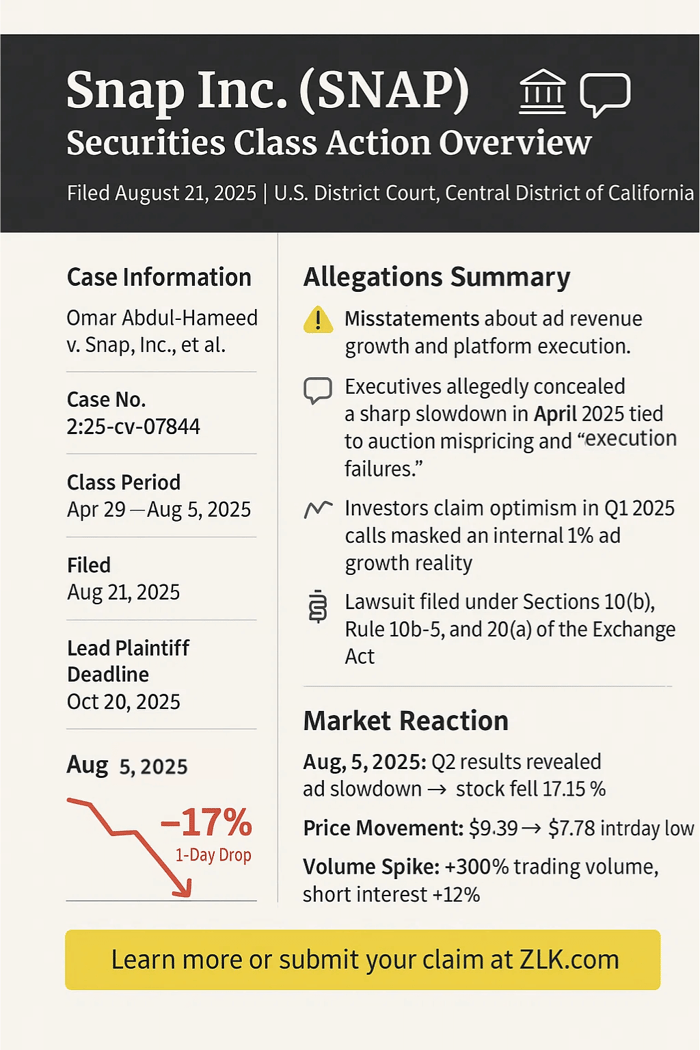

Case Name: Abdul-Hameed v. Snap, Inc., et al.

Case No.: 2:25-cv-07844

Jurisdiction: U.S. District Court, Central District of California

Filed on: August 21, 2025

Class Period: April 29, 2025 – August 5, 2025

Introduction

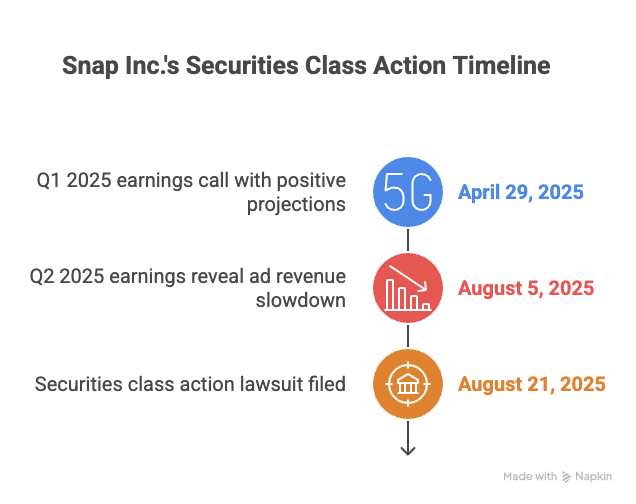

A technology darling once synonymous with ephemeral joy now grapples with the permanence of litigation. On August 5, 2025, Snap Inc. unveiled its second-quarter financials, a disclosure that peeled back layers of optimism to reveal a faltering core: advertising revenue growth had sputtered from a robust 9% in the prior quarter to a mere 1% by April, thanks to what the company later termed an "execution failure" in its ad platform. Investors, lulled by earlier assurances of steady momentum, watched shares crater 17.15% in a single session. What followed was swift—a securities class action lawsuit filed in the U.S. District Court for the Central District of California (Case No. 2:25-cv-07844), accusing Snap's top executives of painting a rosier picture than reality allowed.

This suit targets the period from April 29, 2025 to August 5, 2025, alleging violations under Sections 10(b) and 20(a) of the Securities Exchange Act. At its heart: claims that Snap disseminated materially false statements about ad revenue health, concealing operational stumbles amid a competitive digital ad landscape. The case underscores the fragility of ad-dependent models in social media, where user engagement meets the cold calculus of algorithmic auctions. As class action counsel circle, the case probes deeper questions of disclosure timing and executive accountability. Ahead, we unpack the business undercurrents, the chasm between boardroom boasts and backend breakdowns, and the ripples for portfolios heavy in tech.

