![DeFi Technologies Inc. (DEFT) Securities Class Action Lawsuit Update [December 8, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/deft-alert-plus-banner.webp)

The Arbitrage Trap: Investors Allege DeFi Technologies Misled Markets on Core Revenue Strategy

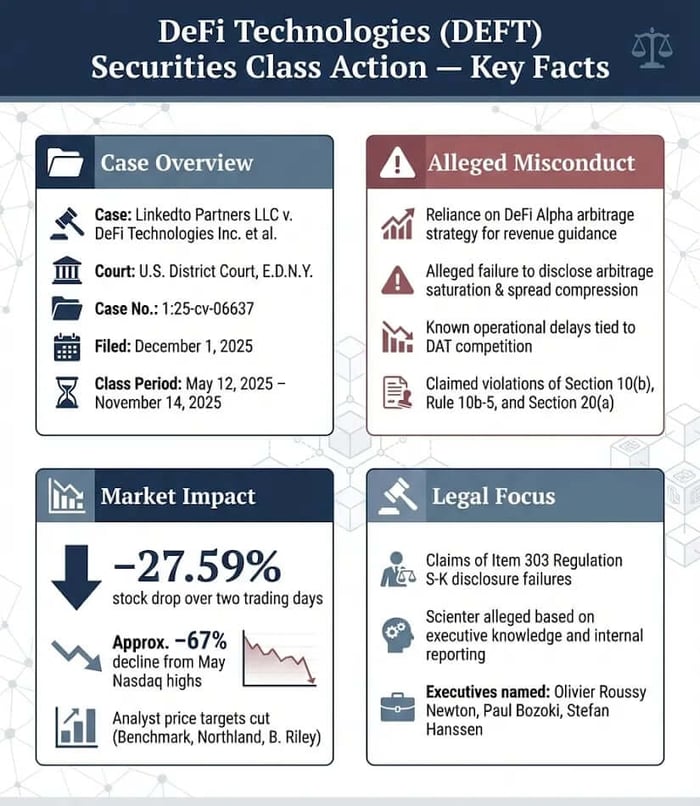

Case Name: Linkedto Partners LLC v. DeFi Technologies Inc. et al.

Case No.: 1:25-cv-06637

Jurisdiction: U.S. District Court, Eastern District of New York

Filed on: December 1, 2025

Class Period: May 12, 2025—November 14, 2025

Introduction

Red flags fly highest just after the ship sinks, and for investors in DeFi Technologies Inc. (DEFT), the wreck of a dramatic revenue guidance cut has led directly to a federal securities class action lawsuit. The core allegation centers on the company’s repeated representations regarding its proprietary DeFi Alpha arbitrage trading strategy. Investors allege that while executives, including CEO Olivier Roussy Newton and CFO Paul Bozoki, touted the strategy as a reliable source of revenue, they failed to disclose critical, known operational trends that had already begun to choke off the profits. This legal challenge covers the period from May 12, 2025, through November 14, 2025, marking the span when the market was allegedly misled about the true financial health of the digital asset company. The lawsuit, filed by lead plaintiff Linkedto Partners LLC in the US District Court for the Eastern District of New York, was triggered by two sharp corrective disclosures that collectively saw the stock price plummet, translating directly into significant investor harm.

Backdrop and Business Context

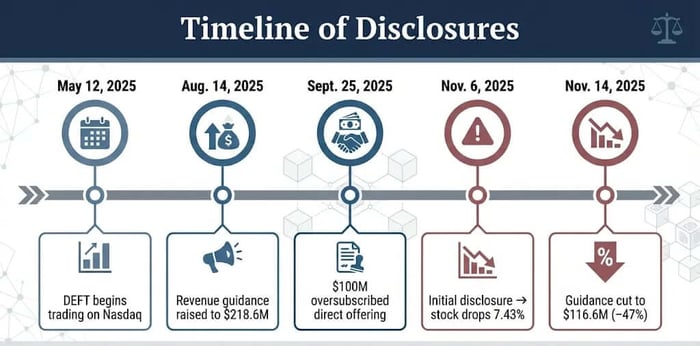

DeFi Technologies Inc. operates as a financial technology company, positioning itself as a key bridge between traditional capital markets and the burgeoning decentralized finance (DeFi) sector. The company's operations are divided primarily between its Valour subsidiary—an issuer of digital asset exchange-traded products (ETPs) in Europe—and its internal digital asset treasury and trading functions, which include the DeFi Alpha arbitrage desk. The company's shares began trading on the Nasdaq Capital Market under the ticker DEFT on May 12, 2025, a notable milestone intended to enhance visibility and liquidity.

The backdrop to the alleged misconduct lies in the aggressive growth strategy and reliance on the DeFi Alpha desk to generate substantial revenue, particularly after the company raised approximately $100 million in an oversubscribed direct offering announced on September 25, 2025. The success of this arbitrage strategy—trading on price differentials across digital asset exchanges—was pitched as central to the company’s ability to meet its ambitious guidance. It was a mechanism meant to provide consistent, high-yield returns, distinguishing DEFT from simpler cryptocurrency investment vehicles.

