pointed lesson in assessing the true meaning of risk factors in SEC filings. Investors, fund managers, and counsel are trained to look for risk—but this case illustrates the danger of a company using generic, standardized language to shield a specific, ongoing liability. A risk that has materialized into a Civil Investigative Demand is no longer a hypothetical risk; it is an undisclosed material operational event that can severely impact the value of a security.

For investors in the healthcare technology sector, the primary takeaway is to scrutinize regulatory disclosures for signs of unusual specificity—or, in this case, a compelling lack thereof. When a company's success relies heavily on Medicare/Medicaid reimbursement for a specific device or procedure, any hint of an undisclosed inquiry into compliance, even one that begins with a CID, should be viewed as a massive red flag. The $29.75 million settlement cost, which materialized after years of non-disclosure, is the price of that silence. This case reinforces that securities law demands more than mere technical compliance with disclosure rules; it requires material transparency on facts that a reasonable investor would consider important.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Ardent Health, Inc. (ARDT) Securities Class Action Lawsuit Update [January 13, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/ardt-alert-plus-banner.webp)

![Tronox Holdings Plc (TROX) Securities Class Action Lawsuit Update [November 28, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/trox-alert-plus-banner.webp)

![Varonis Systems, Inc. (VRNS) Securities Class Action Lawsuit Update [January 12, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/vrns-alert-plus-banner.webp)