Table of Contents

- Introduction

- A Call, But Not Just a Call

- What Actually Happens on an Earnings Call?

- Why Should You Care?

- Legal Reality: The Microphone Carries Weight

- Real Cases Where the Call Was the Catalyst

- What to Listen For (Even If You're Not a Finance Pro)

- You Don’t Have to Listen Live to Be Paying Attention

- Final Thought: The Script Isn’t Just PR

Introduction

Every quarter, without much fanfare, public companies open a line into their inner-workings. Company execs dial into a scheduled call and tell the world how the company’s doing. Sometimes, though, these calls are more than just a “review of numbers,” because something comes out that says “things aren’t right.”

These are earnings calls: the quarterly ritual where CEOs and CFOs walk analysts and investors through the numbers, field questions, and (sometimes) reveal more than they intend. It’s like the world’s most technical show-and-tell. But instead of glue sticks and poster boards, the props are balance sheets, growth forecasts, and verbal cues parsed like poetry.

For shareholders, these calls are front-row seats to a performance that can move markets . . . or, sometimes, set lawsuits in motion.

A Call, But Not Just a Call

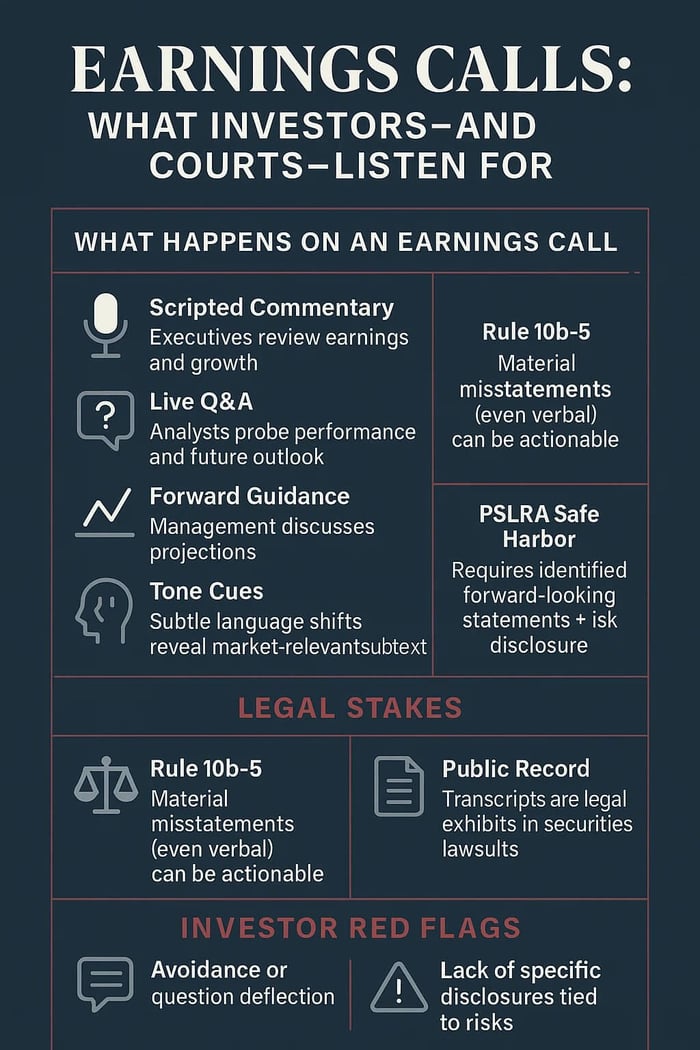

Earnings calls typically happen after a company releases its quarterly earnings results, often through a press release furnished to the SEC on Form 8-K. The full quarterly (10-Q) or annual (10-K) filings, with detailed financial statements, are submitted later. Those filings are pretty much all numbers and corporate speak: revenue, profits, segments, risks. They're formal, dry, and the sort of thing that puts most investors to sleep.

The call is different.

It’s a livestreamed conversation, when the company’s big wigs explain what those numbers really mean. They’ll highlight good news, play spin doctor with the bad, and sometimes slip into optimism that sounds more like a wish than finance. Note that forward-looking statements (e.g., growth forecasts) may be protected under the Private Securities Litigation Reform Act’s (PSLRA) safe harbor if properly identified and accompanied by cautionary language about risks. Analysts ask questions. There’s a script at first. Then, it gets real.

What gets revealed isn’t always in what’s said. It’s in how it’s said. And, sometimes, it’s in what isn’t said. That’s why these calls matter: they provide the close-up view to what’s really going on, as told by the executives themselves.

What Actually Happens on an Earnings Call?

Many of these calls are sleepy, scripted, and full of corporate babble.

You’ll usually hear:

- An overview of key financial results

- Comments on what’s driving performance—good or bad

- Forward-looking statements: where they think things are going

- A Q&A with analysts that either clarifies or muddies the waters

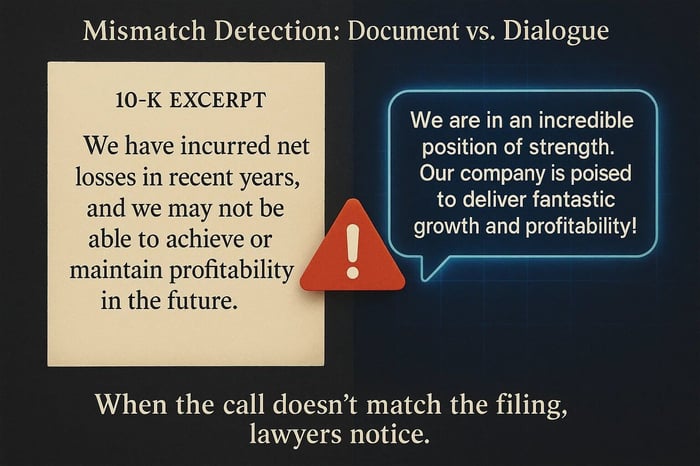

Sometimes, though, the numbers don’t add up or the story given doesn’t match up with reality or the story’s totally changed from last time.