Promises Made vs. Reality

The claims of misrepresentation lie in the chasm between the company's optimistic public pronouncements and the alleged operational reality.

In its public filings and statements during the Class Period, DeFi Technologies projected confidence, backed by a significant $218.6 million annualized operating revenue guidance for 2025. This figure heavily relied on the continued high performance of the DeFi Alpha strategy. Management, including the named key executives Olivier Roussy Newton, Paul Bozoki, and Stefan Hanssen, suggested the company was structurally and financially prepared for market volatility.

The reality, as later acknowledged by the company, was starkly different. The complaint alleges that the company had failed to disclose that the DeFi Alpha arbitrage opportunities were facing a critical delay in execution. The key problem was an issue of saturation: the proliferation of digital asset treasury (DAT) companies entering the same market had consolidated digital asset prices and sharply compressed the available trading spreads. The aggressive guidance was already unlikely to be met, a known trend that investors claim was omitted in violation of Item 303 of Regulation S-K.

Timeline of Alleged Misconduct and Disclosures

The narrative flow of the case charts a causal chain from alleged omission to market correction.

May 12, 2025: DeFi Technologies begins trading on the Nasdaq under the ticker DEFT. The Class Period begins, during which the company allegedly maintains misleading revenue expectations predicated on the strong, yet increasingly constrained, DeFi Alpha strategy.

May 14, 2025: The company's Q1 2025 press release claimed DeFi Alpha had an "unblemished track record," cited C$132.1 million in 2024 gains with "zero losses to date." That same day, Newton projected full-year 2025 revenue of approximately C$285.6 million (US$201.07 million).

August 14, 2025: Newton told investors that "Q2 2025 was proof that our model executes in a softer market," praised DeFi Alpha's "low-risk opportunities," and raised annualized 2025 operating revenue guidance to US$218.6 million.

September 25, 2025: The company announces an oversubscribed $100 million direct offering. The complaint suggests that the undisclosed operational headwinds made the company’s valuation artificially inflated at the time of this capital raise.

November 6, 2025: The company issues an initial partial disclosure regarding the issues facing its trading activities. The market immediately registers the concern, and the stock price drops by 7.43%, or $0.13 per share, closing at $1.62.

November 14, 2025: The company announces its Q3 2025 financial results and, more importantly, a shocking cut to its 2025 revenue forecast. The full-year revenue guidance is slashed by approximately 47%, from $218.6 million to $116.6 million, explicitly attributing the failure to the "delay in executing DeFi Alpha arbitrage opportunities as a result of the proliferation of digital asset treasury companies and the consolidation of digital asset prices." The company acknowledged that the expected $102 million of DeFi Alpha-related revenues will be deferred.

Investor Harm and Market Reaction

The corrective disclosures created a fiscal reckoning. The Class Period ended with the definitive revelation of the core business problem. The impact was severe and immediate.

The most catastrophic reaction occurred after the November 14 announcement: the stock price fell 27.59%, or $0.40 per share, over the subsequent two trading sessions, closing at $1.05 on November 17, 2025. For investors who had held shares since the Nasdaq uplisting in May 2025, the decline represented a loss of approximately 67%.

The massive guidance cut triggered a wave of downgrades and price target reductions from professional analysts, tying the price drops directly to the loss of confidence in the company’s core revenue engine.

Litigation and Procedural Posture

The lawsuit, Linkedto Partners LLC v. DeFi Technologies Inc., et al., is proceeding in the US District Court for the Eastern District of New York under Case No. 1:25-cv-06637.

The complaint asserts claims under the following sections of the Securities Exchange Act of 1934:

Section 10(b) and Rule 10b-5, the primary anti-fraud provisions, alleging that the Defendants made material misstatements and omissions.

Section 20(a), which asserts "control person" liability against the key executives Olivier Roussy Newton, Paul Bozoki, and Stefan Hanssen, on the grounds that they possessed the authority to control the company's public statements.

The key to the litigation will be establishing scienter, or the Defendants’ state of mind. The complaint summarizes the scienter allegations by noting that the Executives would have known of the deteriorating operational trends—the competition and pricing consolidation—through their direct roles and internal reporting. The alleged motive centers on the company successfully completing its $100 million direct offering during the Class Period at a supposedly inflated stock price.

Shareholder Sentiment

DeFi Technologies (NASDAQ: DEFT) shareholder sentiment on social media has plummeted from pre-November optimism to outright frustration and skepticism following the November 14, 2025, revenue guidance slash—from $218.6 million to $116.6 million—blamed on DeFi Alpha arbitrage delays from surging digital asset treasury (DAT) competition. The December 1, 2025, class action lawsuit filing amplified the backlash, with retail investors on X (formerly Twitter) and Stocktwits decrying the 67% stock plunge from May Nasdaq highs to $1.05 by November 17.