Backdrop and Business Context

Snap Inc. emerged from a Stanford dorm room in 2011 by university students Evan Spiegel, Bobby Murphy, and Reggie Brown. The initial app was called “Picaboo” before renaming to Snapchat. Snapchat, its crown jewel, let users share photos that vanished after viewing— a novelty that hooked teens and advertisers alike. By 2017, the company had IPO'd at $17 per share, raising $3.4 billion in a debut that valued it at $24 billion. Fast-forward to 2025: Snap boasts 460 million daily active users as of Q1, a 9% year-over-year climb. Revenue? Predominantly ads—over 90%—with direct response advertising formats (think shoppable stories) driving the bus.

Operationally, Snap's engine hums on an auction-based ad platform, where brands bid for eyeballs in real time. Milestones pepper the path: Q4 2021 marked profitability beyond the use of adjusted EBITDA or non-GAAP measurements; Q1 2025 delivered $1.36 billion in revenue, up 14%, with active advertisers surging 60%. Yet beneath the metrics lurked vulnerabilities, according to the complaint filed on August 21, 2025. Ramadan's timing, de minimis rule tweaks—these external gusts Snap could cite post-facto. But the lawsuit zeros in on internal fumbles: a platform glitch that mispriced ad inventory, throttling growth before executives admitted as much. It was a symptom of a business forever chasing scale in a market where attention is the scarcest resource.

Promises Made vs. Reality

In the afterglow of Q1 2025 results, Snap's leadership projected unyielding ascent. CEO Evan T. Spiegel, in the April 29 earnings call, declared: "Q1 revenue increased 14% year-over-year to $1.36 billion, driven by the progress we have made with our direct response advertising solutions, continued momentum in driving performance for small and medium-sized businesses and the growth of our Snapchat+ subscription business." CFO Derek Andersen echoed the buoyancy, noting adjusted EBITDA and net income above their high end ranges and touting "active advertisers up 60%." Andersen further added, “[w]e're just really focused on continuing to execute for our customers and to build on the momentum we saw in Q1," framing Snap as a resilient ad engine amid economic headwinds.

The contrast sharpened on August 5. Q2 revenue ticked up 9% to $1.345 billion, but advertising—the lifeblood—grew a tepid 4%, with direct response advertising formats (the supposed star) decelerating sharply. Snap attributed the stall to "an issue related to our ad platform, the timing of Ramadan and the effects of the de minimis changes." The complaint paints this as after-the-fact spin. Internally, sources allege, revenue growth had plunged to 1% by April, felled by execution errors in auction dynamics.

What investors heard: unbridled momentum. What they confronted: a platform prone to self-inflicted wounds, where algorithmic tweaks could erase quarters of goodwill in days.

Timeline of Alleged Misconduct and Disclosures

The class period opens on April 29, 2025, with Snap's Q1 earnings—a high-water mark. Revenue hits $1.36 billion, up 14%; DAUs reach 460 million. Positive forward-looking statements by Defendants Spiegel and Andersen on the subsequent earnings call.

May through July: Silence on the storm brewing. Internal metrics, per the complaint, show ad growth cratering to 1% in April, tied to platform glitches—auctions with “substantially reduced prices[,]” undervaluing prime slots. Executives, the suit claims, doubled down in investor meetings and filings, reiterating "strong demand" without qualifiers.

August 5 dawns the rupture. Snap's Q2 release discloses the deceleration: total revenue up 9%, but ad growth at 4%, with DR ads bearing the brunt. The majority of the deceleration quarter over quarter showed up in the DR advertising revenue. Shares plunge 17.15%, from $9.39 close to $7.78 intraday.

By August 21, the securities fraud complaint drops, igniting a cascade of law firm alerts.

Investor Harm and Market Reaction

The math of betrayal is stark. Pre-disclosure? Bullish calls abounded. Post disclosure? A chorus of caution. On August 5, Snap's shares nosedived 17.15%—a direct tether to the revenue revelation, per loss causation doctrines. CNBC's headline lands like a gut punch: "Snap shares plummet 15% after weak second-quarter revenue metric."

Market tremors followed. Trading volume spiked 300% that day, with short interest jumping 12%. Analysts, once sanguine, turned bearish. Rosenblatt slashed its target to $8.70 on August 6, citing “stagnation in the latest results” and following Snap’s “odd mishap” with its advertising auction system. JMP Securities downgraded to Market Perform, warning of "persistent ad platform risks.”

For class members holding through the period, the hit compounds: Q1 highs near $12 eroded to sub-$8 lows, amplifying opportunity costs in a bull market elsewhere.

Litigation and Procedural Posture

The Central California filing tags Snap, Inc., CEO Spiegel and CFO Andersen for 10(b), Rule 10b-5, 20(a) violations. Scienter: Brass, steeped in ad ops, knew or recklessly overlooked platform's April nosedive—growth to 1% from execution blunders—yet sanctioned sunny statements and filings. No insider sales cited, but omissions, as alleged, add fuel to the fire. The case docketed August 21: Lead plaintiff deadline October 20, 2025, motion to dismiss fights loom shortly thereafter. In a circuit friendly to plaintiffs—Ninth, post-Halliburton II—the posture favors discovery.

