![Tronox Holdings Plc (TROX) Securities Class Action Lawsuit Update [November 28, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/trox-alert-plus-banner.webp)

Investors Allege Tronox Misled Market on Pigment and Zircon Growth

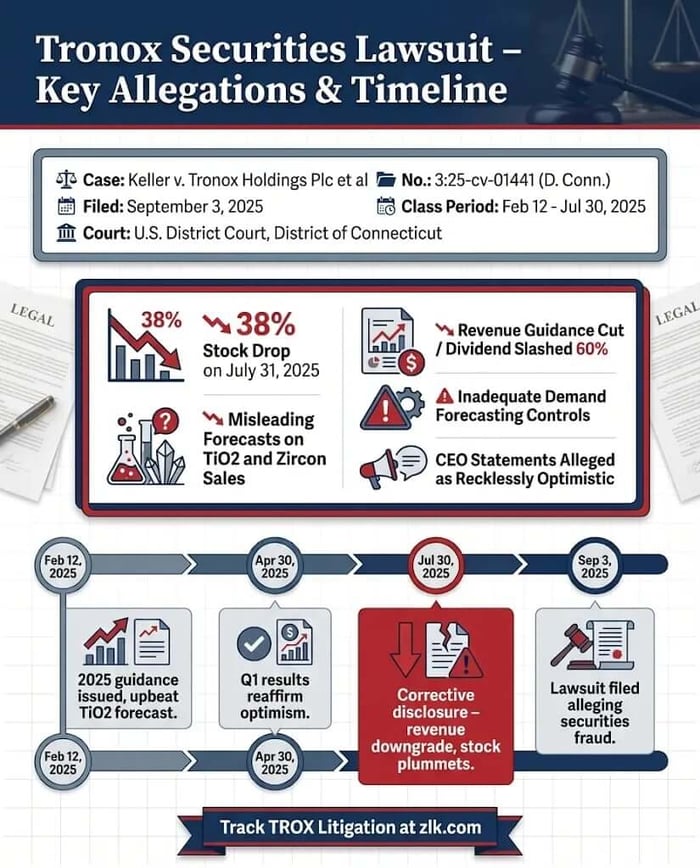

Caption: Keller v. Tronox Holdings Plc et al.

Case No.: Case 3:25-cv-01441

Jurisdiction: U.S. District Court, District of Connecticut

Filed on: September 3, 2025

Class Period: February 12, 2025 – July 30, 2025

Introduction

This securities class action, Keller v. Tronox Holdings Plc, et al., is a reckoning for investors who bought into the narrative of robust volume growth for titanium dioxide (TiO2) and zircon, only to watch that promise dissolve into a 38% single-day stock collapse. The lawsuit alleges that Tronox Holdings Plc (TROX) disseminated materially false and misleading statements about the strength of its commercial division and its ability to forecast product demand during the Class Period of February 12, 2025, through July 30, 2025. The triggering event was the Company’s July 30, 2025, announcement, which slashed full-year revenue guidance and drastically reduced the dividend, revealing that the demand for its core products was softer than anticipated.

Backdrop and Business Context

Tronox Holdings Plc is a United Kingdom corporation with its principal executive offices in Stamford, Connecticut, trading on the NYSE under the ticker TROX. The Company operates primarily in the chemical sector, mining titanium-bearing mineral sands and processing them to produce TiO2 products, zircon, and other specialty chemicals. TiO2 pigment is a foundational component used widely in paints, coatings, plastics, and paper, tethering Tronox’s financial performance closely to global construction and consumer discretionary spending cycles.

Leading up to the alleged misconduct, executives consistently framed the Company’s strategy around a significant cost savings plan—ranging from $125 million to $175 million in sustainable, run-rate improvements by the end of 2026—and the successful execution of its commercial strategy, particularly in regions subject to anti-dumping duties. This framework was the foundation upon which the Company built its lofty 2025 full-year revenue and Adjusted EBITDA guidance.

Promises Made vs. Reality

The disconnect between the Company’s public rhetoric and the alleged internal reality is the core of the investors’ complaint.