Sometimes, those questions hit nerves. Sometimes, executives fumble through them. And sometimes, the real story is buried in the language—phrases like “uncertain outlook” or “temporary softness” that sound innocuous but aren’t.

It’s not theater. But it is performance. And the market reacts accordingly.

Why Should You Care?

Because the numbers in the earnings release might tell you where a company is. But the call tells you what leadership wants you to believe happens next. That’s a subtle but crucial difference.

A company might beat revenue expectations—but lower guidance for next quarter. They might spin a loss as a strategic investment. Or downplay risks that only show up weeks later, when the stock drops and someone finally files suit.

If you're watching, the signs are usually there. The catch is: most people aren’t watching.

While misleading statements can lead to liability, successful claims require proving scienter—a deliberate intent to deceive or extreme recklessness—not just optimism or poor forecasting.

Legal Reality: The Microphone Carries Weight

Here’s where it stops being soft. Under U.S. securities law, public companies can’t make false or misleading statements of material fact—not in SEC filings, not in press releases, and not during earnings calls.

That means a CEO who exaggerates on a call isn’t just being optimistic. If their words create an inflated view of the company’s condition—and investors act on that view—it can become a basis for securities fraud litigation under Section 10(b) and Rule 10b-5. Liability generally requires scienter (intent to deceive or reckless disregard for the truth), materiality, reliance, and loss causation, as pleaded with particularity under the PSLRA.

This isn't theoretical. It happens. And courts take it seriously.

Real Cases Where the Call Was the Catalyst

Let’s talk specifics. These aren’t law school hypotheticals—they’re real cases with real money lost.

Toll Brothers

In City of Hialeah Employees’ Retirement System v. Toll Brothers, 2008 WL 4058690 (E.D. Pa. 2008), executives painted a positive picture during earnings calls. The market responded. But internally, the company knew demand for new homes was weakening. When that reality caught up with the narrative, the stock fell—and shareholders sued.

The court didn’t toss the case. Why? Because the gap between internal knowledge and public tone during the calls raised serious questions. That’s how the call became part of the legal record.

The case later settled for $25 million in 2010.

Nvidia

In In re Nvidia Securities Litigation, 768 F.3d 1046 (9th Cir. 2014), management allegedly failed to disclose known defects in certain graphics processing units and media processors, making statements about growth and performance misleading. Behind the scenes, internal reports indicated product failures and potential costs.

The Ninth Circuit affirmed the dismissal of the case, finding insufficient allegations of scienter, but the allegations highlighted how undisclosed issues can underpin fraud claims.

What they said—out loud, on the record—mattered. The thread between these cases is clear: if what’s said on the call doesn’t match reality, that mismatch can become a claim.

What to Listen For (Even If You're Not a Finance Pro)

You don’t need to be an analyst to pick up on red flags. Honestly, sometimes that helps.

Here’s what sharp listeners catch:

- When an executive pivots away from specifics after being asked twice

- When the tone goes flat during a question about future cash flow

- When “short-term volatility” becomes the answer to everything

- When forward-looking comments lack accompanying risk disclosures, potentially losing safe harbor protection

Buzzwords like “macro headwinds” or “strategic realignment” often hide more than they reveal. And the more those phrases show up, the more you should wonder: what aren’t they saying?

Also: compare what’s said on the call to what’s written in the 10-Q or 10-K. If something feels off—if risks are minimized in speech but fully laid out in print—that inconsistency matters. Not just ethically. Legally.

You Don’t Have to Listen Live to Be Paying Attention

Let’s be real: most people aren’t going to stream an hour-long earnings call during lunch. That’s fine. The transcripts exist. So do the summaries. So do the headlines that ripple out afterward.

But if you're an investor—especially one who’s lost money—you should know that the call transcript might be more important than the financials.

Why? Because tone and content can push a stock price up. And when it falls later, what was said on the call might help explain why.

That’s how lawyers think. That’s how courts think. And it’s how some of the strongest shareholder lawsuits start: not with the numbers, but with how the numbers were framed.

Final Thought: The Script Isn’t Just PR

It’s easy to dismiss earnings calls as fluff. As canned talking points. As spin.

But courts don’t see it that way.

When executives speak—especially when they improvise—they're still bound by the rules. If they mislead investors, even with the best intentions, those words carry legal weight. And those transcripts? They don’t disappear.

So even if you don’t tune in, remember this: the call happened. The statements were made. And someone—somewhere—is reading every word of it, looking for the gap between what was said and what was true.

Because sometimes, the story that moves markets is told in real time—and later, it’s told again in court. That said, the vast majority of earnings calls are routine and compliant, with courts often dismissing unsubstantiated claims due to high pleading standards.

![iRobot Corporation (IRBT) Securities Class Action Lawsuit Update [August 15, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/irobot-securities-lawsuit-blog-banner.webp)

![Rocket Pharmaceuticals, Inc. (RCKT) Securities Class Action Lawsuit Update [July 16, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/rocket-pharma-rckt-securities-lawsuit-blog-banner.webp)