On X, sentiment skews bearish, with users venting about the "arbitrage trap" and lawsuit's implications. Retail traders mock the lead plaintiff threshold of $100K+ losses as a "nothingburger," predicting the case fizzles without big fish. One user quipped, "Hahaha this 100% screams the lawsuit won’t go anywhere [...] only if it’s worth their time. Moving on." Some posts lament DEFT's outsized drops versus peers during crypto dips, with one investor noting, "$DEFT falls more sharply than DAT companies when cryptocurrency prices decline, and rises significantly less [...] Management's share buybacks were too small and actually backfired." High short interest (over 35% in August) fuels fears of further squeezes.

Stocktwits mirrors this gloom, with sentiment gauges hitting "extreme bearish" post-cut, per real-time chatter on DEFT's page—traders pile on about the 27.59% two-day crash and Q3 revenue miss (down 20% YoY). Reddit's r/ValueInvesting threads from August show early hype around the $218M guidance, but November updates reflect regret, with comments like "Deft has a lot of promise but short interest is on the rise—passed 35% this week," evolving into post-lawsuit doubts on recovery.

Analyst Commentary

The volatility surrounding DeFi Technologies led to a sharp, immediate re-rating across the professional analyst community, particularly following the November 14 guidance cut.

Before the disclosure, the overall consensus for the company was overwhelmingly positive, with multiple firms maintaining a "Buy" or "Strong Buy" rating and aggressive price targets. However, the revelation that the core DeFi Alpha trading strategy had effectively stalled triggered a cascade of target price reductions that painted a clearer picture of the risk investors had been taking.

Benchmark cut its price target most dramatically, lowering it to $3.00 from $8.00 on November 21, 2025.

Northland Securities also slashed their targets, bringing them down to $1.79 in the days following the disclosure.

B. Riley adjusted its target down to a mere $1.60 from $3.00, confirming the market’s realization that the company’s previous projections were unsustainable.

Despite the dramatic cuts, the fundamental rating often remained "Buy," suggesting analysts still saw value in the company’s core asset management (Valour ETPs) business, but recognized the substantial risk and failure in the high-yield trading segment.

SEC Filings & Risk Factors

The class action fundamentally argues that the company's SEC filings were not just inaccurate, but materially incomplete. The core of this claim rests on the requirements of Item 303 of Regulation S-K, which compels companies to disclose "known trends, demands, commitments, events or uncertainties" that are reasonably likely to have a material effect on financial condition or operating results.

The lawsuit alleges that the proliferation of DAT companies and the resulting compression of arbitrage spreads were precisely the kind of known negative trends that should have been disclosed in the Q1 2025 periodic reports (such as the 6-K and MD&A). By omitting these factors, investors claim the company misrepresented the sustainability of its expected future revenue.

While the company's SEC filings did contain general risk factors related to its business—including the high sensitivity to the volatile crypto market and the threat of intense competition—the complaint focuses on the failure to connect these general risks to the specific, quantifiable operational decay in the DeFi Alpha strategy. The later disclosure of November 14, 2025, which explicitly detailed the negative impact of DAT competition on arbitrage, essentially provided the evidence for the omitted risk that should have been present earlier in the Class Period filings.

Conclusion: Implications for Investors

The DeFi Technologies class action is more than a standard securities fraud case; it is a clinical study in the risks of digital asset treasury (DAT) companies and the peril of relying on non-core, high-yield trading strategies to meet guidance. Investors should take two key lessons from this legal action.

First, the case highlights the critical need for scrutiny when a company’s valuation hinges on a black-box revenue stream, like proprietary algorithmic arbitrage, that is vulnerable to rapid market saturation and competitive decay. Arbitrage profits, by their nature, are ephemeral; they attract competition until they vanish. The proliferation of digital asset treasury companies acted as the market’s invisible hand, choking off the very spreads the company was relying upon.

Second, the litigation reinforces the gravity of Item 303 disclosure failures. When known operational trends threaten a core component of future profitability, the law demands forthright disclosure. The time to reveal the threat was not when the revenue target was already missed, but when the trend was known to management and before the company completed a major capital raise. For investors navigating the digital asset sector, this case is a stark reminder: when management touts "exceptional performance" in a highly competitive market, the only question that matters is, How long can this last?

![Bitdeer Technologies Group (BTDR) Securities Class Action Lawsuit Update [December 8, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/btdr-alert-plus-banner.webp)

![StubHub Holdings, Inc. (STUB) Securities Class Action Lawsuit Update [December 3, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/stub-alert-plus-banner.webp)

![Blue Owl Capital Inc. (OWL) Securities Class Action Lawsuit Update [December 9, 2025]](https://dropinblog.net/cdn-cgi/image/fit=scale-down,format=auto,width=700/34260815/files/featured/owl-alert-plus-banner.webp)