The Promises Made:

On February 12, 2025, the Company established its initial 2025 full-year guidance, projecting revenue between $3.0 and $3.4 billion and Adjusted EBITDA from $525 million to $625 million, driven by "improving TiO2 and zircon volumes."

CEO John D. Romano touted strong execution and commercial performance, stating that in the fourth quarter of 2024, "Zircon sales exceeded our previous guidance, driven by strong execution from our commercial group."

During the February 13, 2025 earnings call, Romano indicated an expectation for high single-digit volume growth for TiO2 moving into the first quarter of 2025. He also expressed confidence that pricing would "move as well" in the second half of the year, underscoring that the forecast was "not all based on volume."

Following the first quarter on April 30, 2025, Romano reiterated confidence, noting that TiO2 had realized a "stronger than normal seasonable demand uplift" sequentially.

The Reality Revealed:

The positive pronouncements contrasted sharply with the July 30, 2025, announcement revealing the truth of the Company’s commercial division. The complaint alleges that all this time, Tronox’s forecasting processes were inadequate, unable to appropriately anticipate or execute on demand.

The Company admitted to a significant reduction in TiO2 sales for the second quarter of fiscal 2025.

This decline was attributed to a "softer than anticipated coatings season and heightened competitive dynamics," a material fact that allegedly rendered earlier forecasts unknowably reckless.

The ultimate financial consequence was the lowering of the full-year revenue guidance and a dramatic 60% reduction in the dividend.

Timeline of Alleged Misconduct and Disclosures

A concise narrative highlights the causal chain from promise to alleged fraud:

February 12–13, 2025: Tronox issues Q4 FY24 results and full-year 2025 guidance of $3.0–3.4 billion in revenue. CEO Romano highlights strong execution in zircon and anticipates high single-digit TiO2 volume growth.

April 30–May 1, 2025: Tronox announces Q1 FY25 results, noting a "stronger than normal seasonable demand uplift" in TiO2 and confirms its full-year guidance. The Company emphasizes its cost control and anti-dumping advocacy as evidence of its ability to create "sustainable value." The stock price is artificially inflated by the sustained optimism.

July 30, 2025 (Corrective Disclosure): The Company announces Q2 FY25 financial results. It reveals a significant reduction in TiO2 sales volume, citing "weaker than usual seasonality across all regions" and macroeconomic pressures. The full-year financial outlook is lowered, and the dividend is cut by 60% to maintain liquidity.

July 31, 2025 (Market Reaction): The Company’s common stock price plummets from a close of $5.14 per share to $3.19 per share, a devastating decline of about 38% in a single trading day.

Investor Harm and Market Reaction

The disclosure on July 30, 2025, was a violent correction. Investor losses were quantified by the near-immediate evaporation of market capitalization, which accompanied the 38% stock drop. The price decrease was a direct consequence of the market internalizing the true operational and commercial risk that had allegedly been concealed: that Tronox’s demand forecasting was inadequate, sales were declining, and costs were increasing despite assurances of a "stronger" second half.

The market’s reaction was compounded by a cascade of analyst downgrades, which quickly tied the price drop to the specific disclosures of prolonged weakness.

Litigation and Procedural Posture

The class action, Maxwell Keller, Individually and on Behalf of All Others Similarly Situated, v. Tronox Holdings Plc, John D. Romano, and D. John Srivisal, was filed in the United States District Court for the District of Connecticut.

Legal Claims and Defendants:

The complaint asserts claims for violations of:

Section 10(b) of the Securities Exchange Act of 1934 and Rule 10b-5 promulgated thereunder, against all Defendants.

Section 20(a) of the Exchange Act, against the Individual Defendants.

The defendants include the Company, Tronox Holdings Plc, and two key executives: CEO John D. Romano and Senior Vice President and CFO D. John Srivisal.

Scienter and Control Person Allegations:

Scienter—the mental state implying an intent to deceive or a reckless disregard for the truth—is alleged based on the Individual Defendants' positions of control and access to internal, non-public information. The complaint avers that the Individual Defendants possessed the "power and authority to control the contents" of the Company's public statements and, because of their positions, "knew that the adverse facts specified herein had not been disclosed." This access to the underlying metrics of sales execution and forecasting failures is positioned as the basis for their knowing or reckless misconduct.