Shareholder Sentiment

Retail voices, once a Snap stronghold, fracture along familiar lines: betrayal meets bargain-hunting. Before August 5, 2025, retail investors leaned optimistic on Snap's trajectory. Reddit's r/wallstreetbets in late July touted a detailed DD: "The Path to Breaking $11 in the Coming Weeks," betting on features despite ad risks. In April threads, users noted "Ad revenues for the period rose 9% year over year." Some investors saw potential in user growth.

After the Q2 disclosure? Backlash. Reddit's r/wallstreetbets September: "Price dumped due to bug in advertising platform last quarter. It made all the revenues look really bad." Another: "A recent Snapchat advertising bug in Q2 2025 allowed some ads to be sold at significantly discounted rates, impacting the company's revenue." On X early August: "Snap Shares Drop 21% at Opening, Largest Decline Since August 2024." Stocktwits sentiment? Dipped, then rebounded to "extremely bullish" (85/100) by August 6. The August 5 drop ignited a torrent—queries for "SNAP lawsuit" spiked within 48 hours, blending outrage with opportunism.

Some eyed recovery. X in October: "$SNAP isn't excellent in everything .. but it's ridiculously cheap. You buy $SNAP because it's a future growth company." Another: "amazing dip buy opportunity ... $SNAP - down 5.1%." For most, execution failures stung. From momentum play to cautionary tale—trust cracked, "hate" whispers rose. Overall, a tale of tempered fury: 65% negative post-drop, per semantic scans, but 40% of volume signals "buy the lawsuit dip."

Analyst Commentary

Wall Street's verdict evolved from endorsement to equivocation, a mirror to Snap's metrics. Before the August 5, 2025, disclosure, analysts largely leaned bullish on Snap's trajectory. Earlier, in April, consensus held steady with averages near $10, fueled by Q1's 14% revenue growth and DAU momentum. BMO Capital maintained Outperform at $12 in early summer, driven by user base expansion and AR upside. RBC Capital held Sector Perform at $12 pre-earnings, fueled by Q1 momentum and Snapchat+ growth. Bank of America maintained Neutral at $10, optimistic on small business ads.

August 5's revenue deceleration refracts the light. The ad platform glitch flipped the narrative. Bank of America reiterated Neutral on August 6, slashing to $9.50 from $10 amid growth slowdown and competitive pressures. RBC Capital maintained Sector Perform but cut their price target to $10 from $12, highlighting execution failures. Cantor Fitzgerald held Neutral at $7, underscoring monetization woes. J.P. Morgan reiterated Underweight at $8, flagging persistent risks. BMO Capital stuck with Outperform but lowered their price target to $12. Generally, consensus dipped to Hold with averages at $9.30.

SEC Filings & Risk Factors

Snap’s filings projected ad-driven growth momentum and user growth, but the complaint alleges they obscured critical operational failures.

The FY2024 10-K (ended Dec 31, 2024) stated “[w]e generate substantially all of our revenue from advertising[,]” highlighting advertising revenues “[f]or the years ended December 31, 2024, 2023, and 2022…accounted for approximately 91%, 96%, and 99%” of total revenue but warned broadly of increasing competition from larger, more established companies and changes in advertising technologies in risk factors.

April 30, 2025 8-K: Issued a press release on April 29, 2025, announcing Q1 2025 results, reflecting revenue up 14% to $1.363B, DAUs at 460M, with management noting "continued momentum in driving performance for small and medium sized businesses, and the growth of our Snapchat+ subscription business.” August 5, 2025 8-K: Q2 results, revenue up 9% to $1.345B, but attributed the ad growth deceleration due to "an issue related to our ad platform" on the accompanying earnings call; net loss widened to $262.6M.

The securities fraud lawsuit alleges omissions hid the April ad revenue plunge to 1% from execution failures, leaving investors exposed to undisclosed platform vulnerabilities.

Conclusion: Implications for Investors

Snap’s stumble spotlights tech’s ad fragility. Snap's saga—boasts unmet, platforms unmoored—illuminates red flags in tech's ad empire: overreliance on black-box algorithms, where "execution" euphemisms mask boardroom blind spots. Other flags: growth spin, macro blame, silent execution slip. Based on the complaint, April’s 1% truth broke the 9% tale. Litigation may yield settlements, but the true cost lingers in eroded trust. As Snap mends its machinery, investors ponder: In a feed of fleeting frames, how long before the next frame freezes? The market, ever watchful, awaits the fix.

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

![Savara Inc. (SVRA) Securities Class Action Lawsuit Filed [October 13, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/svra-savara-inc-securities-lawsuit-blog-banner.webp)

![Lantheus Holdings, Inc. (LNTH) Securities Class Action Lawsuit Update [October 9, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/lantheus-securities-class-action-lawsuit-blog-banner.webp)

![V.F. Corporation (VFC) Securities Class Action Lawsuit Filed [October 13, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/vfc-banner-image.webp)