Shareholder Sentiment

The immediate and profound market plunge is perhaps the most eloquent testament to shareholder sentiment. A 38% one-day decline signifies not merely disappointment, but a profound loss of faith. The magnitude of the drop suggests widespread investor shock and a sense of betrayal, where the "strong execution" story became instantly untenable. Prior to the disclosure, sentiment was likely cautiously optimistic, driven by management's assurances of volume recovery and cost discipline. The subsequent dividend cut—a 60% reduction, described by management as necessary to "manage our liquidity through this longer downturn than we expected"—transforms this sentiment into anger. For retail and institutional investors relying on yield, this was the moment the Company moved from a growth narrative to a cautionary tale about capital preservation.

Analyst Commentary

Professional commentary quickly reflected the legal reality of loss causation. Following the July 30 disclosure, analysts moved swiftly to downgrade the Company’s prospects, revising models that had bought into the earlier optimistic outlook.

UBS immediately downgraded Tronox to a Neutral rating. Their rationale was a three-part indictment: "1) volumes/earnings remain more challenged near term, 2) we see a recovery further out than we previously expected, and 3) FCF/leverage remains more challenging in a weaker demand environment." Critically, UBS noted they now saw "minimal FCF over the next two years, and leverage in the ~5-7x range," pushing the timeline for attractiveness to 2027.

Truist Securities similarly slashed their price target. While acknowledging management’s hope for second-half TiO2 volume improvement driven by the Indian market, they specifically warned that this growth would likely "come at the expense of seq’l lower average realized prices." The downgrades crystallized the fact that the alleged misrepresentations had misled the entire financial community, not just individual investors, causing an immediate, uniform repricing of the stock.

SEC Filings & Risk Factors

While the specific 10-K or 10-Q risk factors are not fully detailed, the lawsuit itself serves as an exegesis on omitted risks. The core allegation asserts that the Company’s projections and statements were materially misleading because management failed to disclose the true state of its commercial division and the fact that its forecasting processes were inadequate.

In an SEC filing context, standard risk factors usually include macroeconomic volatility, competitive dynamics, and the cyclical nature of commodity prices. However, the complaint suggests the real, undisclosed risk was an internal control deficiency—specifically, the lack of a reliable process for predicting core product demand. The repeated claims of "strong execution" and "confidence" in achieving guidance functioned, in the plaintiffs’ view, to mask this internal inadequacy, turning typical business risks into active misstatements. The statutory safe harbor for forward-looking statements is alleged to be inapplicable, precisely because the statements were not accompanied by "meaningful cautionary statements" about the factors that were known to management, namely the deteriorating commercial reality.

Conclusion: Implications for Investors

According to the Complaint, this action concerns alleged misstatements and omissions regarding Tronox Holdings Plc’s demand forecasting capabilities, volume trends for titanium dioxide and zircon, and the reliability of its full-year 2025 financial guidance. Plaintiffs allege that, during the Class Period, defendants made positive statements about the Company’s commercial performance and outlook while failing to disclose material adverse facts relating to softer-than-anticipated demand conditions and deficiencies in forecasting processes.

The Complaint further alleges that these omissions rendered defendants’ public statements misleading and caused Tronox’s securities to trade at artificially inflated prices. When the Company disclosed reduced sales volumes, lowered its full-year guidance, and cut its dividend on July 30, 2025, plaintiffs allege that the market reacted negatively, resulting in significant losses to investors. The lawsuit seeks relief under Sections 10(b) and 20(a) of the Securities Exchange Act of 1934 on behalf of purchasers of Tronox securities during the Class Period

.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Ardent Health, Inc. (ARDT) Securities Class Action Lawsuit Update [January 13, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/ardt-alert-plus-banner.webp)

![Semler Scientific, Inc. (SMLR) Securities Class Action Lawsuit Update [December 4, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/smlr-alert-plus-banner.webp)

![Varonis Systems, Inc. (VRNS) Securities Class Action Lawsuit Update [January 12, 2026]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/vrns-alert-plus-banner.webp)